‘The Bull Market Can Continue to Roll On;’ BMO’s Brian Belski Predicts Further Gains for Stocks — Here Are 3 Names to Play That Bullish Sentiment

We recently passed an anniversary, of sorts – one year to the day since the stock market hit bottom. On October 12 of last year, the S&P 500 reached its trough; since then, the market trend has been upward despite some volatility and a recent pullback.

Brian Belski, chief investment strategist from BMO Capital, believes that we’re into a secular bull market now. Looking at a series of factors – general economic growth, the slowing pace of inflation, the stage of the Fed’s monetary policy, Belski comes down on the side of the bulls, writing, “it has become increasingly clear over the past year that the economy has held up much better than expected while inflation has cooled closer to normal levels…”

This sets the stage for a bull market that can deliver further gains. As such, although nothing is set in stone, Belski gives an upbeat vision for the coming year. “While there is certainly no perfect historical comparison that can be used to lay out the road map for stocks in the future,” he says, “we are confident that the secular bull market can continue to roll on, especially given the current fundamental states of US stocks and the economy.”

With that promising outlook as background, the stock experts at BMO are pointing investors toward the names that are poised to do well in the year ahead; they see three specific equities as potential winners, with one boasting upside of more than 170%. We used the TipRanks Database to also find out what the rest of the Street makes of these choices. Let’s check the details.

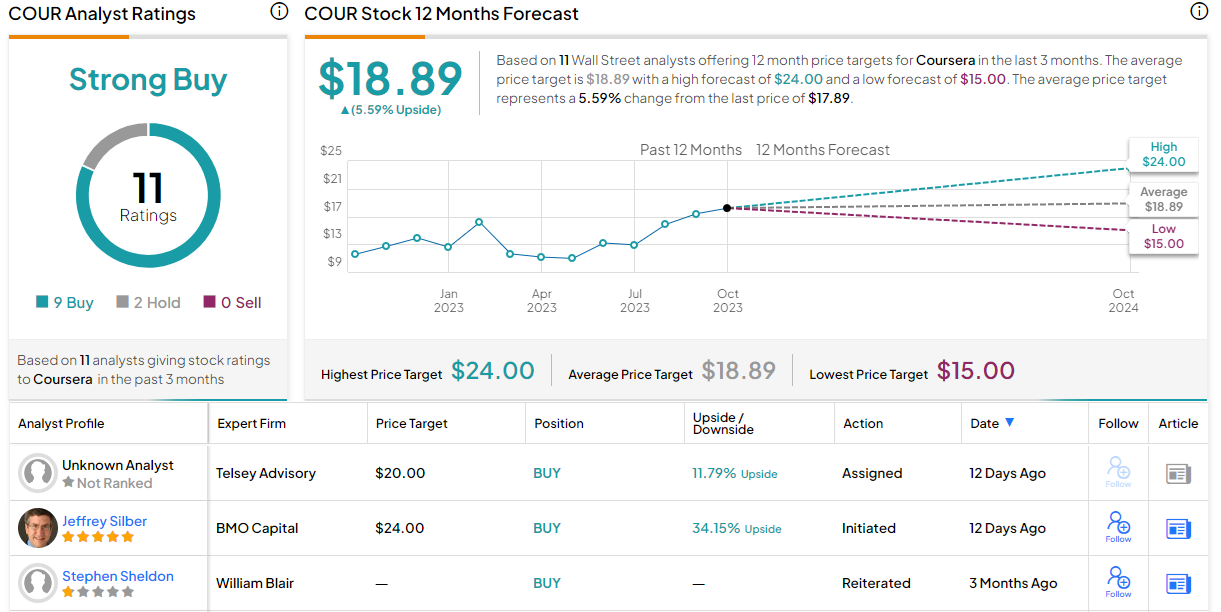

Coursera (COUR)

We’ll start in the world of online learning. Coursera operates an online platform for college level courses, connecting learners with the courses they need, whether for professional development, degree credit, or personal expansion. The company’s catalog includes a wide range of studies and subjects, and Coursera can boast that it has over 129 million registered learners. It all points toward the company’s goal, providing universal access to world-class higher education.

