Church & Dwight (CHD) Gains on Portfolio Strength Amid Cost Woes

Church & Dwight Co., Inc. CHD has been benefiting from the favorable consumer demand for its brands. The company’s regular innovation, product introductions and acquisitions have helped it curate a solid portfolio. Brand strength, efficient pricing and productivity gains have been working well for Church & Dwight amid cost inflation and high SG&A expenses.

These aspects were evident in CHD’s third-quarter 2023 results, wherein the top and bottom lines beat the Zacks Consensus Estimate, and sales increased year over year. In its earnings release, management stated that it expects to witness solid operating fundamentals. Let’s delve deeper.

Buyouts & Innovation Boost Portfolio Strength

Church & Dwight, which started with only one brand, ARM & HAMMER, has acquired several top high-margin brands over the years that have been contributing to its top-line growth. The company recently completed its latest buyout of the Hero Mighty Patch brand (or Hero) and other acne treatment products. In December 2021, CHD concluded the buyout of TheraBreath, which marks the company's 14th power brand. THERABREATH mouthwash and the HERO brand delivered impressive consumption growth and grew market share in the third quarter of 2023.

Church & Dwight has been focused on product innovation to propel growth. The company has been differentiating its brands to consumers through innovative products, packaging and forms. On its third-quarter earnings call, Church & Dwight stated that it launched the ARM & HAMMER Power Sheets laundry detergent online.

The company also launched ARM & HAMMER Hardball, aimed at capturing a greater share of the lightweight litter category. Moreover, the TROJAN brand is building on the success of the Raw franchise by offering the new TROJAN Raw Non-Latex condom.

Management further highlighted that the THERABREATH brand has extended operations to the kids’ category with the launch of three new fluoride types of mouthwashes. The NAIR brand has introduced Prep & Smooth, a one-step solution that preps the face for makeup application in a No-Touch, No-Mess format. The company’s HERO brand remains focused on undertaking innovation in the acne treatment arena.

Image Source: Zacks Investment Research

Pricing Actions Aid, Online Sales Grow

Church & Dwight resorted to incremental pricing across its portfolio to counter rising costs. Favorable pricing remained an upside to the company’s organic sales in the third quarter of 2023. Organic sales increased 4.8% due to gains from volumes to the tune of 2.7%, and a favorable product mix and pricing of 2.1%. Another factor working for CHD is the online channel. The company’s global online sales continued to grow in the third quarter. Global online sales, as a percentage of total consumer sales, stood at 17%.

For 2023, organic sales growth is likely to be almost 5%. For the fourth quarter of 2023, organic sales are estimated to rise nearly 4%.

Cost Headwinds Linger

Although compensated by pricing, volumes and productivity gains, Church & Dwight’s gross margin was partly hurt by manufacturing cost inflation in the third quarter of 2023. For 2023, the company expects elevated manufacturing costs to the tune of nearly $120 million.

Church & Dwight has been witnessing increasing marketing and SG&A expenses for the past few quarters. The company has been undertaking increased marketing to fuel brand awareness, especially for new products and acquired brands. Management continues to expect increased SG&A expenses in 2023, both on a dollar basis and as a percentage of sales. The expected increase in SG&A can be attributed to additional R&D investments and elevated incentive compensation, among other factors.

Management expects marketing as a percentage of net sales to be 11% in 2023, reflecting an increase from 10% in 2022. Church & Dwight expects SG&A expenses and marketing costs to increase considerably year over year in the fourth quarter of 2023. Though the company expects gross profit expansion in the fourth quarter and full year 2023, high SG&A expenses and elevated marketing spend are likely to affect the EPS.

Wrapping Up

Strong consumer demand encouraged Church & Dwight to raise its sales guidance for 2023 during its last earnings release. The company now expects reported sales growth of nearly 9%, up from the 8% growth projected earlier. Management expects volumes to gain from marketing investments, product innovations and effective execution during the back half of the year.

The full-year adjusted operating profit is anticipated to increase nearly 8%. Management anticipates adjusted EPS of $3.15 in 2023, which implies growth of 6% from the year-ago period quarter. For the fourth quarter of 2023, Church & Dwight expects a nearly 5% increase in reported sales. Management expects adjusted EPS of 63 cents for the quarter, indicating a 2% increase from the year-ago quarter’s figure.

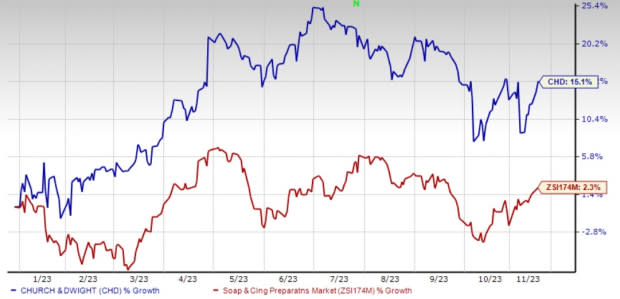

Shares of this Zacks Rank #3 (Hold) company have rallied 15.1% year to date compared with the industry’s growth of 2.3%.

3 Solid Staple Picks

Lamb Weston LW, which offers frozen potato products, currently sports a Zacks Rank #1 (Strong Buy). LW has a trailing four-quarter earnings surprise of 46.2%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Lamb Weston’s current financial-year sales and earnings suggests growth of 28% and 24.8%, respectively, from the year-ago reported numbers.

Sysco Corporation SYY, a food and related product company, currently has a Zacks Rank #2 (Buy). SYY delivered a positive earnings surprise in the last two quarters.

The Zacks Consensus Estimate for Sysco’s current fiscal-year sales and earnings suggests growth of 4.4% and 7.7%, respectively, from the corresponding year-ago reported figure.

The Kraft Heinz Company KHC, a food and beverage product company, currently carries a Zacks Rank #2. KHC has a trailing four-quarter earnings surprise of 9.9%, on average.

The Zacks Consensus Estimate for Kraft Heinz’s current fiscal-year earnings suggests growth of 6.1% from the corresponding year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Church & Dwight Co., Inc. (CHD) : Free Stock Analysis Report

Sysco Corporation (SYY) : Free Stock Analysis Report

Kraft Heinz Company (KHC) : Free Stock Analysis Report

Lamb Weston (LW) : Free Stock Analysis Report