Children's Place (NASDAQ:PLCE) Q3 Sales Beat Estimates But Stock Drops 10.8%

Kid’s apparel and accessories retailer The Children’s Place (NASDAQ:PLCE) announced better-than-expected results in Q3 FY2023, with revenue down 5.7% year on year to $480.2 million. On top of that, next quarter's revenue guidance ($462.5 million at the midpoint) was surprisingly good and 6.3% above what analysts were expecting. Turning to EPS, Children's Place made a non-GAAP profit of $3.22 per share, down from its profit of $3.33 per share in the same quarter last year.

Is now the time to buy Children's Place? Find out by accessing our full research report, it's free.

Children's Place (PLCE) Q3 FY2023 Highlights:

Revenue: $480.2 million vs analyst estimates of $464.6 million (3.4% beat)

EPS (non-GAAP): $3.22 vs analyst expectations of $3.51 (8.3% miss)

Revenue Guidance for Q4 2023 is $462.5 million at the midpoint, above analyst estimates of $435.2 million

EPS (non-GAAP) Guidance for Q4 2023 is $0.35 at the midpoint, below analyst estimates of $1.30

Gross Margin (GAAP): 33.7%, down from 34.8% in the same quarter last year

Same-Store Sales were down 7.3% year on year (miss vs. expectations of down 5.9% year on year)

Store Locations: 591 at quarter end, decreasing by 67 over the last 12 months

Jane Elfers, President and Chief Executive Officer said, “Our Q3 results exceeded our expectations on the top line. The top line beat was driven by another quarter of industry-leading digital performance, fueled by a double digit increase in ecommerce traffic, with strong Back-to-School results in August and the success of our seasonal categories in September and October. And, our wholesale channel, led by Amazon, delivered another outstanding quarter. Importantly, our Q3 ending inventories were down 16%, exceeding our expectations. Our bottom-line results were negatively impacted in the third quarter by higher than planned distribution costs driven by a combination of largely unplanned but addressable factors. First, higher fulfillment costs, including the increased utilization of third party fulfillment services, stemming from shipping significantly more ecommerce units than planned due to higher volumes coupled with an outsized increase in packages resulting from lower transaction size as our consumer remains under pressure in the current environment. Second, significantly higher labor costs than planned due to the increased ecommerce demand and a very tight labor market. Third, a delay of certain planned freight and fulfillment savings. Looking ahead, we are planning for these increased distribution costs to continue in the fourth quarter.”

Offering sizes up to young teens, The Children’s Place (NASDAQ:PLCE) is a specialty retailer that sells its own brands of kid’s apparel and accessories.

Apparel Retailer

Apparel sales are not driven so much by personal needs but by seasons, trends, and innovation, and over the last few decades, the category has shifted meaningfully online. Retailers that once only had brick-and-mortar stores are responding with omnichannel presences. The online shopping experience continues to improve and retail foot traffic in places like shopping malls continues to stall, so the evolution of clothing sellers marches on.

Sales Growth

Children's Place is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

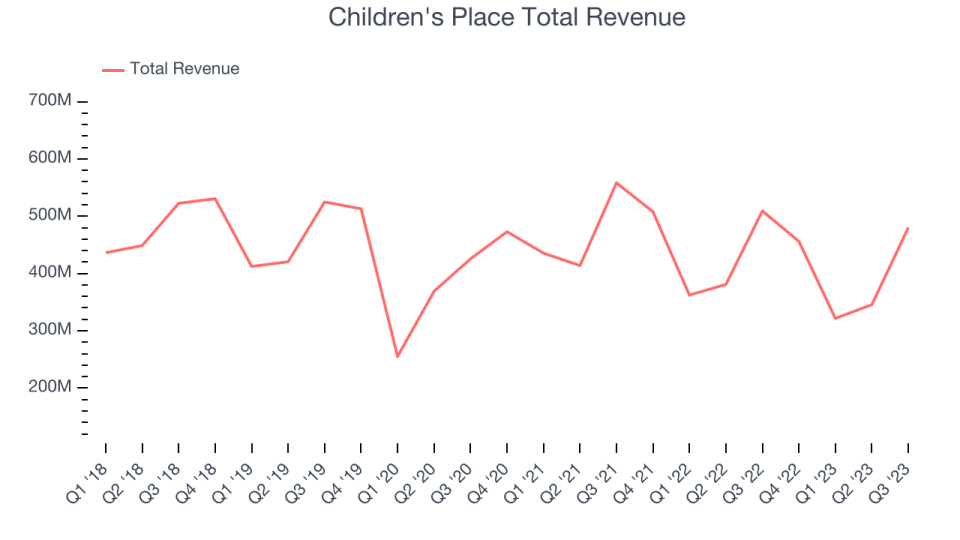

As you can see below, the company's revenue has declined over the last four years, dropping 4% annually as its store count and sales at existing, established stores have both shrunk.

This quarter, Children's Place's revenue fell 5.7% year on year to $480.2 million but beat Wall Street's estimates by 3.4%. The company is guiding for revenue to rise 1.4% year on year to $462.5 million next quarter, improving from the 10.2% year-on-year decrease it recorded in the same quarter last year. Looking ahead, analysts expect revenue to decline 4.4% over the next 12 months.