Coursera doesn’t operate in a vacuum, and it has working relationships with more than 300 leading university, business, and industry partners. Among the company’s partners are such major names as Google, IBM, and the University of Michigan. Coursera is always looking to expand its course offerings, and new offerings include courses from Microsoft, DeepLearning.AI, and Amazon Web Services. Students new to online higher ed can start with a set of courses offered free of charge.

Ever since the COVID pandemic, online learning has been a big business. Coursera has leveraged that to achieve consistent quarter-over-quarter revenue growth for the past several years. In the last reported quarter, 2Q23, the company’s top and bottom lines both beat the forecasts; revenue came in at $153.7 million, $7.5 million better than expected and up 23% year-over-year, and the GAAP EPS, while a loss of 21 cents per share, was 8 cents per share better than the estimates. The EPS loss marked a 38% improvement on the prior year’s Q2 result.

Coursera will report its 3Q23 numbers on October 26, and the Street is looking to see $158.3 million in revenue along with an EPS loss of 26 cents per share.

In coverage for BMO, analyst Jeffrey Silber notes Coursera’s steadily increasing revenues and sees more gains ahead. The 5-star analyst writes, “We expect COUR’s robust revenue growth to continue through its flywheel approach and taking advantage of key secular drivers (upskilling, digital transformation, international). While the company is not yet profitable, it should get there over time given the scalable nature of its learning platform. Despite the rally in shares post 2Q23 results and some current risk to its Enterprise segment (slowing growth), we believe this stock will generate long-term benefits for investors.”

Along with these views, Silber sets an Outperform (Buy) rating on the stock, and his $24 price target implies a one-year potential upside of 34%. (To watch Silber’s track record, click here)

The Strong Buy consensus rating on COUR shares is based on 11 recent analyst reviews with a 9 to 2 breakdown in favor of Buys over Holds. The stock is selling for $17.89 and its $18.89 average price target suggests it will gain a modest 5.5% over the coming year. (See Coursera stock forecast)

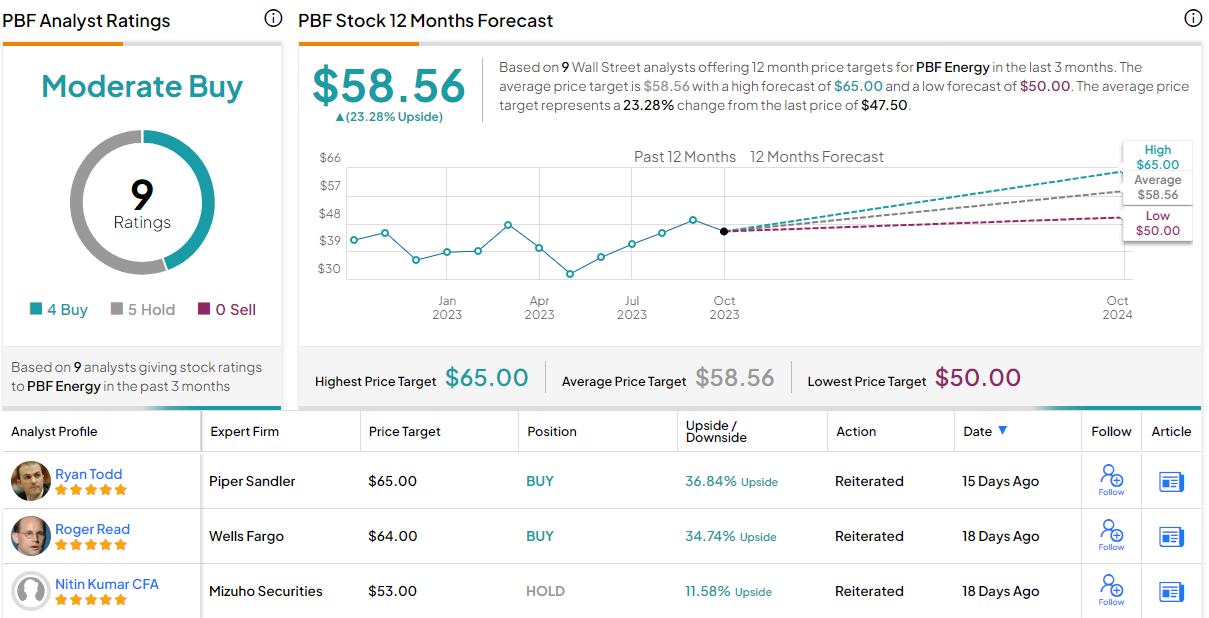

PBF Energy (PBF)

Next on our list of BMO picks is an energy company, the aptly named PBF Energy. This New Jersey-based firm is one of the largest petroleum refiners in the US, an independent company in the industry and a leader in producing petroleum products from crude oil. PBF refines and distributes transportation fuels, heating oil, lubricating oils, and petrochemical feedstocks; the range of products are sent out through the company’s logistic operations as unbranded fuels. PBF’s network includes storage facilities, tanker trucks, and marine vessels, along with the Delaware Pipeline Company.

