The CEO Of Flight Centre Travel Group Limited (ASX:FLT) Might See A Pay Rise On The Horizon

Key Insights

Flight Centre Travel Group will host its Annual General Meeting on 15th of November

Salary of AU$666.6k is part of CEO Skroo Turner's total remuneration

Total compensation is 75% below industry average

Flight Centre Travel Group's EPS grew by 79% over the past three years while total shareholder return over the past three years was 24%

Shareholders will probably not be disappointed by the robust results at Flight Centre Travel Group Limited (ASX:FLT) recently and they will be keeping this in mind as they go into the AGM on 15th of November. They will probably be more interested in hearing the board discuss future initiatives to further improve the business as they vote on resolutions such as executive remuneration. We have prepared some analysis below and we show why we think CEO compensation looks decent with even the possibility for a raise.

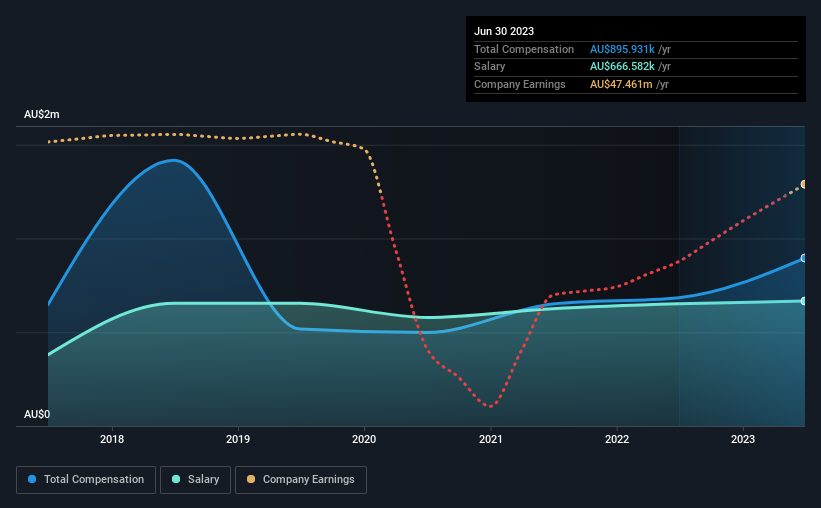

See our latest analysis for Flight Centre Travel Group

How Does Total Compensation For Skroo Turner Compare With Other Companies In The Industry?

At the time of writing, our data shows that Flight Centre Travel Group Limited has a market capitalization of AU$4.2b, and reported total annual CEO compensation of AU$896k for the year to June 2023. We note that's an increase of 31% above last year. We note that the salary portion, which stands at AU$666.6k constitutes the majority of total compensation received by the CEO.

On comparing similar companies from the Australian Hospitality industry with market caps ranging from AU$3.1b to AU$10.0b, we found that the median CEO total compensation was AU$3.6m. This suggests that Skroo Turner is paid below the industry median. Moreover, Skroo Turner also holds AU$321m worth of Flight Centre Travel Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2023 | 2022 | Proportion (2023) |

Salary | AU$667k | AU$651k | 74% |

Other | AU$229k | AU$33k | 26% |

Total Compensation | AU$896k | AU$684k | 100% |

On an industry level, around 57% of total compensation represents salary and 43% is other remuneration. Flight Centre Travel Group pays out 74% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Flight Centre Travel Group Limited's Growth Numbers

Flight Centre Travel Group Limited has seen its earnings per share (EPS) increase by 79% a year over the past three years. It achieved revenue growth of 126% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The combination of strong revenue growth with medium-term EPS improvement certainly points to the kind of growth we like to see. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Flight Centre Travel Group Limited Been A Good Investment?

Flight Centre Travel Group Limited has served shareholders reasonably well, with a total return of 24% over three years. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

To Conclude...

While the company seems to be headed in the right direction performance-wise, there's always room for improvement. Assuming the business continues to grow at a good clip, few shareholders would raise any objections to the CEO's remuneration. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. We did our research and spotted 2 warning signs for Flight Centre Travel Group that investors should look into moving forward.

Switching gears from Flight Centre Travel Group, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.