Braskem SA (BAK): A Modestly Undervalued Investment Opportunity?

Braskem SA (NYSE:BAK) recently saw a daily gain of 5.09%, despite a 3-month loss of -23.84%. The company reported a Loss Per Share of 1.66. Given these figures, the question arises: Is Braskem SA (NYSE:BAK) modestly undervalued? This article delves into a comprehensive valuation analysis of Braskem SA, aiming to provide readers with a clear understanding of the company's intrinsic value. We invite you to read on for an in-depth exploration.

Company Overview

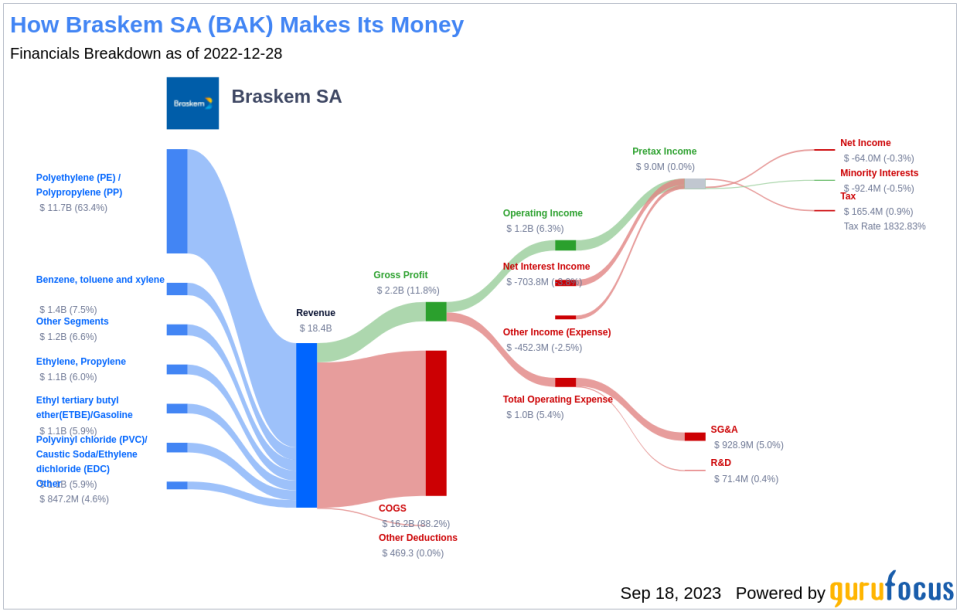

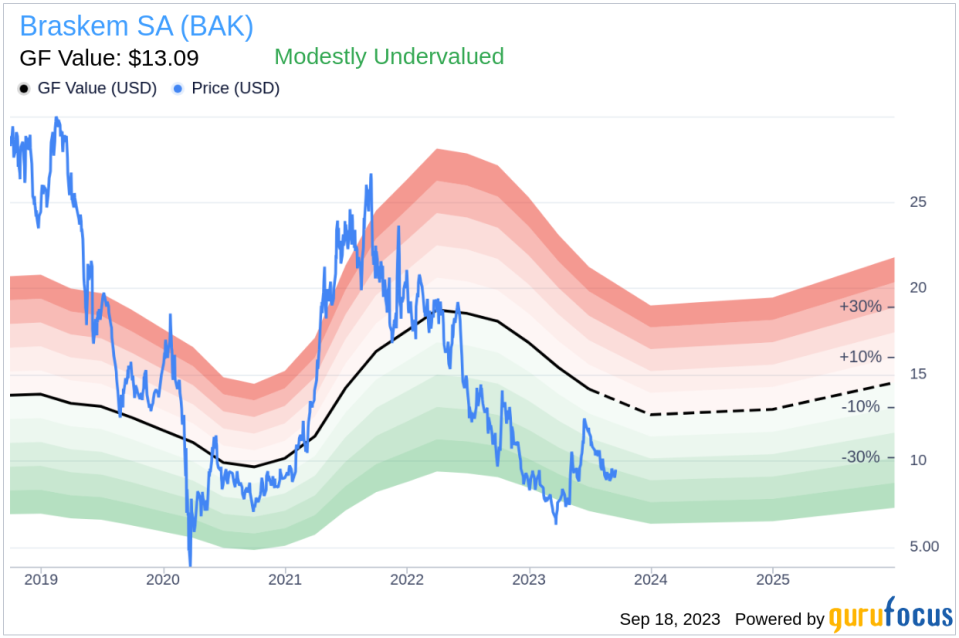

Braskem SA, a manufacturer and seller of chemicals, petrochemicals, fuels, and utilities, operates across various geographical segments, including Brazil, the United States, Europe, and Mexico. The company's primary revenue comes from Brazil. Braskem SA produces olefins, fuels, and intermediates, and its current stock price stands at $9.49. With a market cap of $3.80 billion, the company's GF Value, a proprietary measure of fair value, is estimated at $13.09, suggesting that the stock may be modestly undervalued.

