Brinker International (EAT): A Closer Look at Its Undervalued Status

Brinker International Inc (NYSE:EAT) experienced a daily gain of 4.69%, although it has seen a 3-month loss of -11.87%. The company's Earnings Per Share (EPS) stands at 2.24. This article aims to answer the question: Is Brinker International (NYSE:EAT) modestly undervalued? We will delve into a comprehensive valuation analysis of the company, providing you with valuable insights into its intrinsic worth.

Company Overview

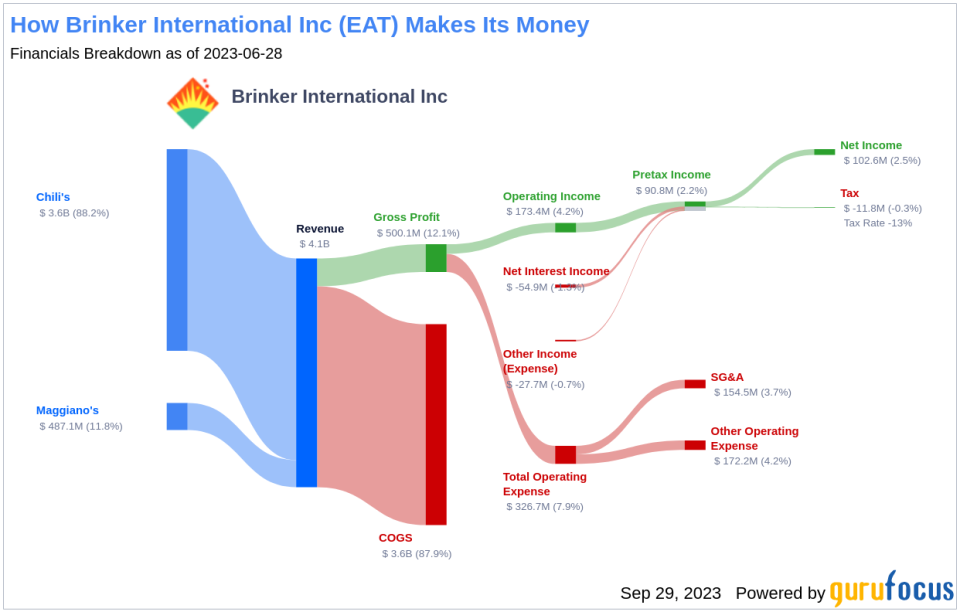

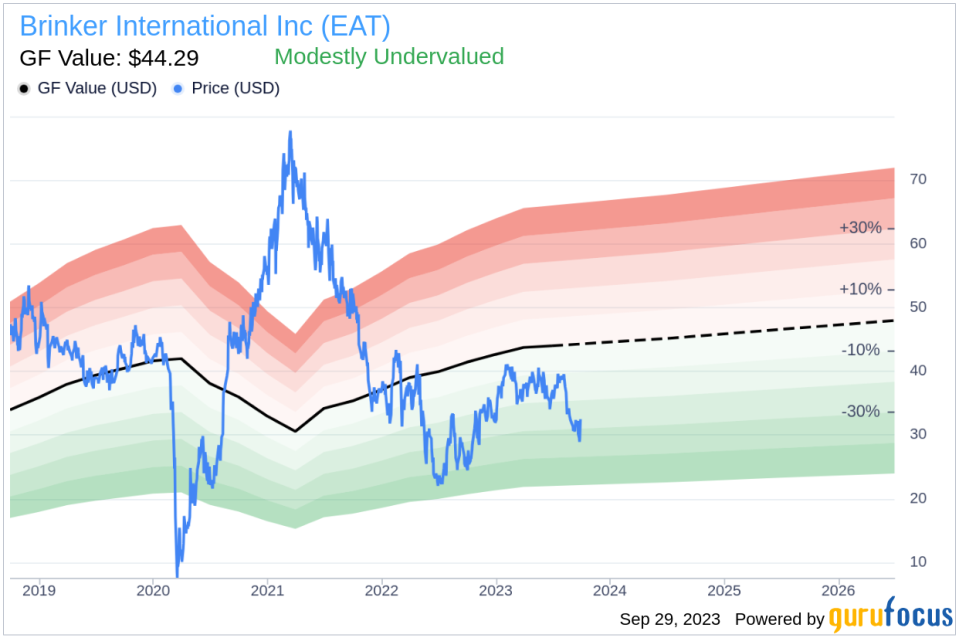

Brinker International operates casual dining restaurants under the brands Chili Grill and Bar (Chili's) and Maggiano's Little Italy (Maggiano's). With a market cap of $1.50 billion and sales reaching $4.10 billion, the company has carved a niche in the casual dining sector. Its stock price currently stands at $32.51, while the GF Value, an estimation of its fair value, is $44.29. This initial comparison suggests that Brinker International (NYSE:EAT) may be modestly undervalued.

