A Competitive Solar Market Analysis for NextEra Energy

From my research, by 2050, solar energy should be the largest provider of electricity on the planet. I believe there is a significant long-term value and growth opportunity in investing in the market at this time. NextEra Energy offers exposure to a diversified clean energy portfolio. While I think it is an attractive long-term investment, I believe there are better allocations to companies more concentrated on solar, which I will specify, that offer the highest future returns.

Company overview

NextEra Energy Inc. (NYSE:NEE) is a prominent player in the clean energy sector, and it is the parent company of Florida Power & Light Company, which is the largest electric utility in the United States based on retail electricity produced and sold. FPL serves around 5.8 million customer accounts, catering to 12 million people across Florida.

The company is also one of America's largest capital investors in infrastructure, with a presence in 49 U.S. states. It also operates NextEra Energy Resources, which is recognized as having the world's most extensive clean energy portfolio, with a generation capacity of 24,000 megawatts from renewable sources, predominantly solar and wind, which is more than any other company globally.

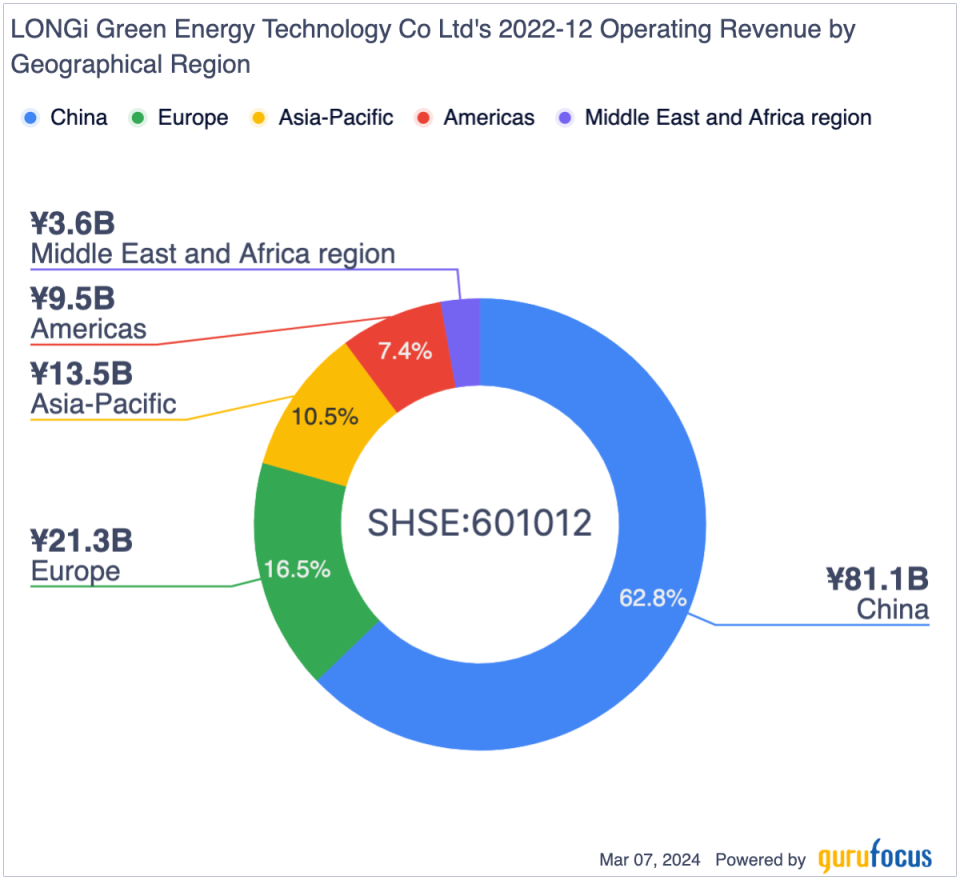

All of its operating revenue comes from the U.S., of which 82.5% comes from Florida Power & Light Company, 17.8% from NextEra Energy Resources and -0.2% from other corporate expenses.

Long-term market outlook

From my research and confirmed by my investment recently in Enphase Energy (NASDAQ:ENPH), I believe solar energy is going to be the dominant form of power provision in the world by 2050. The Department of Energy's Solar Futures Study outlines that for a goal of 100% decarbonization of the U.S. grid by 2050, solar deployments could be 1,050 gigawatts to 1,570 gigawatts, meaning 44% to 45% of electricity demand. The study outlines a potential for net savings of $1.7 trillion due to this initiative.

