CB or PGR: Which P&C Insurer Should You Buy for Higher Returns?

Increased exposure, streamlined operations, global presence, better pricing, solid underwriting, and a strong capital position have helped the Zacks Property and Casualty Insurance industry perform well. The industry has risen 12.2% year to date compared with the Zacks S&P 500 composite and the Finance sector’s rise of 25.1% and 14.9%, respectively. Per Fitch Ratings, the industry is poised to perform well, banking on improved personal auto, lower claims and an increase in investment.

The performance of non-life insurers is affected by catastrophes. Per Gallagher Re, total economic losses were estimated to be $290 billion in the first nine months of 2023. According to AM Best, total net underwriting loss was $32.2 billion in the first nine months of 2023, much higher than $24.6 billion incurred in the year-ago period, largely attributed to rising loss costs, above-average catastrophe activity and adverse trends in personal auto. The combined ratio was 103.5 for the same time frame, per the credit rating giant, to which catastrophe losses added 980 basis points.

Per a report in Insurance Journal, the combined net ratio in 2023 is estimated to be 102.2. The soft performance of personal lines, which are expected to witness higher catastrophe losses per Insurance Information Institute and Milliman, is expected to result in underwriting losses. Fitch estimates the combined ratio to remain above 100 in 2024.

An increase in catastrophe activities leads to a change in pricing. Global commercial insurance prices rose for 24 straight quarters, though the magnitude has slowed down, per Marsh Global Insurance Market Index. Improved pricing drives higher premiums, ensuring smooth claims settlement.

Per Deloitte Insights, gross premiums are estimated to increase about six-fold to $722 billion by 2030. China and North America should account for more than two-thirds of the global market, per the report. Per Fitch Ratings, personal auto is likely to deliver better performance in 2024. This, coupled with better investment results and lower claims, should fuel insurers' performance next year per Fitch Ratings.

The insurance industry benefits from a rising rate environment. Though the Fed paused rate hikes at its last three meetings in 2023, and there remains a high probability of rate cuts in 2024, the rate environment has improved over some time. The interest rate currently stands at 5.25-5.50%.

The industry is continually undergoing technological developments to improve scale and efficiency. While a solid policyholders’ surplus helps the industry absorb losses, a sturdy capital level supports inorganic expansion, investment in growth initiatives and capital payout to shareholders.

Here, we focus on two property and casualty insurers, namely Chubb Limited CB and The Progressive Corporation PGR. Chubb, with a market capitalization of $90.6 billion, is one of the world’s largest providers of property and casualty (P&C) insurance and reinsurance and the largest publicly traded P&C insurer based on market capitalization. Progressive Corporation, with a market capitalization of $92.1 billion, is a leading independent agency writer of private passenger auto coverage, and the market share leader in motorcycle products. The companies carry a Zacks Rank #2 (Buy) each. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Let’s now see how these P&C insurers fare in terms of some of the key metrics.

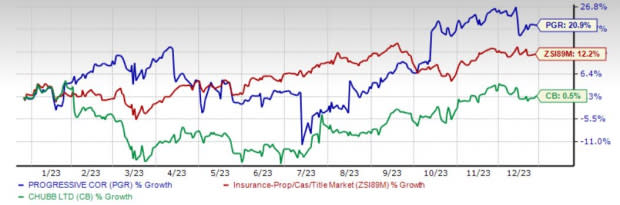

Price Performance

Progressive has gained 20.9% year to date compared with Chubb’s rise of 0.5%. The industry has risen 12.2% in the said time frame.

Image Source: Zacks Investment Research

Return on Equity

Progressive has a return on equity (“ROE”) of 17.4%, which exceeds Chubb’s ROE of 14.3% and the industry average of 7.2%. ROE measures how efficiently a company is utilizing its shareholders’ funds.

Return on Invested Capital

Return on invested capital (ROIC) is a profitability or performance ratio that aims to measure the percentage return that a company earns on invested capital. The ratio shows how efficiently a company is using investors' funds to generate income.

Progressive has an ROIC of 12.2%, which exceeds Chubb’s ROIC of 9% and the industry average of 5.5%.

Dividend Yield

Chubb’s dividend yield of 4% exceeds Progressive’s dividend yield of 0.3% and the industry average of 0.3%.

Debt-to-Equity Ratio

Progressive’s debt-to-equity ratio of 39.6 is higher than the industry average of 24 as well as Chubb’s reading of 30.

Growth Projection

The Zacks Consensus Estimate for CB’s 2024 earnings indicates a 7.4% increase from the year-ago estimated figure, while that for PGR implies a year-over-year increase of 51.7%.

The expected long-term earnings growth rate for CB is 10%, while that for PGR is 26.6%.

Combined Ratio

The combined ratio represents the underwriting profitability of an insurer. CB’s combined ratio for the first nine months of 2023 was 86.8, while the same for PGR was 97.2.

Net Margin

CB’s proforma net margin for the trailing 12 months was 14.7%, higher than PGR’s reading of 4.7%.

Valuation

CB shares are trading at a price-to-book value multiple of 1.58, lower than the PGR’s reading of 5.45. The industry average is 1.46.

To Conclude

Our comparative analysis shows that CB outpaces PGR in terms of dividend yield, combined ratio, net margin, valuation and leverage. PGR has the edge over CB with respect to price performance, return on equity, return on invested capital and growth projection.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Chubb Limited (CB) : Free Stock Analysis Report

The Progressive Corporation (PGR) : Free Stock Analysis Report