Understanding GF Value

The GF Value is a proprietary measure that represents the current intrinsic value of a stock. This measure is derived from three key factors: historical multiples that the stock has traded at, a GuruFocus adjustment factor based on the company's past performance and growth, and future estimates of business performance. The GF Value Line provides an overview of the fair value at which the stock should ideally be traded.

Brinker International's stock is believed to be modestly undervalued based on GuruFocus' valuation method. The GF Value estimates the stock's fair value at $44.29, suggesting that at its current price of $32.51 per share, Brinker International's stock may be undervalued and have higher future returns.

Financial Strength

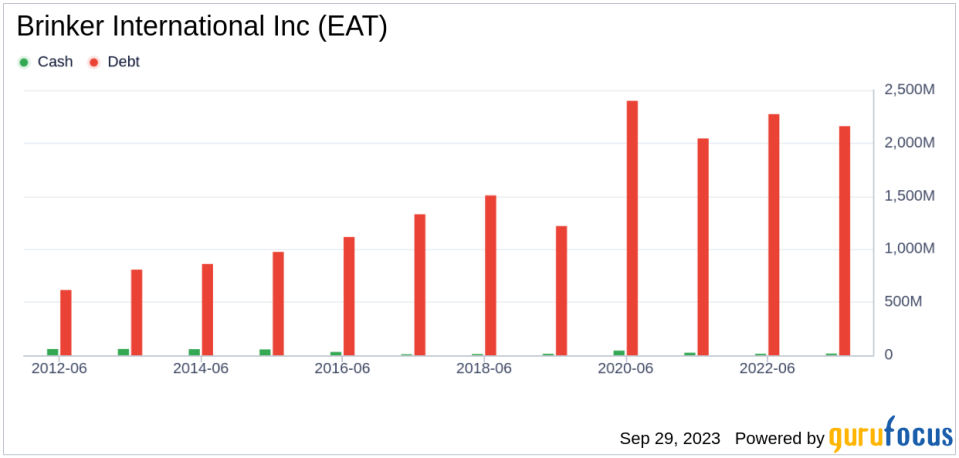

Investing in companies with poor financial strength can pose a high risk of permanent capital loss. Brinker International's cash-to-debt ratio of 0.01 ranks worse than 96.56% of 349 companies in the Restaurants industry, indicating that the company's financial strength is poor.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, poses less risk. Brinker International has been profitable for 10 out of the past 10 years, with an operating margin of 4.18%, ranking better than 53.56% of 351 companies in the Restaurants industry.

One of the most important factors in the valuation of a company is growth. Brinker International's average annual revenue growth is 5.1%, which ranks better than 71.12% of 329 companies in the Restaurants industry. Its 3-year average EBITDA growth is 6.2%, ranking better than 56.32% of 277 companies in the Restaurants industry.

ROIC vs WACC

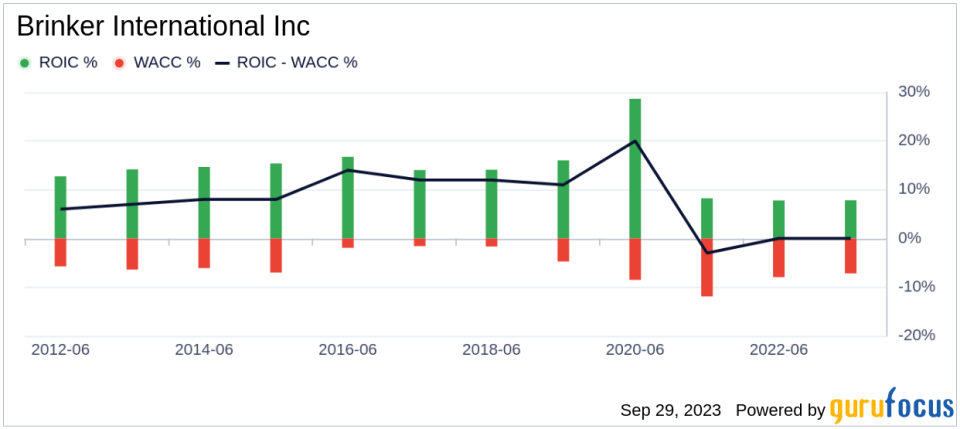

Comparing a company's return on invested capital (ROIC) to its weighted cost of capital (WACC) is another way to evaluate its profitability. Brinker International's ROIC over the past 12 months was 7.83, while its WACC came in at 6.22, indicating that the company is creating value for shareholders.

Conclusion

Overall, Brinker International (NYSE:EAT) stock appears to be modestly undervalued. The company's financial condition is poor, and its profitability is fair. However, its growth ranks better than 56.32% of 277 companies in the Restaurants industry. To learn more about Brinker International stock, you can check out its 30-Year Financials here.

To discover high-quality companies that may deliver above-average returns, check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.