In addition, the International Energy Agency highlights how globally, policy support and technological innovation are accelerating solar capacity growth. Countries including China, the European Union, the U.S., India and Brazil have ambitious decarbonization targets and policies, which are strengthened by advancements in solar photovoltaic technology and manufacturing capacity. The IEA's Net Zero by 2050 plan forecasts a 20-fold increase in solar capacity by 2050.

Competition and financial analysis

As mentioned, I recently invested in Enphase Energy, but this is not the only allocation to solar energy I plan to make. I think that China's LONGi Green Energy Technology Co. (SHSE:601012) is the greatest long-term investment in solar at this time. Its price is down 71% at the time of writing, indicating what I believe to be a rare opportunity. I have provided a breakdown of the key elements of comparison here:

LONGi Green Energy: Price down 71%, price-earnings ratio of 10.25, equity-to-asset ratio of 0.44, debt-to-equity ratio of 0.21, net margin of 11.40% and three-year revenue growth rate of 53.70%.

Enphase Energy: Price down 62%, price-earnings ratio of 41, equity-to-asset ratio of 0.29, debt-to-equity ratio of 1.32, net margin 19.16% and three-year revenue growth rate of 43.10%.

NextEra Energy: Price down 40%, price-earninngs ratio of 15.40, equity-to-asset ratio of 0.27, debt-to-equity ratio of 1.54, net margin of 26% and three-year revenue growth rate of 14.80%.

LONGi evidently has an advantage, particularly in its balance sheet above both of the other companies, but also in regard to its revenue growth rate. Where it falls short is the net margin. Notably, LONGi is the only company of the three to have geographically diversified operating revenue. Both Enphase and NextEra have all revenue generated in the U.S.

LONGi is widely recognized as the world's leading solar technology company. It is planning to build the world's largest solar factory for $6.70 billion; positioned in China, it will be capable of manufacturing 100 gigawatts of solar wafers and 50 gigawatts of solar cells each year.

NextEra provides some competitive advantage over LONGi through its broader operational scope, including exposure to wind generation, energy storage and the operation of an extensive grid network. However, this operational diversification does not necessarily make for the best investment case in terms of long-term growth. In fact, I believe its portfolio diluted away from solar indicates lower growth than a pure-play solar investment provided by Enphase and LONGi.

Value analysis

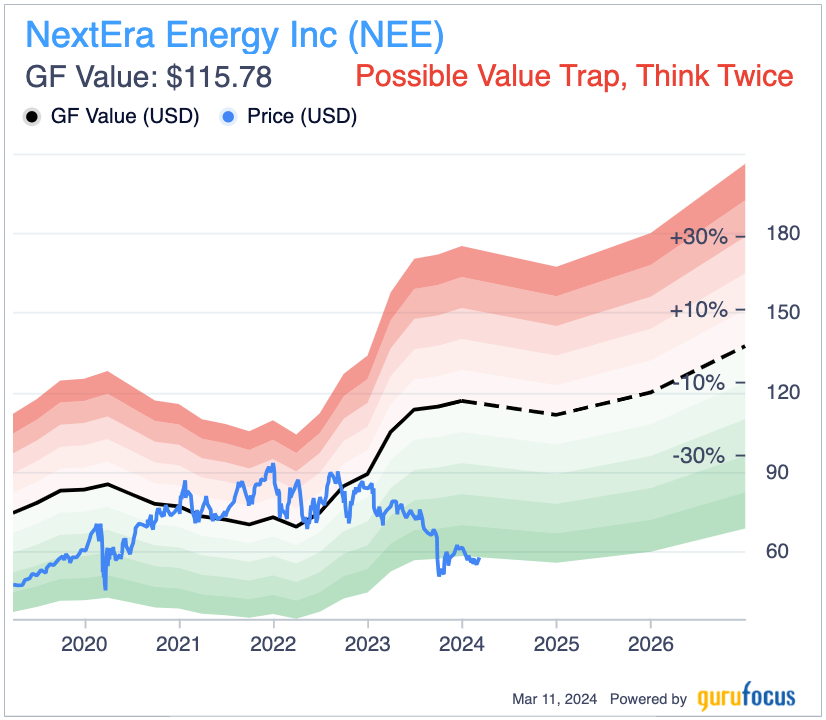

At this time, all three stocks look significantly undervalued to me, but I will focus on NextEra for the purpose of this analysis. The GF Value chart suggests the stock could be a possible value trap, but, if not, it indicates a significant undervaluation. We can also see from the chart that consensus analyst estimates predict an earnings per share contraction until fiscal 2025, when growth is set to resume. Therefore, I consider now to be an excellent time to invest as I believe the market will begin to price the investment higher once it starts showing year-over-year earnings growth.

