Cortus Energy (STO:CE) Has Debt But No Earnings; Should You Worry?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that Cortus Energy AB (publ) (STO:CE) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Cortus Energy

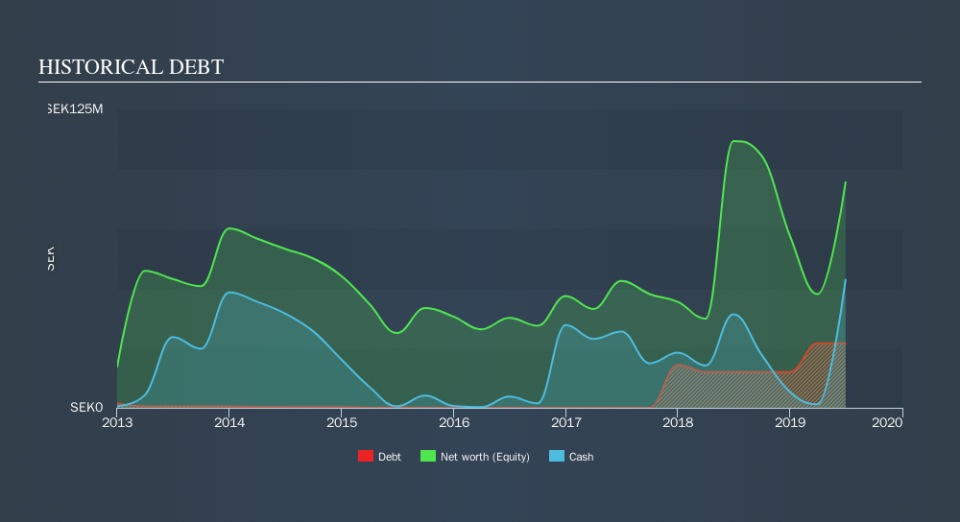

What Is Cortus Energy's Debt?

As you can see below, at the end of June 2019, Cortus Energy had kr27.0m of debt, up from kr15.0m a year ago. Click the image for more detail. But it also has kr53.7m in cash to offset that, meaning it has kr26.7m net cash.

How Strong Is Cortus Energy's Balance Sheet?

According to the last reported balance sheet, Cortus Energy had liabilities of kr23.1m due within 12 months, and liabilities of kr27.0m due beyond 12 months. Offsetting these obligations, it had cash of kr53.7m as well as receivables valued at kr1.03m due within 12 months. So it can boast kr4.55m more liquid assets than total liabilities.

Having regard to Cortus Energy's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the kr538.7m company is struggling for cash, we still think it's worth monitoring its balance sheet. Succinctly put, Cortus Energy boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is Cortus Energy's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Cortus Energy actually shrunk its revenue by 33%, to kr3.7m. That makes us nervous, to say the least.

So How Risky Is Cortus Energy?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Cortus Energy had negative earnings before interest and tax (EBIT), over the last year. Indeed, in that time it burnt through kr129m of cash and made a loss of kr133m. Given it only has net cash of kr54m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Cortus Energy insider transactions.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.