Cars.com (CARS): A Thorough Examination of Its Modest Overvaluation

As of September 15, 2023, Cars.com Inc (NYSE:CARS) experienced a daily loss of 4.9%, marking a 3-month loss of 6.14%. Despite an Earnings Per Share (EPS) of 1.65, the stock appears to be modestly overvalued. This article delves into the valuation analysis of Cars.com Inc, providing a comprehensive understanding of the company's financial standing.

Company Overview

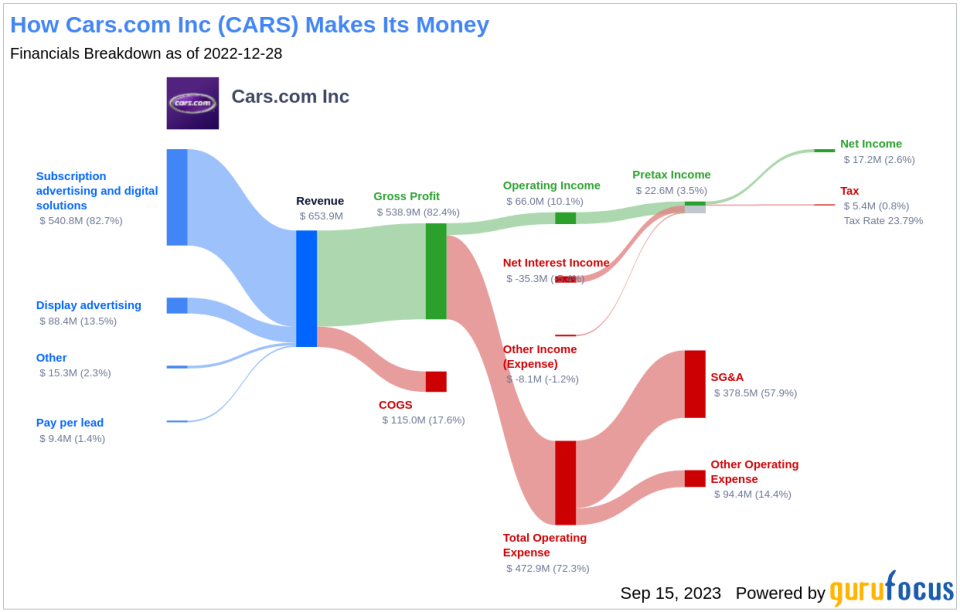

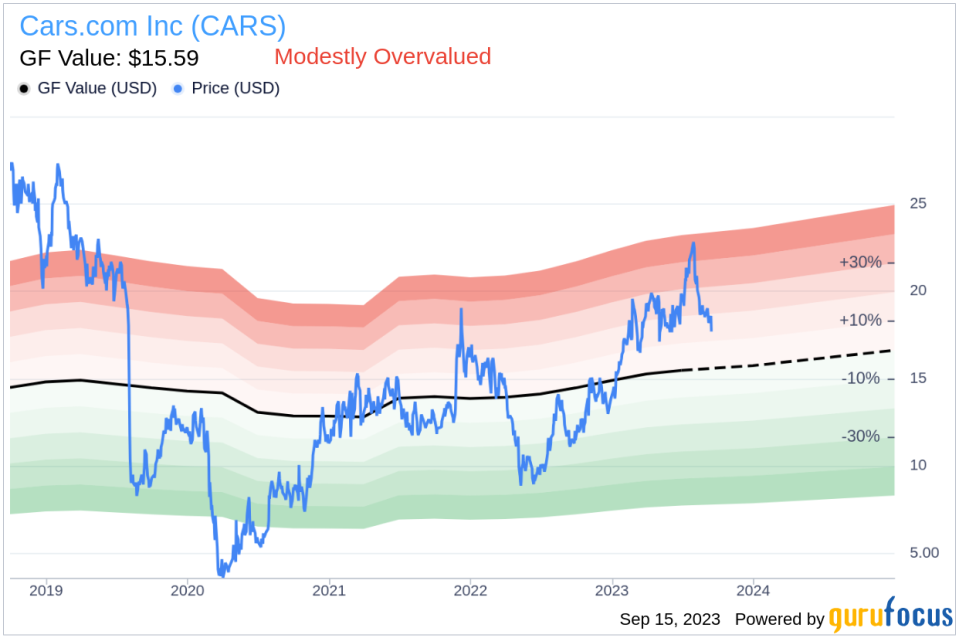

Cars.com Inc is a prominent online platform for buying and selling new and used vehicles. The company operates several brands, including Dealer Inspire, DealerRater, FUEL, Accu-Trade, PickupTrucks.com, CreditIQ, and NewCars.com, each catering to different consumer segments. With a market capitalization of $1.20 billion and sales worth $668 million, the stock's current price stands at $17.67, which is slightly higher than the GF Value of $15.59.

