CASI Pharmaceuticals, Inc.'s (NASDAQ:CASI) Price Is Right But Growth Is Lacking After Shares Rocket 33%

Despite an already strong run, CASI Pharmaceuticals, Inc. (NASDAQ:CASI) shares have been powering on, with a gain of 33% in the last thirty days. The annual gain comes to 256% following the latest surge, making investors sit up and take notice.

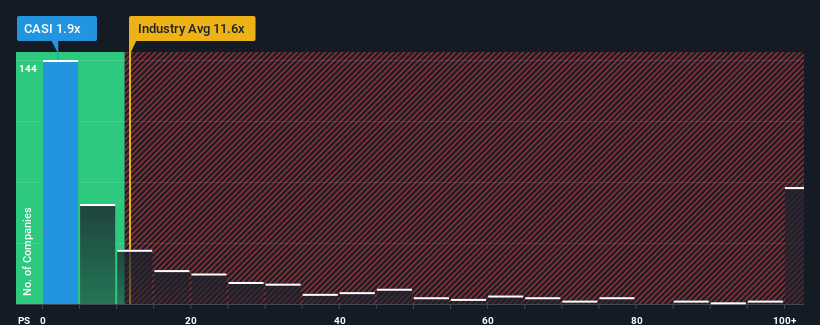

In spite of the firm bounce in price, CASI Pharmaceuticals' price-to-sales (or "P/S") ratio of 1.9x might still make it look like a strong buy right now compared to the wider Biotechs industry in the United States, where around half of the companies have P/S ratios above 11.6x and even P/S above 49x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

See our latest analysis for CASI Pharmaceuticals

How CASI Pharmaceuticals Has Been Performing

With revenue growth that's inferior to most other companies of late, CASI Pharmaceuticals has been relatively sluggish. It seems that many are expecting the uninspiring revenue performance to persist, which has repressed the growth of the P/S ratio. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Want the full picture on analyst estimates for the company? Then our free report on CASI Pharmaceuticals will help you uncover what's on the horizon.

Is There Any Revenue Growth Forecasted For CASI Pharmaceuticals?

CASI Pharmaceuticals' P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 14%. Pleasingly, revenue has also lifted 262% in aggregate from three years ago, partly thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing revenues over that time.

Looking ahead now, revenue is anticipated to climb by 38% each year during the coming three years according to the one analyst following the company. That's shaping up to be materially lower than the 221% per annum growth forecast for the broader industry.

In light of this, it's understandable that CASI Pharmaceuticals' P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Final Word

Even after such a strong price move, CASI Pharmaceuticals' P/S still trails the rest of the industry. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that CASI Pharmaceuticals maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. The company will need a change of fortune to justify the P/S rising higher in the future.

And what about other risks? Every company has them, and we've spotted 2 warning signs for CASI Pharmaceuticals (of which 1 is a bit unpleasant!) you should know about.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.