The heart of PBF’s operation, however, is the refinery business. The company operates six refineries – Delaware City, DE; Paulsboro, NJ; Toledo, OH; New Orleans, LA; and Torrance and Martinez, both in CA. All together, these refineries can produce over 1 million barrels per day of petroleum derivatives.

We’ll see PBF’s results from 3Q22 early next month; for now, we can look back at the firm’s 2Q23 results, which beat the Street’s forecasts.

The company reported revenues of $9.16 billion, beating the forecast by $223.5 million – although the top line was down 35% year-over-year. The company’s earnings result was posted as a non-GAAP EPS of $2.29 per diluted share; this result was less than one-fourth the year-ago value – but it was also 5 cents per share better than had been anticipated.

Even though the top and bottom lines fell y/y, PBF retained its confidence and maintained its reinstated dividend. The company had ceased payment during the COVID crisis, but resumed the quarterly dividend in November of last year. The last payment to go out was sent on August 31 at 20 cents per common share. The annualized payment of 80 cents per share gives a modest yield of 1.68%.

BMO’s Phillip Jungwirth sees PBF as a solid player in its industry, and writes of the stock, “Nobody has benefited more during the refining upcycle than PBF with elevated financial leverage incurred during COVID erased, while key PADD 1 and 5 markets have structurally improved from refinery closures and conversions, with more to come in California (Rodeo) and PADD 1 product inventories remaining tight. PBF has higher operating leverage to cracks, which have retraced recently, although its net cash position and discounted valuation supports a favorable risk/reward.”

Jungwirth goes on to give the stock its Outperform (Buy) rating and a price target of $60 that indicates his confidence in a 26% upside for the year ahead. (To watch Jungwirth’s track record, click here)

The 9 recent reviews on this stock split to 4 Buys and 5 Holds, supporting a Moderate Buy consensus rating. With an average target price of $58.56 and a current trading price of $47.5, PBF boasts a 23% upside potential for the next 12 months. (See PBF stock forecast)

Prime Medicine (PRME)

We’ll wrap up this list in the medical sector, with Prime Medicine. This biotechnology company is working to take genetic medicines to the next level, using its Prime Editing gene editing technology to create new genetic therapies that target only the right edit at the right position within a gene. The goal is to create precision genetic medicines that are one-time curative therapeutic agents.

The company’s approach has broad therapeutic applications, and in theory can repair some 90% of the known disease-causing genetic mutations across many different cell types and body organs. So far, Prime has created a portfolio of 18 genetic medicines. While none have reached the clinical trial stage as yet, a few are approaching that milestone.

Chief among these is PM359, a development candidate for chronic granulomatous disease (CGD). Prime is on track to initiate the investigational new drug- enabling studies before the end of this year, a key step toward beginning human clinical trials. The company is looking to complete its first IND filing next year, and anticipates additional filings in 2025.

The potential of the developmental pipeline informs Kostas Biliouris’ take on the stock. He writes for BMO, “Our thesis is based on the fact that the characteristics of prime editing (high specificity/versatility) appear to be highly differentiated compared to other gene editing approaches, and can potentially offer superior/broader applicability. Despite Prime’s early-stage pipeline, we believe near-term partnerships and key catalysts in the gene editing space can drive upside, while mid-term derisking of Prime’s platform will fuel growth.”

Looking ahead, Biliouris rates the shares as Outperform (Buy) and sets a $19 price target, pointing toward a one-year gain of 172%. (To watch Biliouris’ track record, click here)

Turning now to the rest of the Street, where the Strong Buy consensus rating here is based on 3 additional reviews that include 2 Buys and 1 Hold. The stock has a selling price of $6.99 and its $20.50 average target price implies a robust upside of 193% for the next year. (See PRME stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.