Understanding the GF Value

The GF Value is a unique measure of a stock's intrinsic value, calculated based on historical trading multiples, a GuruFocus adjustment factor, and future business performance estimates. If the stock price is significantly above the GF Value Line, it indicates overvaluation and potentially poor future returns. Conversely, if it is significantly below the GF Value Line, it suggests undervaluation and potentially higher future returns.

Based on our valuation method, Cars.com (NYSE:CARS) appears to be modestly overvalued. This overvaluation suggests that the long-term return of its stock is likely to be lower than its business growth.

Financial Strength

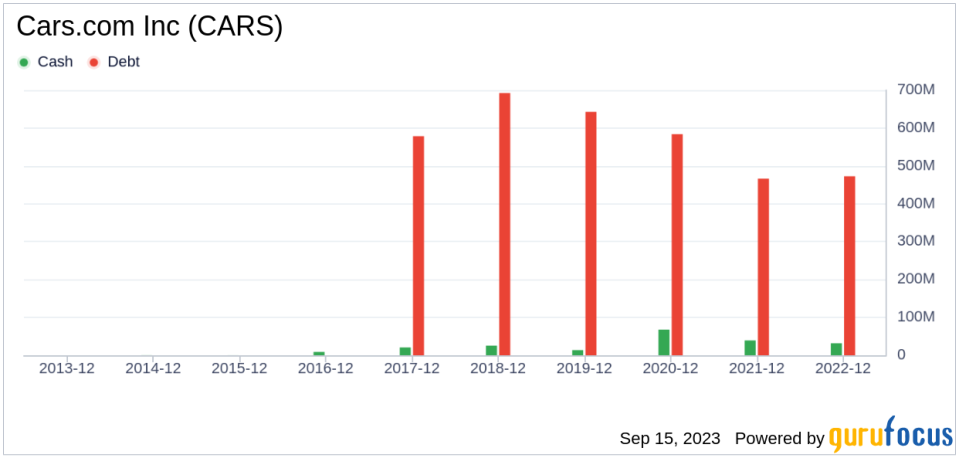

Investing in companies with poor financial strength carries a higher risk of permanent capital loss. Therefore, understanding a company's financial strength is crucial before deciding to buy its stock. Cars.com has a cash-to-debt ratio of 0.06, which is worse than 90.43% of 1223 companies in the Vehicles & Parts industry. This ratio indicates that the financial strength of Cars.com is poor.

Profitability and Growth

Consistent profitability over the long term reduces investment risks. Cars.com has been profitable 8 out of the past 10 years. With an operating margin of 9.67%, the company's profitability is fair. However, Cars.com's growth is worse than 67.03% of 1201 companies in the Vehicles & Parts industry, indicating a need for improvement.

ROIC vs WACC

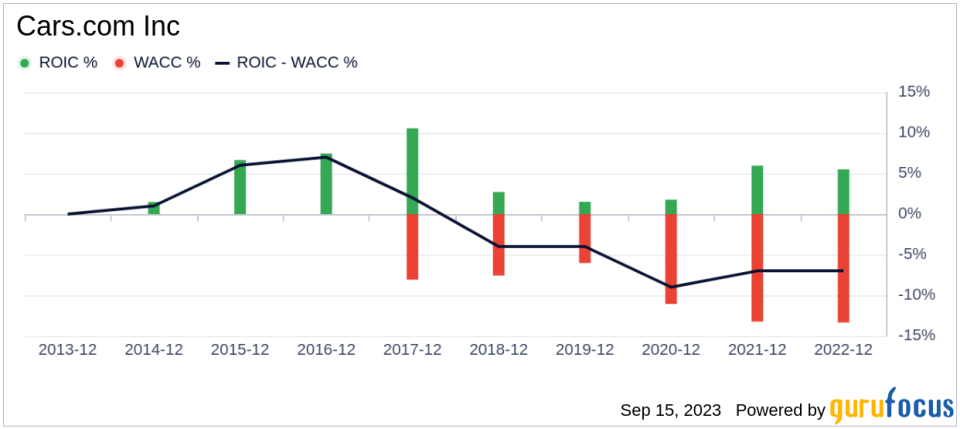

Comparing a company's return on invested capital (ROIC) to its weighted average cost of capital (WACC) can also evaluate its profitability. If the ROIC exceeds the WACC, the company is likely creating value for its shareholders. Over the past 12 months, Cars.com's ROIC was 27.61, while its WACC was 12.44, suggesting a positive value creation.

Conclusion

In conclusion, Cars.com (NYSE:CARS) appears to be modestly overvalued. Despite its fair profitability, the company's financial condition is poor, and its growth ranks worse than most companies in the Vehicles & Parts industry. For more detailed financial information about Cars.com, check out its 30-Year Financials here.

For a list of high-quality companies that may deliver above-average returns, visit the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.