Costco (COST) Lined Up for Q4 Earnings: What's in the Offing?

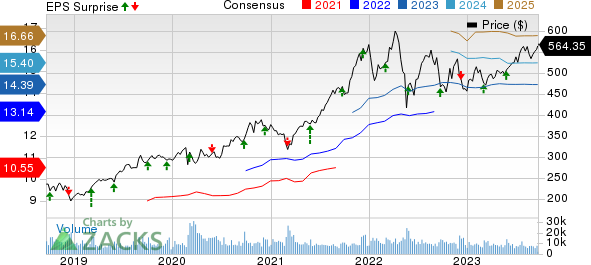

Costco Wholesale Corporation COST is likely to register an increase in the top line when it reports fourth-quarter fiscal 2023 results on Sep 26 after the closing bell. The Zacks Consensus Estimate for revenues is pegged at $78.56 billion, indicating growth of 9% from the prior-year reported figure.

The bottom line of this Issaquah, WA-based company is anticipated to have improved year over year. Although the Zacks Consensus Estimate for fourth-quarter earnings per share has declined by a penny to $4.71 over the past 30 days, the figure still suggests an increase of 12.1% from the year-ago period.

Costco has a trailing four-quarter earnings surprise of 1.8%, on average. In the last reported quarter, the company’s bottom line outperformed the Zacks Consensus Estimate by 3.3%.

Key Factors to Note

Costco’s growth strategies, better price management and decent membership trends have been contributing to its performance. The company’s strategy to sell products at discounted prices has helped attract customers who have been seeking both value and convenience. These factors, complemented by reduced supply-chain costs and an increasing penetration of private-label brands, are expected to have a positive impact on the overall results.

For the quarter in focus, we anticipate an impressive 7.9% jump in net sales and a notable 6.1% increase in total membership fees. Costco's paid membership base has been on a steady ascent, driven by a growing customer base and remarkable renewal rates. We also project 0.7% growth in comparable sales for the fourth quarter.

However, it is essential to acknowledge the presence of certain headwinds, including inflationary pressures and a high-interest-rate environment, which may pose challenges. Additionally, margins remain a critical area to monitor, with potential concerns stemming from any deleverage in the SG&A rate, higher labor and occupancy costs, and increased marketing and other store-related expenses. We expect SG&A expenses, as a percentage of total revenues, to deleverage 50 basis points to 8.9%.

Costco Wholesale Corporation Price, Consensus and EPS Surprise

Costco Wholesale Corporation price-consensus-eps-surprise-chart | Costco Wholesale Corporation Quote

What the Zacks Model Unveils

Our proven model does not conclusively predict an earnings beat for Costco this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. However, that’s not the case here.

Costco has a Zacks Rank #3 but an Earnings ESP of -1.79%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

3 Stocks With the Favorable Combination

Here are three companies you may want to consider as our model shows that these have the right combination of elements to post an earnings beat:

Ross Stores ROST currently has an Earnings ESP of +1.00% and a Zacks Rank #2. The company is likely to register a bottom-line increase when it reports third-quarter fiscal 2023 numbers. The Zacks Consensus Estimate for the quarterly earnings per share of $1.21 suggests an increase of 21% from the year-ago quarter. You can see the complete list of today’s Zacks #1 Rank stocks here.

Ross Stores’ top line is expected to ascend year over year. The Zacks Consensus Estimate for quarterly revenues is pegged at $4.82 billion, which indicates an increase of 5.6% from the figure reported in the prior-year quarter. Ross Stores has a trailing four-quarter earnings surprise of 11.4%, on average.

Casey's General Stores CASY currently has an Earnings ESP of +1.21% and carries a Zacks Rank #3. The company is likely to register a bottom-line decrease when it reports second-quarter fiscal 2024 numbers. The Zacks Consensus Estimate for quarterly earnings per share of $3.49 suggests a drop of 4.9% from the year-ago quarter.

Casey's General Stores’ top line is expected to increase year over year. The Zacks Consensus Estimate for quarterly revenues is pegged at $4.07 billion, which indicates a rise of 2.4% from the figure reported in the prior-year quarter. CASY has a trailing four-quarter earnings surprise of 17.5%, on average.

Nordstrom JWN currently has an Earnings ESP of +5.58% and a Zacks Rank of #3. The company is likely to register a decline in the bottom line when it reports third-quarter fiscal 2023 results. The Zacks Consensus Estimate for the quarterly earnings per share of 14 cents suggests a drop of 30% from the year-ago quarter.

Nordstrom’s top line is expected to decrease year over year. The Zacks Consensus Estimate for quarterly revenues is pegged at $3.41 billion, which suggests a decline of 3.9% from the figure reported in the prior-year quarter. JWN has a trailing four-quarter earnings surprise of 75.4%, on average.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Nordstrom, Inc. (JWN) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Casey's General Stores, Inc. (CASY) : Free Stock Analysis Report