CarMax (NYSE:KMX) Misses Q3 Sales Targets, But Stock Soars 5.1%

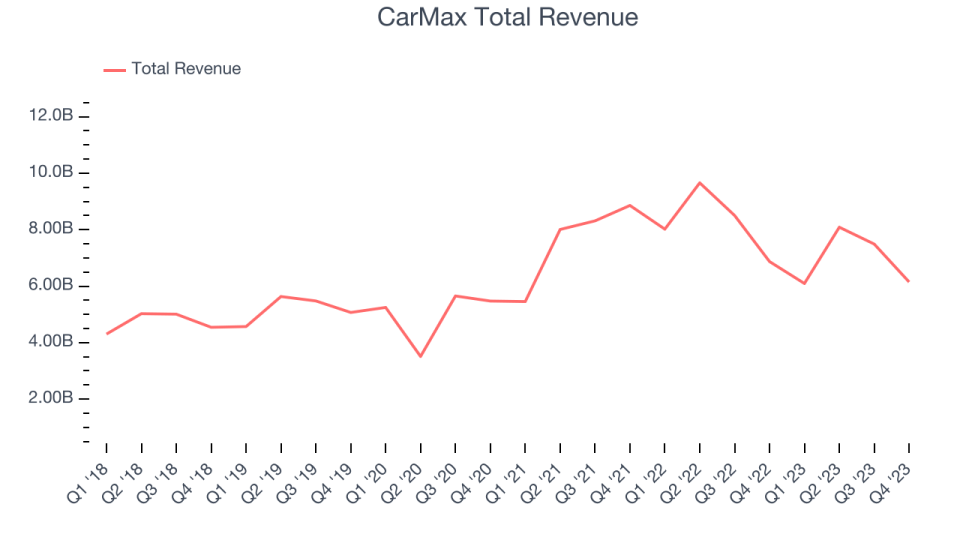

Used automotive vehicle retailer Carmax (NYSE:KMX) fell short of analysts' expectations in Q3 FY2024, with revenue down 10.5% year on year to $6.15 billion. It made a GAAP profit of $0.52 per share, improving from its profit of $0.24 per share in the same quarter last year.

Key Takeaways from CarMax's Q3 Results

We were impressed by how significantly CarMax blew past analysts' EPS expectations this quarter due to a more efficient expense base that resulted from cost reduction efforts. Higher-than-expected operating margin and the resulting EPS beat stood out as positives in these results. However, its revenue unfortunately missed analysts' expectations. Zooming out, we know that expectations have been low for the used car industry, and CarMax reported better-than-feared results. The stock is up 5.6% after reporting and currently trades at $78.89 per share.

Is now the time to buy CarMax? Find out by accessing our full research report, it's free.

CarMax (KMX) Q3 FY2024 Highlights:

Market Capitalization: $11.85 billion

Revenue: $6.15 billion vs analyst estimates of $6.30 billion (2.5% miss)

EPS: $0.52 vs analyst estimates of $0.41 (27.2% beat)

Free Cash Flow of $64.82 million, down 93.9% from the same quarter last year

Gross Margin (GAAP): 10%, down from 10.6% in the same quarter last year

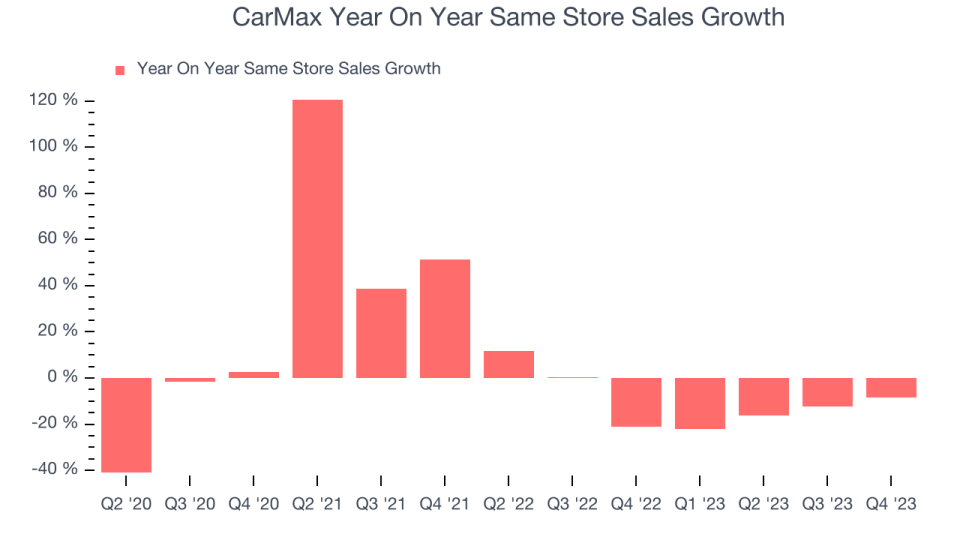

Same-Store Sales were down 8.3% year on year (miss)

