Continued Debt Reduction And Structural Reforms Crucial For Greece’s Sovereign-rating Trajectory

Support for Greece from European institutions, improving economic fundamentals and a strengthened banking system drove Scope Ratings’ decision to upgrade Greece’s credit rating to BBB- in August of last year, helping the sovereign regain an investment-grade standing after more than a decade as a sub-investment-grade credit.

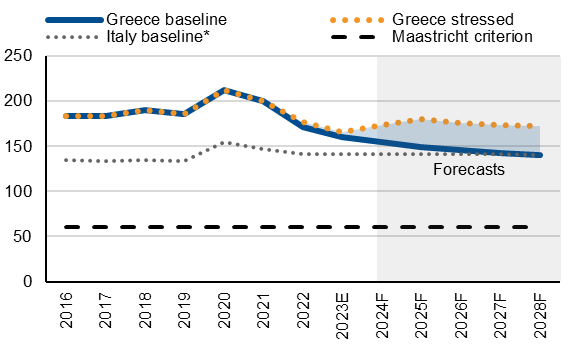

For further improvement of Greece’s credit standing, solid nominal economic growth and continued fiscal consolidation are necessary for ensuring a significant reduction of government debt-to-GDP, even though it has already fallen to below pre-Covid levels – estimated at 160.3% of GDP at end-2023 – and is seen converging on that of Italy (Figure 1). Nevertheless, the debt ratio remains the highest of the euro area. The government needs to foster reforms and maintain prudent management of public finances to ensure further steady debt reduction.

Figure 1. Greece’s general government debt ratio, % of GDP

Sovereign Credit Quality Linked to Bolstering Banking System Given High NPLs

Further progress in strengthening the Greek banking system is also essential. Greek banks’ financial fundamentals have significantly improved over the past years and profitability has recently rebounded. Greek banks reported a return-on-equity of 12.9% over the first nine months of 2023. We see this trajectory continuing, helped by higher interest margins and declining loan-loss provisioning.

Banks have also advanced in cleaning up their balance sheets, although they still significantly lag EU averages when it comes to non-performing loan (NPL) ratios. System-wide NPLs dropped to 7.9% as of September 2023 from the above 49% in mid-2017. The government supported asset securitisations by adopting a scheme providing public guarantees on senior notes. Recently, the government announced plans for extending the Hercules scheme until at least the end of 2024.

We expect banks to continue proactively managing their asset quality to further close the gap to the remainder of the EU. At the same time, NPLs might again rise in the future because of the effect of higher rates on borrowers’ debt-servicing capacities.

Elevated shares of deferred tax credits in banking-system aggregate capital continue to be a problem. Deferred tax credits declined only marginally to 51% of total prudential banks’ own funds in June 2023, from 52% as of end-2022. However, growing operating profits will help banks to accumulate reserves and enhance their asset quality.

Improving Greece’s Modest Growth Potential Critical for Medium-run Economic Outlook

The government needs to oversee further structural improvements in the economy, such as curtailing external-sector risks, assuring higher rates of medium-run economic growth and strengthening macroeconomic sustainability. Greece has a sizeable current-account deficit and a net international investment position deeply in net-debtor position.

The economy’s medium-run growth potential remains tepid around 1% despite continued progress on reforms through the “Greece 2.0” and Greek Recovery and Resilience plans. Constraints include adverse demographics, as well as weak and uneven productivity growth across the regions because of years of public- and private-sector under-investment and a lack of business-sector dynamism.

Political Stability And Policy Continuity Crucial To Sustaining Investor Confidence

The recent out-performance of the Greek economy gives us confidence that robust economic growth is not transitory, but there are nevertheless several challenges for the outlook. Persistent uncertainty over the inflation outlook raises questions of whether inflation will continue to decline towards the ECB 2% objective. Core inflation sits well above 2% despite recent significant disinflation.

We see inflation remaining above the ECB objective for much of this year. Furthermore, we cannot exclude new supply-side crises in view of a turbulent international political and economic context, which might again send inflation higher later and further postpone the fuller normalisation of monetary policies.

Environmental challenges are also relevant. Among the EU, Greece is most exposed to rising temperatures and more frequent heatwaves and wildfires, which can damage the crucial tourism and agriculture sectors.

Finally, new political challenges could emerge following general elections due by 2027 if the government shifts away from current business-friendly policies. Maintaining a constructive dialogue with European institutions and the capital markets is relevant, as is avoiding the temptation of further reversing the difficult reforms introduced during the debt crisis.

Regaining investment-grade status has contributed to the narrowing of yield spreads on 10-year Greek government bonds – to under 100bp to Germany recently – reflecting significantly better investor confidence.

Further progress on reforms to strengthen the structure of the economy and enhance macroeconomic sustainability would contribute to improving Greece’s appeal for foreign and domestic investors. Moreover, the presumed peak in the ECB rate-hike cycle ought to facilitate investment.

For a look at all of today’s economic events, check out our economic calendar.

Dennis Shen is Senior Director in Sovereign and Public Sector ratings at Scope Ratings GmbH, and lead analyst on Greece. Alessandra Poli, Analyst at Scope, and Matthew Curtin, Deputy Head of Communications of Scope, contributed to writing this article.

This article was originally posted on FX Empire