Buy now, pay later options are increasing

During the holiday shopping season, layaway is a popular option for consumers to buy everything from toys to TVs. Offered by big-box retailers like Walmart, Sears and T.J. Maxx, the program lets in-store shoppers put items on layaway, spread the cost out over several payments, and take it home when it’s all paid up.

A new breed of companies like Afterpay and Klarna have emerged, prompting renewed interest in the buy now pay, later service.

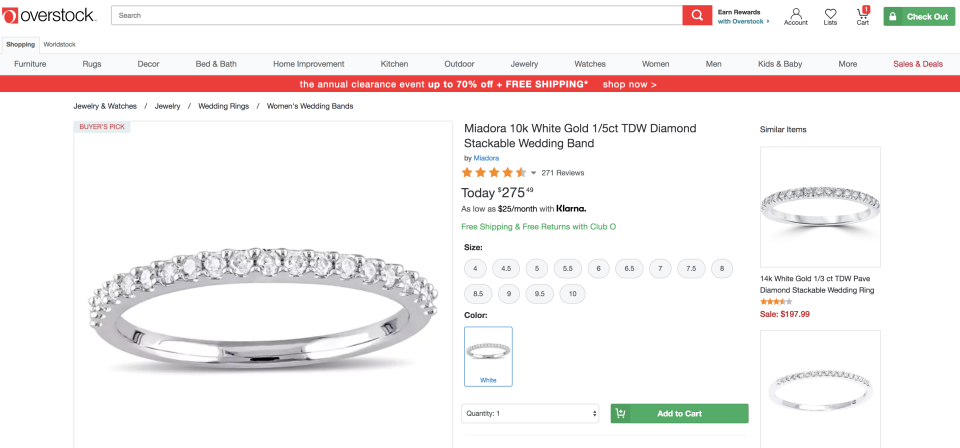

Offering the installment payment service across multiple retailers – and not just during the holiday season — these companies let you buy anything you want, from underwear to diamond rings, take it home and still feel like you’re not splurging.

Afterpay and Klarna are tapping into a market that’s ripe for micro loans. With 35% of millennials never owning a credit card — the lowest across all generations, according to data from CreditCards.com — and a high degree of sensitivity toward debt, these companies fill a gap for those who want to spend more, but don’t want to take on credit card debt.

The concept of micro-installment payments is not new.

Apart from big retail chains like T.J. Maxx and Walmart, PayPal Credit (PYPL) has also been offering micro-loans that are interest-free if paid within a fixed term.

But what these companies offer is an instant financing option on the central checkout page for popular millennial-focused retailers like Anthropologie, Revolve, Overstock.com, Urban Outfitters and Wish. (Walmart and T.J. Maxx, for example, only offer their layaway programs for in-store purchases.)

‘Life’s little luxuries’

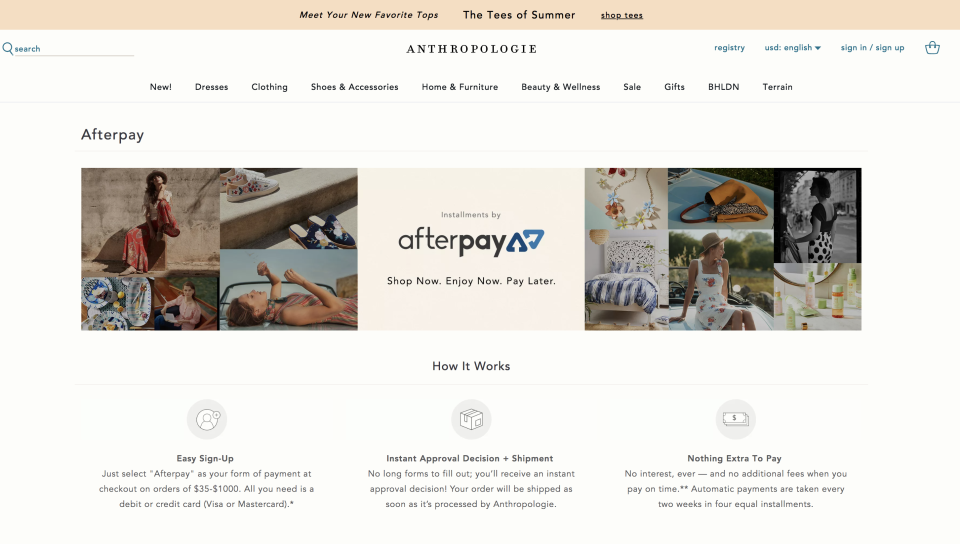

Afterpay offers small loans with a minimum order value of $35, focusing on the beauty and fashion space. So, for instance, that $198 dress from Anthropologie can be had for four installments of $49.50 instead of paying the full amount upfront.

