Casey's (CASY) Expands Horizons Through Operational Efforts

Casey's General Stores, Inc. CASY has been strengthening its place in the industry through a resilient business operating model, stellar omnichannel capabilities, expanded customer outreach, and exclusive private-label offerings. Driven by an unwavering commitment to guest-centered convenience and restaurant-quality food, Casey's endeavors to carve out a unique niche in the market.

Decoding Casey's Strategies

Casey's shines brightly in the retail landscape, thanks to its ingenious pricing and product optimization strategies, successful expansion of private brands and adept digital engagement through mobile apps and online ordering systems. Ranked as the third-largest convenience retailer and the fifth-largest pizza chain, Casey's self-distribution strategy, strong performance in the Inside category and strategic acquisitions indicate a promising future.

Casey’s focus on technology advancements, merchandise ordering efficiency, inventory management and data analytics positions it well for future growth. The company has been strengthening pizza promotions for guests seeking meal solutions, along with enhancing breakfast lineups. Casey’s Rewards, the company's flagship loyalty program, has proven to be a vital tool for guest engagement.

With a strategic vision to expand, Casey's aims to add 350 stores by the end of fiscal 2026, ensuring that each store is strategically positioned and stocked with the right products to meet customer demands. This growth strategy seamlessly blends organic expansion and strategic acquisitions.

Image Source: Zacks Investment Research

A Glimpse Into Casey's Success

In the first quarter of fiscal 2024, Casey's demonstrated strength with a surge in Inside sales. The metric grew 8.1% to $1,369.7 million during the quarter. The growth was not just quantitative but qualitative as well, with Inside same-store sales witnessing an increase of 5.4%.

This was driven by a stellar performance in the Prepared Food & Dispensed Beverage category, including whole pizza pies, hot sandwiches and donuts as well as non-alcoholic and alcoholic beverages, snacks and candy in the Grocery & General Merchandise category.

Grocery & General Merchandise sales saw a notable 8% increase, totaling $997 million, while Prepared Food & Dispensed Beverage sales grew 8.5% to reach $372.8 million in the quarter.

Charting the Path Ahead

Casey’s business model, private-label offerings, expansion of its footprint and digitization endeavors are likely to support sales. The company estimates Inside same-store sales to increase between 3% and 5% in fiscal 2024. Additionally, it anticipates maintaining an Inside margin within the range of 40%-41%, promising a healthy financial outlook.

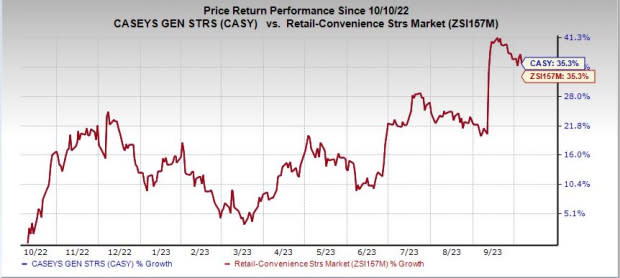

Investors have recognized its potential, with shares of this Zacks Rank #2 (Buy) company rising an impressive 35.3% in the past year, aligning with the industry’s growth.

3 More Stocks Looking Red Hot

Here, we have highlighted three other top-ranked stocks, namely Grocery Outlet GO, Ross Stores ROST and Walmart WMT.

Grocery Outlet, an extreme value retailer of quality, name-brand consumables and fresh products, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Grocery Outlet’s current financial-year sales and earnings suggests growth of 11.2% and 4.9%, respectively, from the year-ago reported numbers. GO has a trailing four-quarter earnings surprise of 14.3%, on average.

Ross Stores, which operates off-price retail apparel and home fashion stores, currently sports a Zacks Rank #1. ROST has a trailing four-quarter earnings surprise of 11.4%, on average.

The Zacks Consensus Estimate for Ross Stores’ current financial-year sales and earnings indicates growth of 7.1% and 19.4%, respectively, from the year-ago reported numbers.

Walmart, which operates a chain of hypermarkets, discount department stores and grocery stores, currently carries a Zacks Rank #2. WMT has a trailing four-quarter earnings surprise of 11.6%, on average.

The Zacks Consensus Estimate for Walmart’s current financial-year sales and earnings implies growth of 5% and 2.2%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Casey's General Stores, Inc. (CASY) : Free Stock Analysis Report

Grocery Outlet Holding Corp. (GO) : Free Stock Analysis Report