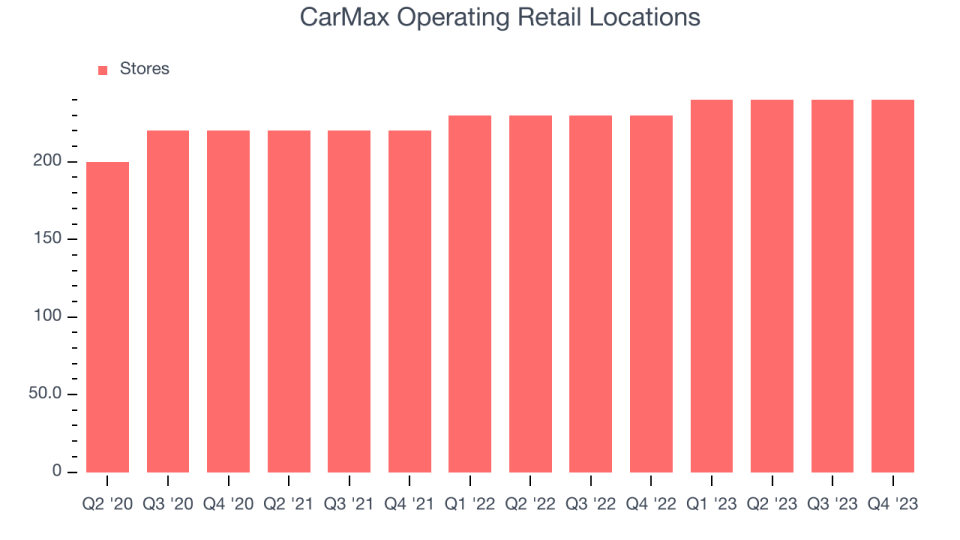

Store Locations: 240 at quarter end, increasing by 10 over the last 12 months

“Our third quarter performance reflects the continued efforts of the team that have resulted in several quarters of sequential improvements across key components of our business, despite the persistent widespread pressures in the used car industry,” said Bill Nash, president and chief executive officer.

Known for its transparent, customer-centric approach and wide selection of vehicles, Carmax (NYSE:KMX) is the largest automotive retailer in the United States.

Vehicle Retailer

Buying a vehicle is a big decision and usually the second-largest purchase behind a home for many people, so retailers that sell new and used cars try to offer selection, convenience, and customer service to shoppers. While there is online competition, especially for research and discovery, the vehicle sales market is still very fragmented and localized given the magnitude of the purchase and the logistical costs associated with moving cars over long distances. At the end of the day, a large swath of the population relies on cars to get from point A to point B, and vehicle sellers are acutely aware of this need.

Sales Growth

CarMax is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

As you can see below, the company's annualized revenue growth rate of 7.6% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was decent as it opened new stores and expanded its reach.

This quarter, CarMax missed Wall Street's estimates and reported a rather uninspiring 10.5% year-on-year revenue decline, generating $6.15 billion in revenue. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Our recent pick has been a big winner, and the stock is up more than 2,000% since the IPO a decade ago. If you didn’t buy then, you have another chance today. The business is much less risky now than it was in the years after going public. The company is a clear market leader in a huge, growing $200 billion market. Its $7 billion of revenue only scratches the surface. Its products are mission critical. Virtually no customers ever left the company. You can find it on our platform for free.

Number of Stores

The number of stores a retailer operates is a major determinant of how much it can sell, and its growth is a critical driver of how quickly company-level sales can grow.

When a retailer like CarMax is opening new stores, it usually means it's investing for growth because demand is greater than supply. Since last year, CarMax's store count increased by 10 locations, or 4.3%, to 240 total retail locations in the most recently reported quarter.

Over the last two years, the company has generally opened new stores and averaged 4.4% annual growth in its physical footprint, which is decent and on par with the broader sector. With an expanding store base and demand, revenue growth can come from multiple vectors: sales from new stores, sales from e-commerce, or increased foot traffic and higher sales per customer at existing stores.

Same-Store Sales

CarMax's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 9.7% year on year. This performance is quite concerning and the company should reconsider its strategy before investing its precious capital into new store buildouts.

In the latest quarter, CarMax's same-store sales fell 8.3% year on year. This decrease was an improvement from the 21% year-on-year decline it posted 12 months ago. It's always great to see a business improve its prospects.

So should you invest in CarMax right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.