Bull of the Day: Casey's General Stores, Inc. (CASY)

Casey's General Stores, Inc. (CASY) stock has crushed the S&P 500 and its sector over the last 20 years and more recently by effectively and efficiently operating simple, essential local businesses.

Casey's General Stores’ outlook is solid and CASY stock has been the picture of consistency, helping make CASY an attractive long-term addition to a diversified portfolio.

General Store Giant

Casey's operates over 2,500 convenience stores across 17 states, mostly in the Midwest. The company’s offerings include your typical convenience store fare and an array of grocery items, as well as freshly prepared food. Casey’s has become known for its donuts, sandwiches, breakfast food, and most of all, its pizzas. Casey’s also operates self-service fuel stations at nearly every location.

The combination of its one-stop offerings and well-run stores have helped Casey's become staples in local communities and on Wall Street. Roughly 50% of Casey's stores are in towns and areas with populations of 5,000 people or less. The firm is expanding its reach into larger regions, with about 25% of CASY locations now in areas with 20,000 people or more.

Image Source: Zacks Investment Research

Casey's has adapted along with the wider retail segment by rolling out digital offerings to boost convenience and customer loyalty. The company’s mobile app and online ordering enable customers to easily order food, locate stores, and access exclusive deals and promotions.

Recent Performance and Outlook

Casey's relatively small geographical footprint enables it to stock a large chunk of its stores out of just three distribution centers. These three locations help supply 90% of in-store products and roughly 55% of fuel. The company also currently offers nearly 350 private label items, with more to come.

Casey's topped our second-quarter fiscal 2024 EPS estimate on December 11 and boosted its guidance once again. The firm said that it was able to reduce same-store labor hours while expanding its business. On top of that, Casey's built or acquired 59 stores in the quarter and recently entered Texas (its 17th state) via a 22-store acquisition that closed in November.

Image Source: Zacks Investment Research

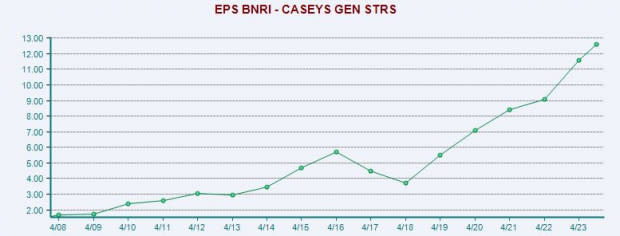

Casey’s fiscal 2024 revenue is projected to climb marginally as it faces tough year-over-year comparisons over the past several years for a variety of reasons. Yet, the firm’s efficiency remains on full display, with its adjusted earnings projected to climb by 9% in FY24 and another 8.3% higher next year. The company is also projected to post 6% revenue growth next year.

Casey’s current year EPS estimate has climbed 10% in the past two months, with FY25’s consensus 7% higher. The company’s most accurate/ recent earnings estimates have also come in above consensus for all periods. All of CASY’s upbeat earnings revisions activity helps it land a Zacks Rank #1 (Strong Buy) right now.

Performance, Technical Levels & Valuation

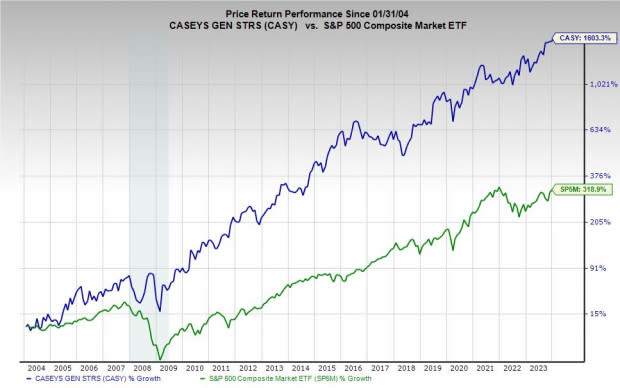

CASY has soared nearly 1,600% in the last 20 years to blow away the Zacks Retail-Wholesale sector’s 372% and the S&P 500’s 318%. CASY stock has also crushed Walmart (WMT) and Target (TGT) over this stretch, both of which unperformed the Zacks Retail-Wholesale sector and the S&P 500.

Image Source: Zacks Investment Research

The company’s shares have climbed 120% in the past five years vs. its sector’s 38% and the benchmark’s 86%. The current run includes a 15% jump during the trailing six months.

CASY looks a tad overheated based on historic RSI levels, but the stock has consistently traded above its 50-month moving average for roughly 20 years outside of a few occasions. Casey’s found support at its 50-day recently and the stock trades slightly below its November records and 12% beneath its average Zacks price target.

Despite its stellar outperformance of the Zacks Retail-Wholesale sector, CASY trades at a 5% discount at 21.1X forward 12-month earnings, while Walmart trades at 22.7X. Casey’s current valuation levels also mark a nearly 30% discount to its 10-year highs.

Image Source: Zacks Investment Research

Bottom Line

Casey’s is expanding its reach and its offerings while attempting to boost efficiency and stock buy backs to return more value to shareholders. CASY’s 0.6% dividend yield is a nice bonus on top of its impressive performance, and its balance sheet is solid.

Casey’s operates in a somewhat unique area of Wall Street, serving small-town America. One could argue that its businesses are more essential to the communities they serve than the likes of Walmart, Target, and many others. CASY’s outperformance appears to agree.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

Casey's General Stores, Inc. (CASY) : Free Stock Analysis Report