What Canadian Utilities Limited's (TSE:CU) P/E Is Not Telling You

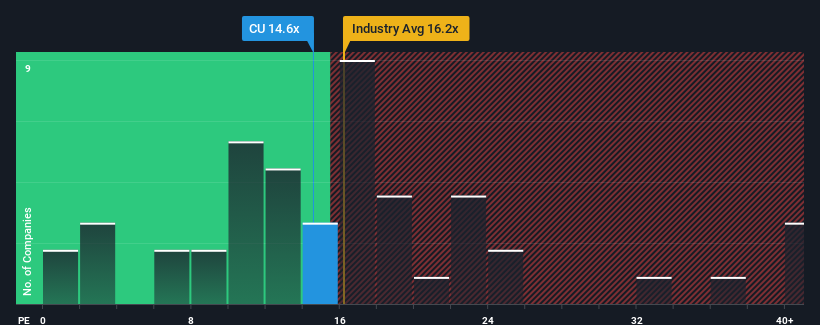

With a price-to-earnings (or "P/E") ratio of 14.6x Canadian Utilities Limited (TSE:CU) may be sending bearish signals at the moment, given that almost half of all companies in Canada have P/E ratios under 12x and even P/E's lower than 5x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's as high as it is.

Canadian Utilities has been doing a reasonable job lately as its earnings haven't declined as much as most other companies. The P/E is probably high because investors think this comparatively better earnings performance will continue. While you'd prefer that its earnings trajectory turned around, you'd at least be hoping it remains less negative than other companies, otherwise you're paying a pretty hefty price for no particular reason.

See our latest analysis for Canadian Utilities

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Canadian Utilities.

Is There Enough Growth For Canadian Utilities?

There's an inherent assumption that a company should outperform the market for P/E ratios like Canadian Utilities' to be considered reasonable.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. However, a few strong years before that means that it was still able to grow EPS by an impressive 46% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 4.3% during the coming year according to the six analysts following the company. With the market predicted to deliver 12% growth , the company is positioned for a weaker earnings result.

In light of this, it's alarming that Canadian Utilities' P/E sits above the majority of other companies. Apparently many investors in the company are way more bullish than analysts indicate and aren't willing to let go of their stock at any price. There's a good chance these shareholders are setting themselves up for future disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

Using the price-to-earnings ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our examination of Canadian Utilities' analyst forecasts revealed that its inferior earnings outlook isn't impacting its high P/E anywhere near as much as we would have predicted. Right now we are increasingly uncomfortable with the high P/E as the predicted future earnings aren't likely to support such positive sentiment for long. This places shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

We don't want to rain on the parade too much, but we did also find 2 warning signs for Canadian Utilities (1 is a bit unpleasant!) that you need to be mindful of.

If these risks are making you reconsider your opinion on Canadian Utilities, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.