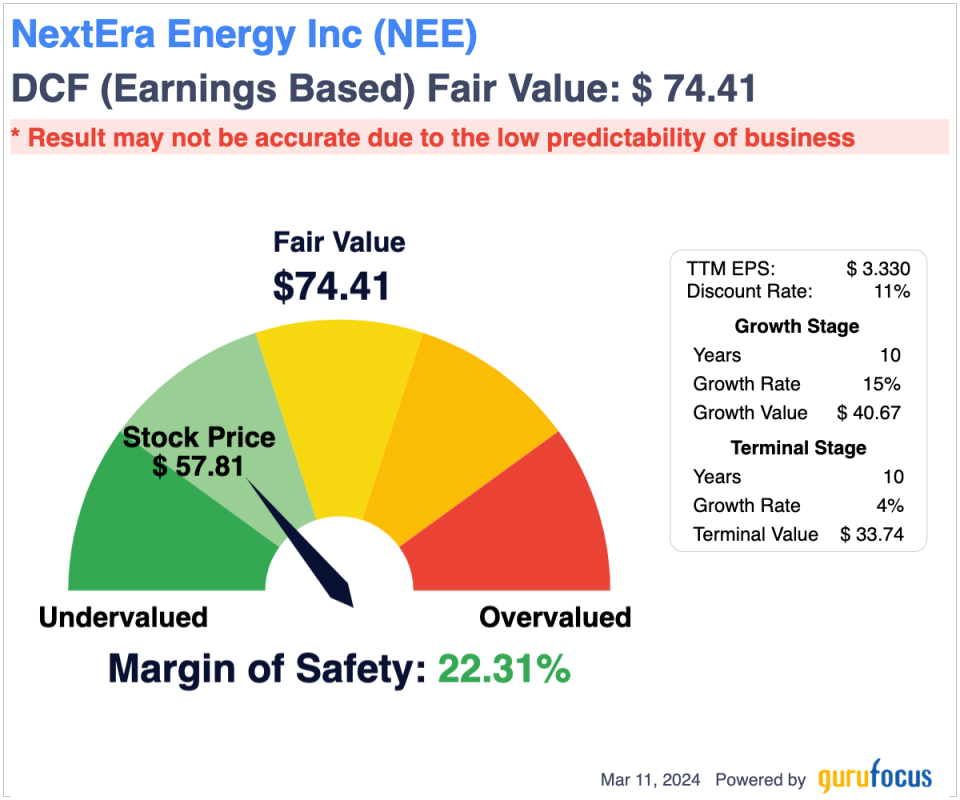

As the market is not placing a premium on solar companies at this time, as is the case with other elite technology companies, I believe a discounted cash flow analysis is the most prudent method of assessing fair value for NextEra. I believe the company has a significant growth horizon beyond the next 10 years; however, for the purpose of this analysis and for the sake of conservatism and risk mitigation, I have kept an inflation level 4% terminal-stage earnings per share annual growth rate for 10 years following my growth stage. From my research, I believe a market compound annual growth rate for solar capacity in the U.S. over the next 10 years could be roughly 20%, which estimates by the World Economic Forum confirm. However, NextEra's exposure to this is reduced due to its more diversified operations, including wind. As such, I have used a 15% earnings per share annual growth rate as a conservative estimate for the growth stage of my discounted cash flow analysis. I have also used a typical 11% discount rate. The results indicate a 22.30% margin of safety based on a share price of $57.80 and my fair value estimate of $74.40.

Short-term downside risk

I believe the most significant risk with investing in any of the three clean energy companies I have outlined is short-term downward momentum as a result of wider economic stagnation and higher interest rates, particularly in the U.S., but also slow economic growth in Asia and wider internationally, as it relates to LONGi. Therefore, I believe investors should consider the need to weather considerable short-term losses before the clean energy markets resume more typical growth. This may be a challenging period, and while it is impossible to invest right at the bottom, I believe we are as close as we can rationally get without speculating, which affirms my buy rating for LONGi and Enphase.

Conclusion

NextEra is an exceptional investment in solar energy, but it is not the best. At this time, the first priority on my list goes to LONGi and second to Enphase. NextEra may have a place in portfolios looking for diversified energy exposure, particularly to wind, but I believe investors will find significantly better returns from allocating to LONGi and Enphase over the long term. I believe now is one of the best times to allocate heavily to solar energy with a long-term holding period considering outsized market growth to come leading up to 2050.

This article first appeared on GuruFocus.