Understanding the GF Value

The GF Value is a proprietary measure that represents the intrinsic value of a stock. It is calculated based on historical multiples, a GuruFocus adjustment factor based on the company's past performance and growth, and future business performance estimates. The GF Value Line provides an overview of the stock's fair value. If the stock price is significantly above this line, it is considered overvalued and might offer poor future returns. Conversely, if it is below the GF Value Line, it is likely undervalued, potentially offering higher future returns.

Braskem SA (NYSE:BAK) appears to be modestly undervalued according to the GF Value. This suggests that the long-term return of its stock is likely to be higher than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength

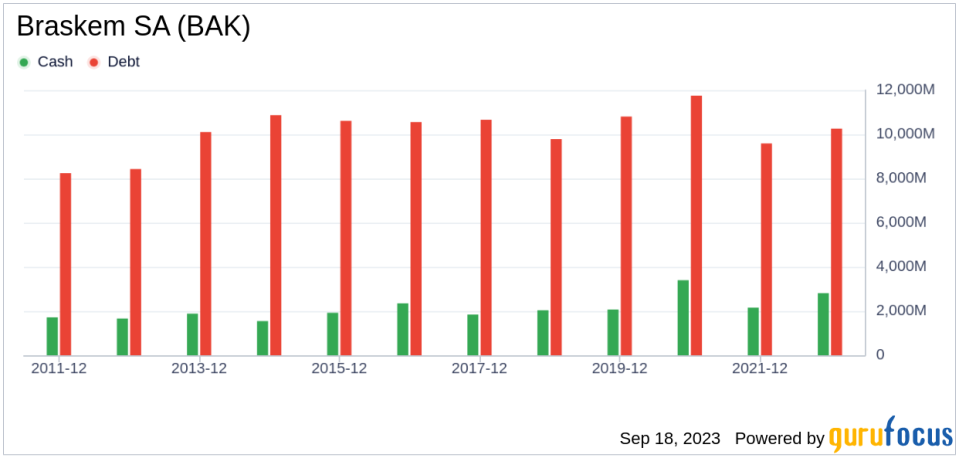

Before investing in a company, it's crucial to assess its financial strength. Companies with poor financial strength pose a higher risk of permanent loss. Braskem SA's cash-to-debt ratio of 0.29 is worse than 70.93% of companies in the Chemicals industry, indicating poor financial strength.

Profitability and Growth

Investing in profitable companies typically carries less risk. Braskem SA has been profitable six years over the past decade. However, its operating margin of -3.56% is worse than 85.11% of companies in the Chemicals industry. The company's growth, however, ranks better than 80.28% of companies in the industry, with an average annual revenue growth of 22.7%.

ROIC vs WACC

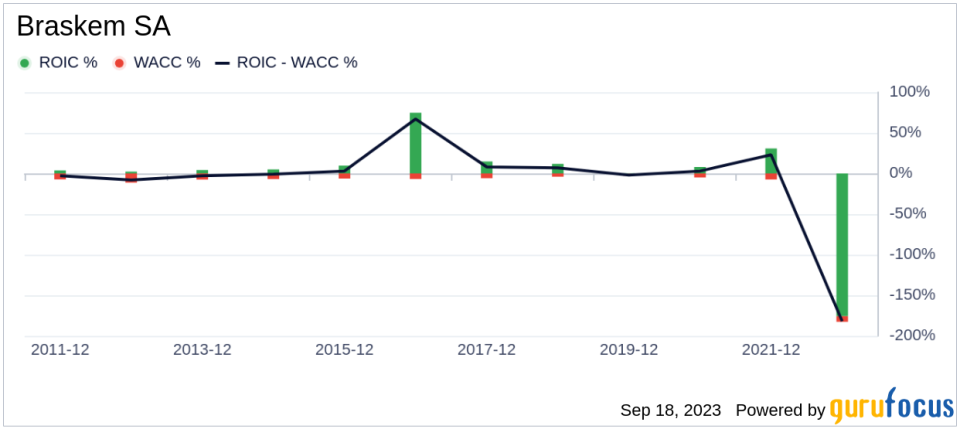

Comparing a company's Return on Invested Capital (ROIC) to its Weighted Average Cost of Capital (WACC) is another way to evaluate its profitability. If the ROIC is higher than the WACC, it indicates that the company is creating value for shareholders. Over the past 12 months, Braskem SA's ROIC was -3.99, while its WACC came in at 2.43.

Conclusion

In conclusion, Braskem SA (NYSE:BAK) appears to be modestly undervalued. Despite poor financial strength, its profitability is fair, and its growth ranks better than many companies in the Chemicals industry. For more information about Braskem SA, you can check out its 30-Year Financials here.

To find high-quality companies that may deliver above-average returns, check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.