Bull Of The Day: EverQuote (EVER)

EverQuote (EVER) is a Zacks Rank #2 (Buy) and it sports that growth divergence that I love to see. Growth investors and value investors are inheirently looking for different things and when I see a weak Zacks Style Score for Value and a strong Zacks Style Score for Growth I know I am on the right path. Let's take a deeper look at EVER in this Bull of the Day article.

Description

EverQuote, Inc. operates an online marketplace for insurance shopping in the United States. Its online marketplace offers consumers shopping for auto, home and renters, life, health, and commercial insurance. The company serves carriers, agents, and indirect distributors and aggregators. The company was formerly known as AdHarmonics, Inc., and changed its name to EverQuote, Inc. in November 2014. EverQuote, Inc. was incorporated in 2008 and is headquartered in Cambridge, Massachusetts.

Earnings History

I see a great earnings history for EVER, with four of the last four quarters all coming in ahead of the Zacks Consensus Estimate. The company posted one outsized beat of 250% and that skews the average positive earnings surprise over the last year to 86%, but without that the number would still be north of 30%.

That tells me these are good sized beats, only one in the last four quarters was just a penny more than the consensus.

Estimate Revisions

There have been lots of negative earnings estimate revisions across the entire market. I see a mixed bag here for EVER as this quarter has seen some positive and negative revisions. The current quarter saw an increase of 2 cents over the last 30 days while the full year saw a decrease of 2 cents as well.

As things stand now, next year is looking at a loss of 4 cents, but there is a good chance that turns around.

Valuation

With estimates just sliding under the breakeven line for next year, the forward PE is NA since the number is negative. What we do see is a 22x book multiple and that is high… but so is the growth of 55% in the most recent quarter. Price to sales of 4.5x is right inline with where it should be and it could easily move to 6x or 7x as margins expand.

The operating margin has been headed in the right direction, moving from -6% to -2.8% to -1.5% over the last three quarters. The COVID pandemic probably isn’t going to help, but as the pandemic loses steam, look for margins to turn positive and that will certainly send this stock higher.

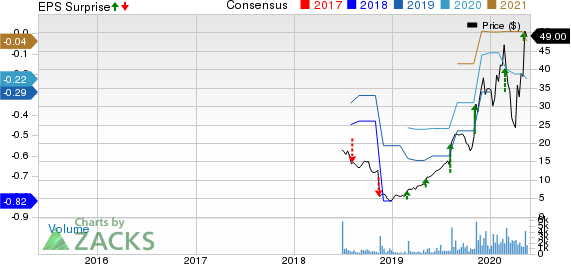

Chart

EverQuote, Inc. Price, Consensus and EPS Surprise

EverQuote, Inc. price-consensus-eps-surprise-chart | EverQuote, Inc. Quote

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2021.

Click here for the 6 trades >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

EverQuote, Inc. (EVER) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research