Coca-Cola (KO) Rises on Q1 Sales & Earnings Beat, Retains View

The Coca-Cola Company KO has reported better-than-expected top and bottom-line results for first-quarter 2023. Earnings and sales also improved year over year and surpassed our estimate in the quarter. The company’s results have benefited from its continued business momentum. KO reiterated its view for 2023.

Comparable earnings of 68 cents per share grew 5% from the year-ago period and beat the Zacks Consensus Estimate of 65 cents. Meanwhile, comparable earnings surpassed our estimate of 64 cents. However, unfavorable currency translations hurt comparable earnings by 7 percentage points. Comparable currency-neutral earnings per share rose 13% year over year.

Revenues of $10,980 million surpassed the Zacks Consensus Estimate of $10,853 million and improved 5% year over year. Revenues also beat our estimate of $10,681.6 million. Organic revenues rose 12% from the prior-year quarter. Coca-Cola’s top line benefited from strong revenue growth most across its operating segments, aided by an improved price/mix and increased concentrate sales. In the reported quarter, Coca-Cola gained a global value share in total non-alcoholic ready-to-drink beverages.

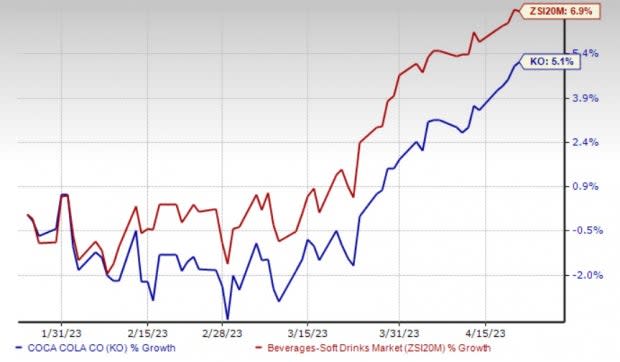

Coca-Cola’s shares jumped 1.8% in the pre-market trading session, owing to the better-than-expected first-quarter 2023 results. The Zacks Rank #2 (Buy) stock has gained 5.1% in the past three months compared with the industry’s growth of 6.9%.

Image Source: Zacks Investment Research

Volume and Pricing

In the reported quarter, concentrate sales rose 1% year over year, while the price/mix rose 11%. The price/mix benefited from pricing actions in the marketplace, coupled with a favorable channel and package mix. In the quarter, concentrate sales were 2 points lower than unit case volume due to the timing of concentrate shipments and the impacts of one less day in the quarter.

Coca-Cola’s total unit case volume rose 3% in the first quarter. The company’s ongoing investments in the marketplace and strength in the away-from-home channel aided the unit case volume. The volume for the developed markets improved in the mid-single digits in the quarter, driven by growth in Mexico, Western Europe and Australia. Meanwhile, the developing and emerging markets rose in the low-single digits. Growth in developing and emerging markets was driven by China, India and Brazil, offset by the suspension of its business in Russia.

CocaCola Company (The) Price, Consensus and EPS Surprise

CocaCola Company (The) price-consensus-eps-surprise-chart | CocaCola Company (The) Quote

Coming to the category cluster performance, volume grew 3% for sparkling soft drinks, driven by 3% growth for the trademark Coca-Cola, 8% growth for Coca-Cola Zero Sugar and a 3% gain in sparkling flavors. The sparkling soft drinks category benefited from the strong performances in Latin America and the Asia Pacific, offset by the suspension of its business in Russia.

Volume for juice, value-added dairy and plant-based beverages was even in the first quarter. Strong growth in fairlife in the United States, Minute Maid Pulpy in China and Maaza in India were largely offset by the suspension of the business in Russia.

The water, sports, coffee and tea category moved up 4% in the first quarter. Coca-Cola witnessed 5% growth in the water category, driven by gains in the Asia Pacific and Latin America. Sports drinks dipped 1% due to declines in BODYARMOR and Powerade in the United States. Tea volume was down 3% due to softness in dogadan in Turkiye. The coffee business witnessed 9% growth on strong Costa coffee performances in the U.K. and China.

