Columbia Sportswear (COLM) Looks Troubled by High SG&A Costs

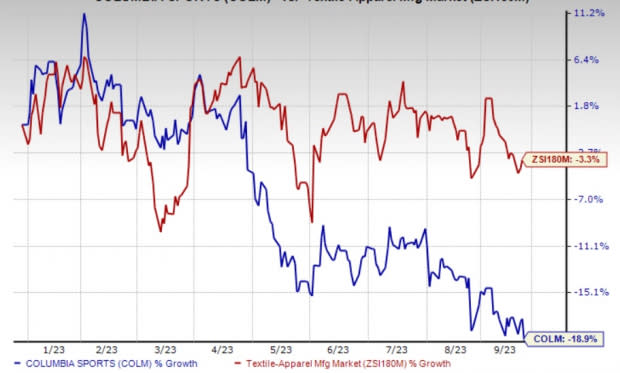

Columbia Sportswear Company COLM has been facing a challenging time, with its stock down almost 19% since the beginning of this year compared with the industry's decline of 3.3%. This Zacks Rank #5 (Strong Sell) company is grappling with several issues impacting its performance, with high SG&A costs being a major concern.

Economic factors like inflation, supply-chain disruptions and evolving consumer preferences are also adding to the company's woes. Additionally, fluctuating currency exchange rates are causing further disturbances.

We note that COLM’s second-quarter 2023 results bore testimony to these headwinds, which prompted management to revise its guidance for 2023 downward. Over the past 60 days, the Zacks Consensus Estimate for the third quarter and full-year 2023 earnings per share (EPS) has seen a significant decline, dropping from $1.97 to $1.68 and from $5.25 to $4.60, respectively.

Image Source: Zacks Investment Research

Key Concerns

One of the key factors affecting Columbia Sportswear's performance is persistently high SG&A costs. In the second quarter of 2023, the company’s SG&A expenses escalated by 11% to $312.5 million. As a percentage of sales, the same expanded from 48.7% to 50.3%.

The year-over-year rise in SG&A expenses can be attributed to elevated costs related to the supply chain, direct-to-consumer (DTC) and technology. As a percentage of net sales, SG&A expenses are anticipated in the range of 40.1-40.5% now compared with the 39-39.2% expected earlier.

For 2023, the operating income is expected in the band of $348-$368 million, with the operating margin expected at 9.8-10.3%. Earlier, the operating income was expected in the range of $413-$432 million, with the operating margin expected at 11.6-11.8%. In 2022, the company reported an operating margin of 11.3%.

In the third quarter of 2023, the operating income is likely to come in the range of $132-$138 million, with the operating margin expected at 13.2-13.6%. This suggests a decline from the operating margin of 15.2% reported in the third quarter of 2022.

Columbia Sportswear's exposure to international markets also makes it susceptible to currency fluctuations. The weakening of foreign currencies against the U.S. dollar may force the company to either raise prices or accept lower profit margins in locations outside the United States. Therefore, adverse currency movements continue to pose a threat to the company's profitability.

Management expects foreign currency translation to hurt net sales growth by roughly 30 bps in 2023. It expects foreign currency translation to hurt earnings by 3 cents in 2023.

2023 View Looks Dull

Columbia Sportswear's performance in the second quarter of 2023 was marked by a dynamic landscape. While some international markets, such as China, showed promise, the company faced increased challenges in the United States. Given the results so far this year and ongoing business trends, management remains cautious about the remainder of the year, per its last earnings release.

COLM's guidance for the full-year 2023 takes into account various economic factors, including inflation, supply-chain disruptions, geopolitical tensions, shifting consumer behavior and increased inventory levels in the marketplace. Columbia Sportswear now anticipates net sales to grow by 2-3.5%, reaching the range of $3.53-$3.59 billion. This is a revision from the previous expectation of 3-6% growth to the $3.57-$3.67 billion band.

EPS projections for 2023 have also been adjusted to the range of $4.40-$4.65, down from the earlier range of $5.15-$5.40. The third-quarter EPS is expected to fall in the range of $1.60-$1.70 compared with $1.80 reported in the same period last year.

Though Columbia Sportswear is benefiting from its focus on strategic priorities and strength in the DTC business, challenges posed by high SG&A costs and uncertainties in the current economic landscape cannot be overlooked in the short term.

Take a Look at These Solid Picks

Three better-ranked stocks include Guess?, Inc. GES, G-III Apparel Group, Ltd. GIII and American Eagle Outfitters, Inc. AEO.

Guess?, which designs, markets, distributes and licenses lifestyle collections of apparel and accessories, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for GES’ current financial-year revenues and EPS suggests growth of 3.7% and 9.9%, respectively, from the year-ago reported figure. Guess? has a trailing four-quarter earnings surprise of 43.4%, on average.

G-III Apparel, which designs, sources and markets women's and men's apparel, sports a Zacks Rank #1.

The Zacks Consensus Estimate for G-III Apparel’s current financial-year sales and earnings suggests growth of 8% and 14.7%, respectively, from the year-ago period. GIII has a trailing four-quarter earnings surprise of 526.6%, on average.

American Eagle, a specialty retailer, currently sports a Zacks Rank #1. AEO has a trailing four-quarter earnings surprise of 43.2%, on average.

The Zacks Consensus Estimate for American Eagle’s current financial-year sales and earnings suggests growth of 1.5% and 29.9%, respectively, from the year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

Columbia Sportswear Company (COLM) : Free Stock Analysis Report

Guess?, Inc. (GES) : Free Stock Analysis Report

G-III Apparel Group, LTD. (GIII) : Free Stock Analysis Report