Canada Goose Stock (NYSE:GOOS): Benefit from Luxury Industry Panic

Canada Goose Stock (NYSE:GOOS) is traversing a challenging landscape due to investor panic within the luxury industry. Renowned for its opulent parkas, Toronto-based Canada Goose has seen its stock dip by 46% in the past year despite the overall market recording noteworthy gains during the same period. This is due to a prevailing industry outlook that appears grim. Nevertheless, Canada Goose continues to post solid results, while the stock’s forward valuation appears attractive. Thus, I’m bullish on the stock.

What’s the Current Luxury Industry Outlook?

The prevailing narrative surrounding the luxury industry’s future outlook has displayed signs of weakness in recent months. Despite a surge in consumer spending on luxury goods after COVID-19, there is a rising expectation among industry experts that this trend might see a reversal in 2024.

Examining potential indicators, data from Bank of America (NYSE:BAC) in October revealed a persistent decline in card spending for luxury fashion in the U.S., with figures showing a continuous decrease for six consecutive quarters. Specifically, luxury fashion spending witnessed a 16% year-over-year drop in the preceding quarter (Q3).

While the data for Q4 will unveil whether this trend persisted during the holiday season, lingering concerns, especially in the U.S. market, remain. Resilient spending habits could undergo a reversal, influenced by factors such as the resumption of student loan payments and the shortage of savings hoarded during 2020-2021.

Fears about diminishing expenditure on luxury goods are also tied to economic challenges in China. As the world’s second-largest economy, previously a substantial buyer of luxury items, faces reports of lagging consumer demand, the global luxury market is impacted.

The impact of these concerns is clearly reflected in the lackluster performance of luxury brand stocks over the past few quarters. While I previously stressed the hurdles encountered by Canada Goose, investors’ unease regarding the luxury sector becomes particularly evident when looking at the performance of the industry bellwether LVMH Moët Hennessy – Louis Vuitton (FR:MC). The largest luxury powerhouse in the world has seen its shares lose nearly a quarter of their value from their 52-week high of €895.80.

Consensus Estimates Tell a Different Story

Despite mainstream outlets reporting on a bleak luxury industry outlook and investors’ fear being clearly evident in the decline of luxury brand stocks, consensus estimates tell a different story. Again, being the largest company in the space, LVMH makes for a nice example. Despite the stock’s slip due to industry concerns, consensus estimates point toward growing revenues and profits.

Specifically, the Paris-based industry behemoth posted sales of €79.2 billion in Fiscal 2022. Yet, the market expects LVMH to have ended Fiscal 2023 with sales of nearly €86 billion, while sales in Fiscal 2024 are expected to rise further to €91.6 billion. This trend can also be seen in other luxury powerhouses such as Hermes International (FR:RMS).

But What About Canada Goose?

While my discussion of Canada Goose may seem delayed, the purpose of presenting the preceding information is to underscore my belief that, regardless of the seemingly pessimistic industry outlook, Canada Goose stands out as an undervalued stock.

Even when considering Canada Goose’s consensus estimates, which align with the prevailing gloomy industry sentiment, the stock remains an enticing prospect. Specifically, Wall Street anticipates a nearly 20% decline in EPS to $0.62 for the fiscal year ending March 2024. This downturn is attributed to a faster expense increase compared to the expected 6.2% growth (implying a growth slowdown) in revenue for the year.

However, it’s crucial to note that this anticipated slowdown is projected to be temporary. Wall Street foresees Canada Goose’s revenue growth bouncing back by 12% in Fiscal 2025, accompanied by a 28.6% increase in EPS from Fiscal 2024’s estimate to $0.80.

At a modest 14.7x Fiscal 2025 “normalized” EPS, Canada Goose appears remarkably undervalued, given its promising growth prospects and the potential for margin expansion due to the recent shift toward Direct-to-Consumer sales over Wholesale channels. For context, Canada Goose’s DTC sales rose 15% to C$109.4 million in Fiscal Q2 2024, gaining share over Wholesale revenue, which fell by 10% to C$162 million. This shift raised gross margins from 59.8% last year to 63.9%.

In the meantime, even following the recent investor sell-offs in most luxury brand stocks, Canada Goose stands out with a notably lower valuation than industry leaders. For instance, Hermes International and LVMH continue to trade at forward P/Es of about 44 and 21, respectively, maintaining their customary premium multiples. This contrast emphasizes Canada Goose’s potential allure and value proposition in the current market landscape.

Is GOOS Stock a Buy, According to Analysts?

Regarding Wall Street’s sentiment on the stock, Canada Goose features a Hold consensus rating based on one Buy, nine Holds, and one Sell assigned in the past three months. Clearly, analysts continue to price in the grim scenario here. At $11.40, the average GOOS stock forecast implies 4.3% more downside potential.

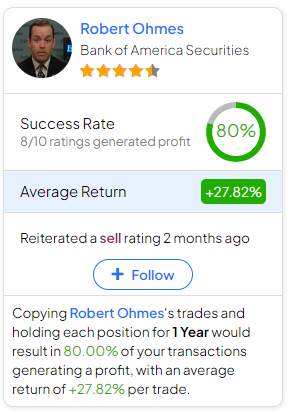

If you’re wondering which analyst you should follow if you want to buy and sell GOOS stock, the most profitable analyst covering the stock (on a one-year timeframe) is Robert Ohmes from Bank of America Securities, with an average return of 27.82% per rating and an 80% success rate. Click on the image below to learn more.

The Takeaway

Overall, while the luxury industry grapples with uncertainties, Canada Goose appears to be a compelling pick in the space. Despite the ongoing industry concerns reflected in the stock’s slip, forward consensus estimates and the company’s strategic shift towards Direct-to-Consumer sales form an attractive narrative of profitable growth ahead.

The temporary projected slowdown in Fiscal 2024’s EPS is outweighed by optimistic Fiscal 2025 estimates, resulting in Canada Goose appearing undervalued today, especially as industry bellwethers maintain premium valuations.