Box (NYSE:BOX) Misses Q3 Revenue Estimates, Stock Drops

Cloud content storage and management platform Box (NYSE:BOX) reported results in line with analysts' expectations in Q3 FY2024, with revenue up 4.6% year on year to $261.5 million. The company expects next quarter's revenue to be around $263 million, slightly below analysts' estimates. It made a non-GAAP profit of $0.36 per share, improving from its profit of $0.31 per share in the same quarter last year.

Is now the time to buy Box? Find out by accessing our full research report, it's free.

Box (BOX) Q3 FY2024 Highlights:

Revenue: $261.5 million vs analyst estimates of $262 million (small miss)

EPS (non-GAAP): $0.36 vs analyst expectations of $0.38 (5.4% miss)

Revenue Guidance for Q4 2024 is $263 million at the midpoint, below analyst estimates of $267.2 million

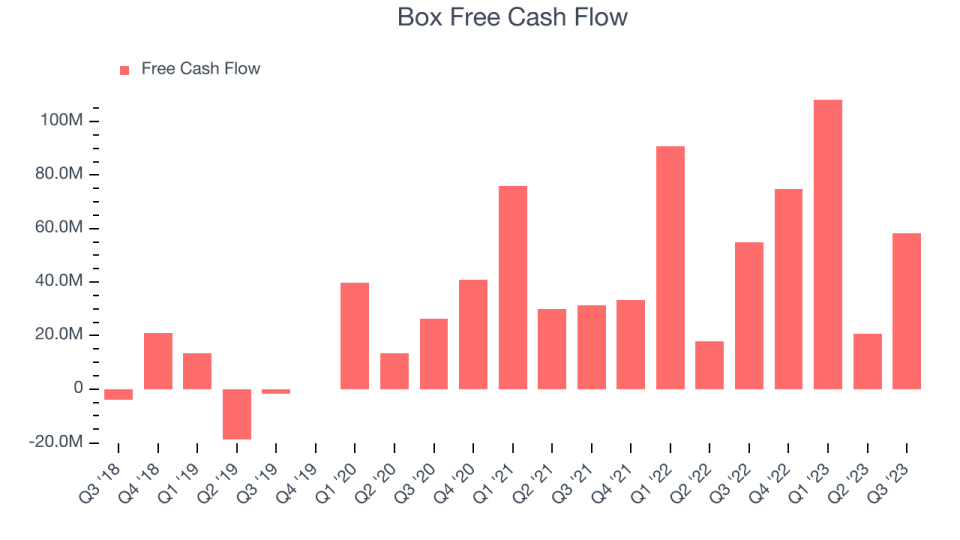

Free Cash Flow of $58.32 million, up 184% from the previous quarter

Gross Margin (GAAP): 73.5%, in line with the same quarter last year

Founded in 2005 by Aaron Levie and Dylan Smith, Box (NYSE:BOX) provides organizations with software to securely store, share and collaborate around work documents in the cloud.

Document Management

The catch phrase "digital transformation" originally referred to the digitization of documents within enterprises. The growth of digital documents has spurred an explosion of collaboration within and between businesses, which in turn is driving the demand for e-signature and content management platforms.

Sales Growth

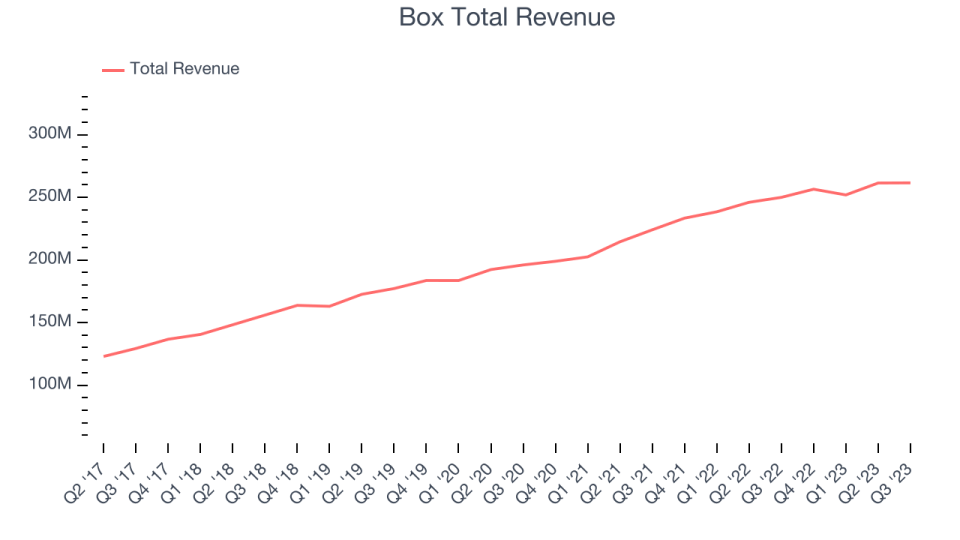

As you can see below, Box's revenue growth has been unremarkable over the last two years, growing from $224 million in Q3 FY2022 to $261.5 million this quarter.

Box's quarterly revenue was only up 4.6% year on year, which might disappoint some shareholders. Additionally, its growth did slow down compared to last quarter as the company's revenue increased by just $109,000 in Q3 compared to $9.53 million in Q2 2024. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter, Box is guiding for a 2.5% year-on-year revenue decline to $263 million, a further deceleration from the 9.9% year-on-year decrease it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 5.9% over the next 12 months before the earnings results announcement.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Box's free cash flow came in at $58.32 million in Q3, up 6.1% year on year.

Box has generated $261.8 million in free cash flow over the last 12 months, an impressive 25.6% of revenue. This high FCF margin stems from its asset-lite business model and strong competitive positioning, giving it the option to return capital to shareholders or reinvest in its business while maintaining a cash cushion.

Key Takeaways from Box's Q3 Results

Sporting a market capitalization of $3.82 billion, Box is among smaller companies, but its more than $439.7 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We struggled to find many strong positives in these results. Although its revenue was close to analysts' estimates, the company missed Wall Street's remaining performance obligations ("RPO"), billings, adjusted operating income, and EPS expectations. Its revenue guidance for next quarter and the full year also underwhelmed. Overall, this was a mediocre quarter for Box. The company is down 8.5% on the results and currently trades at $24.41 per share.

Box may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.