While most things went back to how they were before the pandemic, a few consumer habits fundamentally changed. One founder-led company is benefiting massively from this shift and is set to beat the market for years to come. The business has grown astonishingly fast, with 40%+ free cash flow margins, and its fundamentals are undoubtedly best-in-class. Still, its total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Number of Stores

A retailer's store count often determines on how much revenue it can generate.

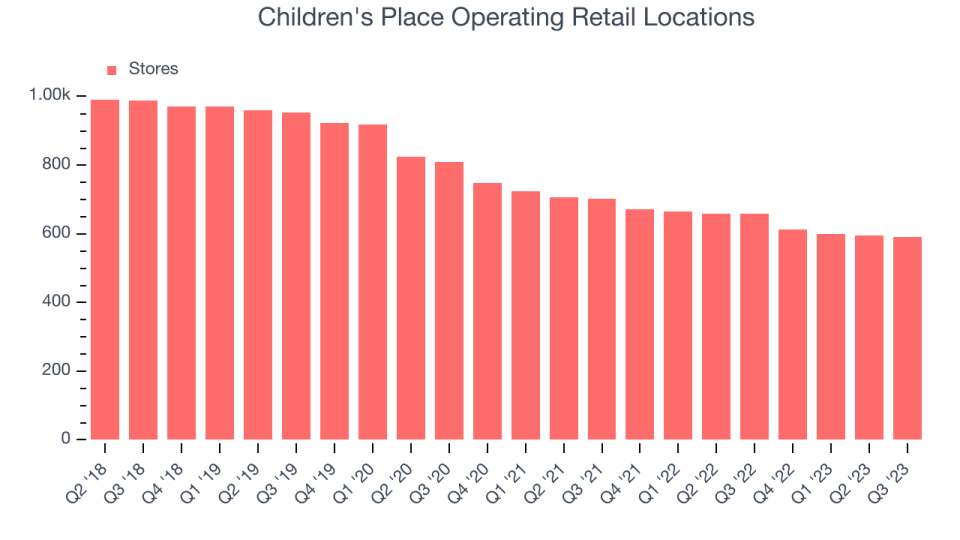

When a retailer like Children's Place is shuttering stores, it usually means that brick-and-mortar demand is less than supply, and the company is responding by closing underperforming locations and possibly shifting sales online. Children's Place's store count shrank by 67 locations, or 10.2%, over the last 12 months to 591 total retail locations in the most recently reported quarter.

Taking a step back, the company has generally closed its stores over the last two years, averaging a 8.8% annual decline in its physical footprint. A smaller store base means that the company must rely on higher foot traffic and sales per customer at its remaining stores as well as e-commerce sales to fuel revenue growth.

Same-Store Sales

Same-store sales growth is an important metric that tracks demand for a retailer's established brick-and-mortar stores and e-commerce platform.

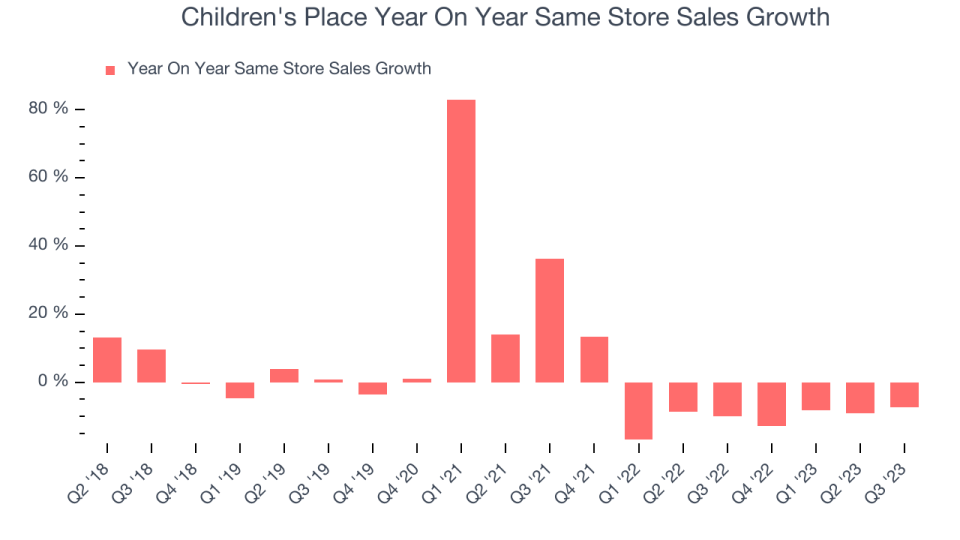

Children's Place's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 7.5% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Children's Place's same-store sales fell 7.3% year on year. This decrease was a further deceleration from the 10% year-on-year decline it posted 12 months ago. We hope the business can get back on track.

Key Takeaways from Children's Place's Q3 Results

With a market capitalization of $356.4 million and more than $13.52 million in cash on hand, Children's Place can continue prioritizing growth.

This was a mixed but overall weaker quarter. Management said that "bottom-line results were negatively impacted...by higher than planned distribution costs driven by a combination of largely unplanned but addressable factors. First, higher fulfillment costs...Second, significantly higher labor costs...Third, a delay of certain planned freight and fulfillment savings. Looking ahead, we are planning for these increased distribution costs to continue in the fourth quarter.”

Same-store sales missed. While revenue guidance for next quarter was ahead, full-year earnings forecast underwhelmed. Overall, the results could have been better and shows the company is under pressure from a cost perspective. The company is down 11.7% on the results and currently trades at $25.25 per share.

Children's Place may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.