Segmental Details

Revenues rose 14% for Latin America, 9% for North America and 10% for EMEA, while the same declined 3% each for the Asia Pacific and Global Ventures, and 5% for Bottling Investments.

Organic revenues improved 23% in EMEA, 19% in Latin America, 9% in North America, 3% in the Asia Pacific, 5% in Global Ventures and 11% in Bottling Investments.

Margins

In dollar terms, the operating income dipped 1% year over year to $3,367 million, including an 8-point impact of currency headwinds. Comparable operating income rose 5.6% year over year.

Comparable currency-neutral operating income advanced 15% on strong organic revenue growth across all segments, offset by higher operating costs and marketing investments.

The operating margin of 30.7% in the first quarter contracted 180 basis points (bps) from 32.5% in the prior-year quarter. The comparable operating margin expanded 40 bps to 31.8%, driven by higher operating revenues and the gains of refranchising bottling operations, offset by higher operating costs, elevated marketing investments and currency headwinds.

Guidance

Management has reiterated its view for 2023. It anticipates organic revenue growth of 7-8% for 2023. Comparable revenues are expected to be impacted by a 2-3% currency headwind based on current rates. The guidance includes a 1% negative impact of acquisition and divestiture.

The company expects an impact of a mid-single-digit percentage from commodity price inflation on comparable cost of goods sold. It anticipates an underlying effective tax rate of 19.5% for 2023.

Comparable currency-neutral earnings per share are estimated to increase 7-9%. The company anticipates year-over-year comparable earnings per share growth of 4-5%. Its comparable earnings per share growth is likely to include a headwind of 3-4% from currency and a slight headwind from acquisitions and divestitures.

For second-quarter 2023, comparable revenues are expected to include a 3-4% currency headwind and a 1% negative impact of acquisitions, divestitures and structural changes. Comparable earnings per share are estimated to include a currency headwind of 2-3%.

Management envisions an adjusted free cash flow of $9.5 billion for 2023, including $11.4 billion in cash flow from operations. Capital expenditure is likely to be $1.9 billion.

Other Stocks to Consider

We highlighted some other top-ranked stocks from the broader Consumer Staples space, namely Coca-Cola FEMSA KOF, Vita Coco Company COCO and PepsiCo PEP.

Coca-Cola FEMSA currently sports a Zacks Rank #1 (Strong Buy) and has an expected long-term earnings growth rate of 12%. KOF has a trailing four-quarter negative earnings surprise of 36.5%, on average. The company has gained 10.7% in the past three months.

You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Coca-Cola FEMSA’s current financial-year sales and earnings suggests growth of 13.4% and 7.8%, respectively, from the year-ago reported numbers. The consensus mark for KOF’s earnings per share has moved up 1.7% in the past 30 days.

Vita Coco currently flaunts a Zacks Rank #1. COCO has a trailing four-quarter earnings surprise of 21.7%, on average. The company has rallied 50.8% in the past three months.

The Zacks Consensus Estimate for Vita Coco’s current financial-year sales and earnings per share suggests growth of 10% and 178.3%, respectively, from the year-ago quarter. The consensus mark for COCO’s earnings has been unchanged in the past 30 days.

PepsiCo currently has a Zacks Rank of 2. PEP has a trailing four-quarter earnings surprise of 5%, on average. It has a long-term earnings growth rate of 7.6%. The company has improved 7.9% in the past three months.

The Zacks Consensus Estimate for PepsiCo’s current financial-year sales and earnings per share suggests growth of 3.6% and 6.5%, respectively, from the prior-year reported numbers. The consensus mark for PEP’s earnings per share has been unchanged in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CocaCola Company (The) (KO) : Free Stock Analysis Report

Vita Coco Company, Inc. (COCO) : Free Stock Analysis Report

PepsiCo, Inc. (PEP) : Free Stock Analysis Report

Coca Cola Femsa S.A.B. de C.V. (KOF) : Free Stock Analysis Report