Caterpillar (CAT) Q2 Earnings & Revenues Beat Estimates, Up Y/Y

Caterpillar Inc. CAT reported record adjusted earnings per share of $5.55 in the second quarter of 2023, which beat the Zacks Consensus Estimate of adjusted earnings per share of $4.51 by a margin of 23%. The bottom-line figure marked a 74.5% improvement year on year. Despite unfavorable manufacturing costs, higher sales volumes and favorable price realization led to the solid improvement in CAT’s earnings for the quarter.

Including one-time items, Caterpillar’s earnings per share was $5.67, up 81% from the prior-year quarter’s figure of $3.13.

Revenues Up on High Volumes & Prices

The company reported second-quarter revenues of around $17.3 billion, which surpassed the Zacks Consensus Estimate of $16.5 billion. The top line improved 22% from the year-ago quarter, aided by higher sales volumes and favorable price realization. Sales growth was noted across all segments, led by 32% growth in North America.

Caterpillar Inc. Price, Consensus and EPS Surprise

Caterpillar Inc. price-consensus-eps-surprise-chart | Caterpillar Inc. Quote

Higher Sales Offset Cost Impact on Margins

In the quarter under review, the cost of sales increased 11% year over year to around $11 billion. Manufacturing costs were higher in the quarter, reflecting inflated material costs. Gross profit improved 46% year over year to $6.25 billion on higher sales. The gross margin was 36.1% in the quarter under review, up from 30% in the prior-year quarter.

Selling, general and administrative (SG&A) expenses increased 7% year over year to around $1,528 million. Research and development expenses were up 10% to $528 million. This was mainly due to CAT’s investments aligned with strategic initiatives.

CAT reported an operating profit of $3,652 million in the second quarter of 2023, compared with $1,944 million in the last year’s quarter. Gains from increased volumes and favorable price realization offset higher costs, leading to an 88% year-over-year jump in profits.

The operating margin was 21.1% in the reported quarter, up from 13.6% in the prior-year quarter. Adjusted operating profit was $3,683 million in the quarter, up 87% from $1,972 million in the last year’s quarter. The adjusted operating margin was 21.3% in the second quarter of 2023 versus 13.8% in the year-ago quarter.

Solid Segment Performances

Machinery and Energy & Transportation (ME&T) sales rose 22% year over year to $16.5 billion in the quarter under review. Construction Industries' sales were up 19% year over year to $7.2 billion on favorable price realization and higher sales volumes. Sales were up 32% in North America and 20% in EAME. Sales were flat in Asia/Pacific and declined 11% in Latin America.

The segment’s external sales were higher than our estimate of $6,553 million, which had factored in a volume and pricing growth of 3% and 6%, respectively, for the quarter. Volume growth of 10.1% and favorable price impact of 10.5% were thus higher than our projections, leading to the variance.

Sales in the Resource Industries segment gained 20% year over year to around $3.6 billion on higher sales volume and improved price realization. The segment witnessed higher sales of equipment to end users, which was offset by lower aftermarket parts sales volume. Growth was noted across all regions, led by North America with year-over-year growth of 31%, followed by Asia/Pacific registering 18% growth. Latin America and EAME delivered growth of 15% and 6%, respectively.

The segment’s second-quarter sales came in higher than our projection of $3,449.5 million. We had expected volume and pricing to contribute 12% and 8%, respectively, to the revenue growth in the quarter. Volume growth was reported at 9% and pricing impact was 13%.

Sales of the Energy & Transportation segment in the quarter were around $7.2 billion, reflecting growth of 27% aided by improved sales in all regions on higher sales volume and favorable price realization. The segment reported sales growth across all applications, which are Oil and Gas (43%), Power Generation (39%) Industrial (18%) and Transportation (12%).

For the Energy & Transportation segment, our sales estimate was $5.5 million, with volume growth at 15% and pricing at 4%. The reported volume and pricing growth were in line with our estimates. The variance was mainly due to the lower-than-expected impact of currency.

The ME&T segment reported an operating profit of $3,550 million, which reflected an improvement of 97% year over year. The Construction Industries segment witnessed an 82% surge in operating profit to $1,803 million. The Resource Industries segment’s operating profit soared 108% year over year to $740 million in the second quarter. The Energy & Transportation segment’s operating profit increased 93% year over year to $1,269 million. Favorable price realization and volumes across all segments helped offset the impact of higher costs, resulting in the improvement in respective segments’ profits.

Financial Products’ total revenues climbed 16% to $923 million from the prior-year quarter due to higher average financing rates. The segment's profits were $240 million in the reported quarter, which was 11% higher than the last year, due to lower provision for credit losses at Cat Financial. However, higher SG&A expenses had a somewhat offsetting impact.

Cash Position

During the first half of 2023, Caterpillar’s operating cash flow was $4.8 billion, compared with $2.5 billion in the prior-year period. Through the quarter, the company returned $2 billion to shareholders as dividends and share repurchases. CAT ended the reported quarter with cash and equivalents of around $7.4 billion.

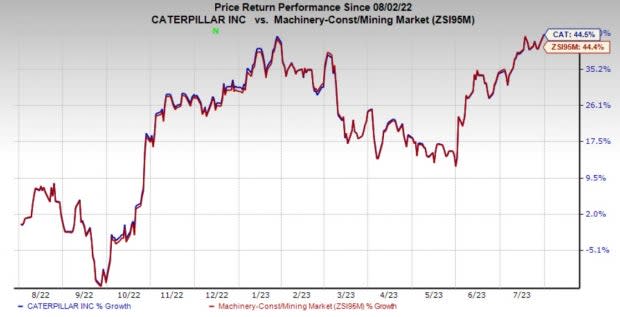

Price Performance

Over the past year, Caterpillar stock has gained 44.5%, compared with the industry’s 44.4% growth.

Image Source: Zacks Investment Research

Zacks Rank & Other Stocks to Consider

Caterpillar currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Some other top-ranked stocks from the Industrial Products sector are Worthington Industries, Inc. WOR, The Manitowoc Company, Inc. MTW, and W.W. Grainger, Inc. GWW. WOR and MTW sport a Zacks Rank of 1 at present and GWW has a Zacks Rank #2 (Buy).

Worthington Industries has an average trailing four-quarter earnings surprise of 14.9%. The Zacks Consensus Estimate for WOR’s fiscal 2023 earnings is pegged at $5.65 per share. The consensus estimate for 2023 earnings has moved 22.6% north in the past 60 days. Its shares have gained 52% in the last year.

Manitowoc has an average trailing four-quarter earnings surprise of 256.3%. The Zacks Consensus Estimate for MTW’s 2023 earnings is pegged at $1.12 per share. The consensus estimate for 2023 earnings has moved 7.8% north in the past 60 days. MTW’s shares have gained 58% in the last year.

The Zacks Consensus Estimate for Grainger’s 2023 earnings per share is pegged at $35.86, up 1% in the past 60 days. It has a trailing four-quarter average earnings surprise of 9.1%. GWW has gained 56% in the last year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Manitowoc Company, Inc. (MTW) : Free Stock Analysis Report

Caterpillar Inc. (CAT) : Free Stock Analysis Report

Worthington Industries, Inc. (WOR) : Free Stock Analysis Report

W.W. Grainger, Inc. (GWW) : Free Stock Analysis Report