Should You Buy iRobot Stock at Below $9?

Things have gone from bad to worse for iRobot (NASDAQ: IRBT) stock. The robotic cleaning device specialist's shares just fell below $9 to mark an over 80% decline in the past full year.

Investors weren't happy to hear that the proposed buyout from Amazon failed its regulatory review. There was more bad news to follow about iRobot's weak short-term outlook as well.

It's possible that the stock's decline reflects an overreaction on Wall Street and that iRobot will beat the market from here. Yet investors need to balance that potential against the likelihood that the company won't succeed at building a sustainably profitable business. Let's take a look at why the stock doesn't look compelling even at its current discounted price.

The weak outlook

iRobot isn't even close to approaching sales stabilization. Instead, revenue is likely to fall by more than 20% in fiscal Q2 after declining by about 10% in Q1, management said in a mid-March operating update.

The device maker entered 2024 with weak momentum. Sales dove to $891 million in 2023 from $1.2 billion, in fact, as consumers shifted spending away from the robotic cleaning device niche.

That demand slump coincided with a flood of new competition, which made it harder for iRobot to defend its market position. Rivals are increasingly competing on price since they are dealing with the same inventory overhang that iRobot faces. It's a perfect storm, then, that pairs declining sales and falling profits for most industry participants at least through the 2024 year.

"We are managing through a challenging period," interim CEO Glen Weinstein said in a recent press release. There's no indication to date that this difficult selling environment is ending.

Financial struggles

The stock might still be attractive if iRobot was making progress toward profitability, perhaps through price increases combined cost cuts and layoffs. But that's just not the case today.

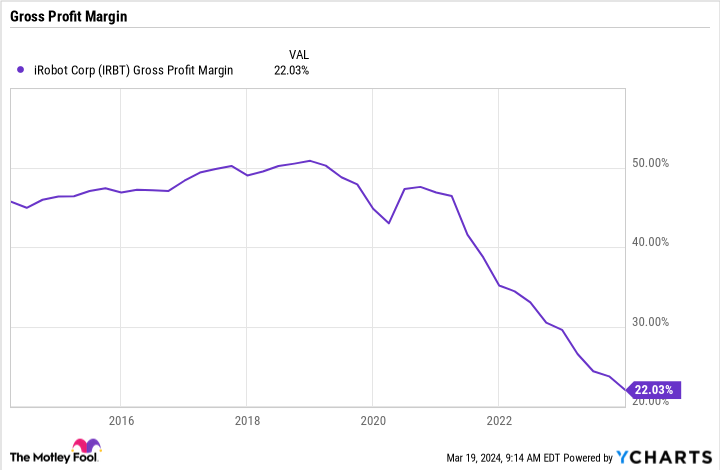

iRobot is projecting significant net losses in 2024 following gushing red ink in both 2023 and 2022. That's partly thanks to declining demand, but it's also a reflection of the fact that its costs are unsustainably high. Despite rising prices, gross profit margin has been slumping since 2021.

It's hard to see a path back to the 50% rate that shareholders saw before the pandemic struck. In fact, management is only projecting a modest rebound -- powered by layoffs and a restructuring program -- ahead for this core profitability metric as gross profit margin rises to around 33% of sales in 2024. Shareholders are right to be demanding more from this consumer device maker.

Bumping along

iRobot executives say that their restructuring plan, which includes a 31% reduction in the workforce and the exit of unprofitable geographies, will start to bear fruit in the second half of 2024, yet investors should take that forecast with a grain of salt.

Sales trends will worsen over the next few quarters first, they say, before the rebound starts to take shape later in 2024. In the meantime, iRobot should continue generating net losses as its sales footprint shrinks.

Don't be tempted, then, by the big discount being offered on this stock right now. Sure, you can own iRobot shares for 0.3 times sales, which is the lowest valuation to date on the stock. Yet there's no concrete evidence of a growth or earnings recovery in the works. Meanwhile, the company is burning through cash today and is projecting more outflows through the first half of 2024.

A return to positive cash flow in the second half of the year would be an encouraging sign of progress. But investors should still wait at least until then before considering iRobot stock as a potential long-term investment.

Should you invest $1,000 in iRobot right now?

Before you buy stock in iRobot, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and iRobot wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Demitri Kalogeropoulos has positions in Amazon. The Motley Fool has positions in and recommends Amazon and iRobot. The Motley Fool has a disclosure policy.

Should You Buy iRobot Stock at Below $9? was originally published by The Motley Fool