Founded in Australia in 2015, the company works with around 16,500 retailers in that country, including Estee Lauder, Lululemon and Sephora. In a press release, Afterpay said it processes more than 25% of all online fashion and beauty transactions in Australia.

The idea is simple: with Afterpay, you can buy a product immediately and pay for it in four interest-free installments, due every two weeks. You’re not required to enter into a traditional loan, or pay any upfront fees or interest.

If you default on your payment, there’s a $10 late fee at first, and another $7 fee if the payment remains unpaid seven days after the due date. You won’t be able to make another AfterPay purchase until you’ve paid up.

The company absorbs default risk on behalf of the retailers, and the platform is friendly to the merchant’s existing infrastructure. Nick Molnar, co-founder and CEO of Afterpay, told Yahoo Finance that the company’s net transaction loss for 2017 was less than 1%.

The average purchase value with Afterpay is between $150 to $200, Molnar said. The small amounts are deliberate because the company is “focused on life’s little luxuries, like fashion, beauty and homewares, rather than a $2,000 couch or electronics purchase,” he said.

Klarna

Similarly, Swedish bank Klarna, founded in 2005, also gives consumers a fixed amount of time to pay — from when the item is shipped.

However, the duration is set between Klarna and the retailer — so it could be six, 12- or 18-month plans. And unlike Afterpay, which always divides your payment into four installments, Klarna “slices up” your purchases based on their agreement with each retailer — and that process (instead of paying in full at the expiration date) incurs interest.

The company, which was valued at $2.5 billion, is rapidly expanding to new markets.

Klarna has 3 million American users, Malin Eriksson, Klarna’s North America CEO, told Yahoo Finance. It has 60 million users across the world, and processes 800,000 purchases a day worldwide — which translates to 290 million transactions a year in the 14 markets they’re in, said Eriksson.

‘Not going to get into a debt trap’

The primary appeal of these installment plans is the opportunity to buy from a trendy retailer like Urban Outfitters and stagger the payments, interest-free.

“The fees themselves are very low — you’re talking about a millennials and younger consumers — they’re traditionally more averse to racking up debt,” James Wester, the research director of global payments at IDC Financial Insights, told Yahoo Finance. “They don’t like paying on credit cards.”

“When you pay with a credit card, you have a minimum payment due, and you have a revolving payment — it’s easier to get into trouble,” said Wester.

Credit cards charge higher interest rates and fees, and can also hurt your credit score if you’re late with payments.

Afterpay and Klarna don’t — hence, “I’m not going to get into a debt trap,” said Wester.

“I’m going to go in, the terms and conditions are very clear, and I know when I’m going to pay this off. That’s where the attraction is, to consumers.”

Free People now offers AfterPay and my bank account is in trouble

— myah (@myaahhmxx) July 24, 2018

i just made 2 seperate orders for the same store so i could use different discount codes in order to save $6 – but still use afterpay. i hate myself

— ♡goth spice♡ (@gxthspice) July 21, 2018

Paid all my bills incl. next months, paid off my afterpay’s. Wahhh. Being an adult 😭

— Jessica (@j_l_t_f) July 21, 2018

Paying in installments can lull consumers into feeling like they’re financially savvy – yes, it’s more manageable, but eventually, those shoes will have to be paid for. Afterpay has gotten so big in Australia that it prompted one expert to warn people that it could fuel unsafe spending.

As of now, in the U.S., Afterpay is currently live with 200 retailers, and has 400 more signed. Klarna is in discussions to expand, hoping to mimic their success with major retailers like ASOS and Zara in Europe.

Follow Aarthi on Twitter.

Read more: