Container shipping stocks outperform despite market gloom

Shipping stocks have a habit of defying expectations. At the beginning of 2023, sentiment was ebullient on crude tanker and product tanker shares. The word “supercycle” was bandied about. Global fuel demand was bouncing back from COVID, sanctions on Russia were inflating voyage distances, and the ratio of tanker tonnage on order to tonnage on the water was historically low.

Dry bulk shares were also expected to rise. As with tankers, the dry bulk orderbook was exceptionally slim. China would rebound quickly from COVID, the theory went, ramping up dry bulk demand as the year progressed.

On the negative side, a large number of liquefied petroleum gas (LPG) carriers — specialized tankers that carry propane — were poised for delivery in 2023, darkening sentiment on LPG shipping stocks as the year began.

Sentiment on container shipping stocks was even worse. Freight rates and ship leasing rates were plunging. A predicted recession was set to curb future demand. The orderbook-to-fleet ratio was an ominous 30% and a tidal wave of newbuildings would hit the market starting in March.

So, over halfway through 2023, what actually happened to shipping stocks?

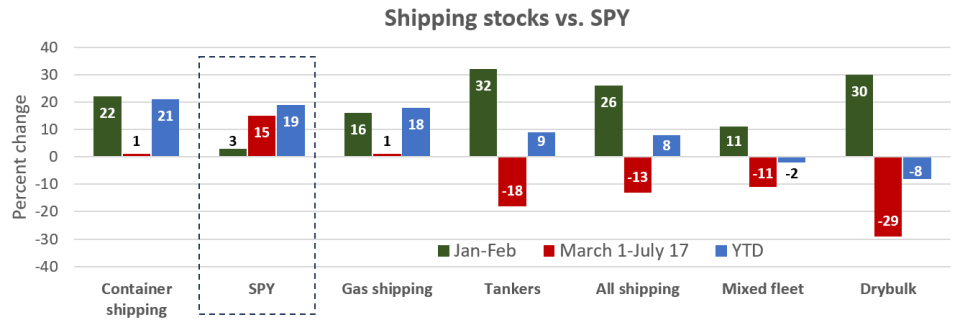

Container shipping has been the best-performing U.S.-listed sector year to date, on average. Gas shipping has been the second best. Tanker stocks are trailing behind containers and gas shipping, while dry bulk shares have performed the worst on average.

This is not what was expected at the beginning of the year.

Shipping stocks by sector vs. SPY

FreightWaves analyzed adjusted closing prices (adjusted to account for dividends) from Dec. 30, 2022, through Monday of 22 U.S.-listed stocks of shipowners with market capitalizations of at least $400 million. Companies with offshore interests were excluded, as were larger owners that listed after Jan. 1.

Performance of the main shipping sectors (using a non-market-cap-weighted average of surveyed shipping shares in those sectors) was compared to the SPDR S&P 500 ETF Trust (NYSE: SPY), one of the most popular vehicles to invest in the broader equity market.

March marked a major turning point for shipping stocks. In January and February, shipping stocks outperformed the broader market. Since March, shipping stocks on average have underperformed the market, albeit with different trends for different segments.

To examine the effect of the March turning point, shipping stocks were compared to SPY year to date (YTD) as well as in January-February and March onwards. SPY’s percentage changes in these three time periods were virtually identical to changes in the average of the three main indexes — the S&P 500, Dow Jones Industrial Average and Nasdaq Composite — making SPY a good proxy for the broader market.

Shares of the 22 shipping stocks included in the analysis are up an average of 8% YTD, less than half the 19% YTD gain of SPY.

Container shipping stocks are up an average of 21%, edging out broader stock market gains. Gas shipping stocks are up an average of 18% YTD and tankers 9%. Mixed-fleet owners are down 2% and dry bulk owners are down 8% YTD.

Tankers and dry bulk stocks rose the most in January and February, 32% and 30%, respectively. But they also fell the most between March 1 and Monday, 18% and 29%, respectively, in a period when SPY rose 15%. Larger-cap container shipping and gas shipping stocks, on average, did not fall like tanker and dry bulk stocks did over the past four and a half months.

Container shipping stocks

The container shipping stocks have done surprisingly well given the gloom in the container business due to overcapacity and excess goods inventories.

The adjusted closing price of container-ship lessor Danaos (NYSE: DAC) is up 29% YTD, as is the price of Hawaii-based niche ocean carrier Matson (NYSE: MATX). Container-ship lessor Global Ship Lease (NYSE: GSL) is up 24%. The outlier — and worst performer among U.S.-listed container shipping stocks — is Israel-based ocean carrier Zim (NYSE: ZIM). Its adjusted stock price (accounting for a large dividend payout) has suffered a 27% pullback since March. Zim shares are significantly underperforming the broader market YTD.

Liquefied gas shipping stocks

Listed gas shipowners include LPG carrier owners and liquefied natural gas carriers owners. The two U.S.-listed LPG carrier owners with market caps over $400 million are Dorian LPG (NYSE: LPG) and Navigator Holdings (NYSE: NVGS). Their adjusted closing prices are up 43% and 12% YTD, respectively.

Dorian, which owns very large gas carriers (VLGCs), is the best-performing U.S.-listed shipping stock YTD. Despite a large influx of VLGC newbuildings, high demand has pushed up VLGC spot rates to nearly triple the trailing five-year average, according to data from Clarksons.

In the LNG shipping market, most of the previously listed owners have gone private. The adjusted share price of Flex LNG (NYSE: FLNG) is flat YTD, with January-February gains counterbalanced by declines since then. (Another large pure LNG carrier owner, Coolco, was not included in the survey because it listed on NYSE in March.)

Tanker shipping stocks

Tanker shipping stocks have been an extremely mixed bag. Stock performance has hinged on the type of tankers that are owned. Shares of owners of mid-sized tankers are still doing very well. Stocks of several owners of very large crude carriers (VLCCs) have given back earlier gains, but are still even to slightly up on the year. Shares of product tanker owners are down.

The big three gainers YTD are Frontline (NYSE: FRO), Nordic American Tankers (NYSE: NAT) and Teekay Tankers (NYSE: TNK), up 39%, 32% and 29%, respectively — handily outperforming SPY despite pullbacks in recent months.

VLCC owners International Seaways (NYSE: INSW), DHT (NYSE: DHT) and Euronav (NYSE: EURN) have underperformed the broader market through mid-July.

The overall tanker sector average has been pulled down by product tanker owners Torm (NASDAQ: TRMD), Ardmore Shipping (NYSE: ASC) and Scorpio Tankers (NYSE: STNG), whose shares have fallen significantly over recent months.

Scorpio is the worst performer among the larger U.S.-listed shipping names. Its adjusted close on Monday was down 20% YTD.

Mixed-fleet stocks

Among the larger mixed-fleet players, Costamare (NYSE: CMRE) owns container ships and bulkers, and Navios Partners (NYSE: NMM) owns container ships, tankers and bulkers. (Ship Finance International was not covered by the survey due to its offshore interests.)

Mixed-fleet shares followed the general shipping trend: rising in January and February and pulling back since then. Costamare is up 9% YTD. Navios Partners is down 12%.

Dry bulk stocks

Dry bulk offers a particularly clear example of shipping’s March turning point, likely due to dry bulk’s high exposure to the Chinese economy. China’s post-COVID Chinese recovery has been much weaker than expected. Current dry bulk spot rates are down double digits from their five-year trailing average, according to Clarksons data.

The four U.S.-listed pure dry bulk owners with market caps over $400 million all followed the same pattern. Shares rose by double digits in the first two months of the year, then gave back those gains and more. All are underperforming SPY, although not by as much as the product-tanker subsector.

The adjusted close of Star Bulk (NYSE: SBLK) was down 4% YTD through Monday, with Genco (NYSE: GNK) down 8%, Eagle Bulk (NYSE: EGLE) down 9% and Golden Ocean (NASDAQ: GOGL) down 11%.

Click for more articles by Greg Miller

Related articles:

Controversy swirls over shipping stocks that sink as rates rise

Shipping stock sell-off: Shares down double digits since March

As oil tumbles, marine fuel gets cheaper — and so do tanker stocks

Shipping faces fallout as China’s post-COVID rebound falls flat

Tanker shipping stocks sink despite talk of looming rate boom

New way to place your bets on boom and bust of shipping cycle

The post Container shipping stocks outperform despite market gloom appeared first on FreightWaves.