Campbell Soup (CPB) Shows Strategic Resilience Amid Challenges

Campbell Soup Company CPB has made significant progress in advancing its strategic plan, demonstrating resilience in the face of a challenging and changing consumer landscape. The company is well-positioned to capitalize on various opportunities within its portfolio to align with evolving consumer trends. CPB’s Snacks business has been performing well for a while now.

The impressive momentum, coupled with the pending acquisition of Sovos Brands, positions Campbell Soup for growth. However, the company projected a decline in volumes for the first half of fiscal 2024 on its first-quarter fiscal 2024 earnings call. CPB is also battling cost inflation, though it has been moderating from the year-ago period levels.

Factors Adding Flavor to CPB

On its first-quarter earnings call, Campbell Soup stated that it has optimized its strategies and plans, focusing on three key areas. These include ensuring product affordability and maintaining competitive pricing within the boundaries of margin goals, sustaining marketing and innovation initiatives and adhering to a disciplined and balanced spending approach, with a focus on high return on investment (ROI) and impactful plans.

Management’s consistent execution has been noteworthy, with robust and sustained performance across the supply chain, successful innovations, effective marketing programs and recent share trend improvements. Management expects these focus areas to aid sequential improvement throughout the year, driving momentum in revenues, volumes, market share and profit margins, especially into the second half of fiscal 2024.

Image Source: Zacks Investment Research

This Zacks Rank #3 (Hold) company expects modest earnings and margin improvements in fiscal 2024, mainly weighted to the second half. This reflects a moderating inflationary landscape, together with ongoing productivity enhancements. For fiscal 2024, adjusted EBIT is forecasted to be up 3-5%. Adjusted EPS is envisioned to increase 3-5% to the $3.09-$3.15 band.

Campbell Soup’s Snacks business has been a driver, which formed 44.2% of total sales in the first quarter of fiscal 2024. Net sales in the division rose 1% on an organic basis, attributed to sales of power brands, which rose 5%.

Sales growth was fueled by a rise in cookies and crackers, specifically Goldfish crackers and Lance sandwich crackers. Favorable net price realization contributed to the upside, which was partially offset by volume/mix declines. Management’s DSD transformation initiative is expected to fuel further growth and margins in the Snacks division.

Cost Headwinds & More

Campbell Soup has been witnessing cost inflation for a while. The company expects core inflation to stay in the low-single-digit range in fiscal 2024 compared with 12% in fiscal 2023. Apart from this, adjusted marketing and selling expenses rose 9% to $220 million in the first quarter due to a 6% increase in advertising and consumer promotion expenses. The persistence of these trends could hurt margins.

Apart from this, the company is navigating a volatile consumer landscape. This affected first-quarter fiscal 2024 results, wherein organic net sales dipped 1% due to the soft volume/mix (down 5%), somewhat offset by net price realization (up 3%). For fiscal 2024, organic sales growth is likely to come between flat and an increase of 2%. Although management expects sequential improvements in fiscal 2024, it expects volumes to decline in the first half.

Wrapping Up

Despite the abovementioned headwinds, Campbell Soup looks well-placed due to its strategic priorities and savings plan. The company’s strategy of concentrating on supply-chain efficiencies, along with curtailing costs and reinvesting part of these savings in areas with high-growth potential, is noteworthy.

Through the first quarter of fiscal 2024, CPB generated $895 million in savings under its multi-year cost-saving program, including Snyder’s-Lance synergies. Management remains on track to deliver savings worth $1 billion by the fiscal 2025-end.

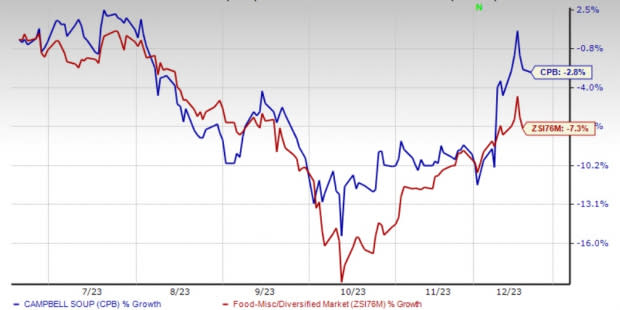

The company’s shares have decreased 2.8% in the past six months compared with the industry’s decline of 7.3%.

3 Appetizing Picks

The Kraft Heinz Company KHC, a food and beverage product company, currently carries a Zacks Rank #2 (Buy). KHC has a trailing four-quarter earnings surprise of 9.9%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Kraft Heinz’s current financial-year sales and earnings suggests growth of 1.1% and 6.5%, respectively, from the year-ago reported numbers.

Celsius Holdings, Inc. CELH, which develops, processes, markets, distributes and sells functional drinks and liquid supplements, holds a Zacks Rank #2. CELH has a trailing four-quarter earnings surprise of 110.9%, on average.

The Zacks Consensus Estimate for Celsius Holdings’ current financial-year sales and earnings suggests growth of 98.5% and 184.1%, respectively, from the year-ago reported numbers.

Vital Farms Inc. VITL offers a range of produced pasture-raised foods. It currently has a Zacks Rank #2. VITL has a trailing four-quarter earnings surprise of 145%, on average.

The Zacks Consensus Estimate for Vital Farms’ current financial-year sales suggests growth of 29.4% from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Campbell Soup Company (CPB) : Free Stock Analysis Report

Kraft Heinz Company (KHC) : Free Stock Analysis Report

Celsius Holdings Inc. (CELH) : Free Stock Analysis Report

Vital Farms, Inc. (VITL) : Free Stock Analysis Report