Boston Scientific (BSX) Rides on Global Growth Amid Macro Woes

Boston Scientific’s BSX innovation, FDA approvals and accretive acquisitions bode well for long-term growth. Yet, unfavorable currency movement and macroeconomic concerns are major dampeners. The stock carries a Zacks Rank #3 (Hold) currently.

Boston Scientific continues to expand operations across different geographies outside the United States. In 2022, 40% of the company’s consolidated revenues came from international regions.

Within its international regions, the company is putting additional efforts to expand its foothold in emerging markets (which are defined as all countries except the United States, Western and Central Europe, Japan, Australia, New Zealand and Canada). The emerging markets hold strong growth potential based on their economic conditions, healthcare sectors and global capabilities. In Europe, the Middle East, and Africa (EMEA), Boston Scientific has been successfully expanding its base, banking on its diverse portfolio, new launches and commercial execution, given healthy underlying market demand.

Within Asia Pacific (APAC), Boston Scientific is particularly registering strong growth in Japan and China. Within Japan, the company has been benefiting from new product launches like AGENT DCB, Rezum, POLARx FIT, and WATCHMAN FLX. In China, the company has been gaining from its Imaging and Complex PCI portfolio.

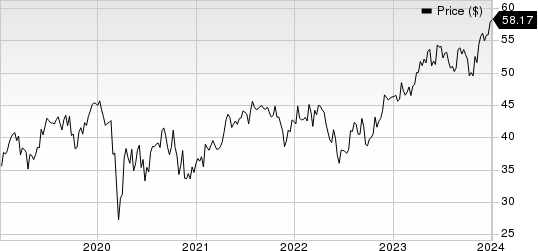

Boston Scientific Corporation Price

Boston Scientific Corporation price | Boston Scientific Corporation Quote

Boston Scientific is consistently registering fast recovery within its MedSurg segment. The Endoscopy business within MedSurg is gaining from strong worldwide demand for its broad range of gastrointestinal and pulmonary treatment options. The company recently received U.S. marketing authorization for an expanded indication of the AXIOS stent to include gallbladder drainage, increasing access to more patients.

Within Urology, Boston Scientific continues to expand its market share globally. The company’s Stone management franchise is growing well, led by LithoVue Single-Use Digital Flexible Ureteroscope System. Growth within the Prostate health franchise is led by the Rezum Water Vapor Therapy System. Further, the company is also registering strong growth within its Prosthetic urology franchise.

Within Neuromodulation, Boston Scientific’s pain business is consistently gaining traction, banking on the strength in spinal cord stimulation (SCS). Its innovative Alpha portfolio with fast therapy in a cognitive suite of digital tools supports patient activation. Boston Scientific expects SCS sales growth to improve in the second half of 2023, backed by strong trialing in the third quarter in support of clinical evidence presented in July at Aspen.

Over the past year, shares of BSX have risen 27.1% compared with the industry’s 1.7% rise.

On the flip side, challenging macroeconomic conditions in the form of inflation, disruptions in economic activity, global supply chains and labor markets, volatile financial market dynamics and significant volatility in price and availability of goods and services are putting pressure on Boston Scientific’s profitability. Further, international conflicts, including the Russia-Ukraine war and tension between China and Taiwan, have increased cybersecurity risks on a global basis. With the sustained macroeconomic pressure, the company may struggle to keep its cost of revenues and operating expenses in check.

For the third quarter of 2023, the company reported a 12.5% rise in cost of product sold and a 9.7% rise in selling, general and administrative expenses. For 2023, 2024, and 2025, our model projects the cost of products sold to grow 7.2%, 10.1%, and 7.4%, respectively, over the prior year.

As Boston Scientific records 40% of its sales from the international markets, it remains highly exposed to currency fluctuations. Unfavorable currency movements have been a major dampener over the last few quarters, as in the case of other important MedTech players too.

For full-year 2023, the company expects an approximate 100 basis-point headwind from foreign exchange on revenues.

Key Picks

Some better-ranked stocks in the broader medical space are DaVita DVA, Haemonetics HAE and HealthEquity HQY. DaVita sports a Zacks Rank #1 (Strong Buy), while Haemonetics and HealthEquity each presently carry a Zacks Rank #2 (Buy).

Estimates for DaVita’s 2023 earnings per share have remained constant at $8.07 in the past 30 days. Shares of the company have increased 36.5% in the past year compared with the industry’s rise of 10%.

DVA’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 36.6%. In the last reported quarter, it delivered an average earnings surprise of 48.4%.

Haemonetics’ stock has increased 8.7% in the past year. Earnings estimates for Haemonetics have remained constant at $3.89 for 2023 and at $4.15 for 2024 in the past 30 days.

HAE’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 16.1%. In the last reported quarter, it posted an earnings surprise of 5.3%.

Estimates for HealthEquity’s 2023 earnings per share have increased from $2.03 to $2.15 in the past 30 days. Shares of the company have increased 12.1% in the past year against the industry’s 2.1% fall.

HQY’s earnings surpassed estimates in all the trailing four quarters, the average surprise being 16.5%. In the last reported quarter, it delivered an average earnings surprise of 22.5%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Boston Scientific Corporation (BSX) : Free Stock Analysis Report

DaVita Inc. (DVA) : Free Stock Analysis Report

Haemonetics Corporation (HAE) : Free Stock Analysis Report

HealthEquity, Inc. (HQY) : Free Stock Analysis Report