Couchbase (NASDAQ:BASE) Beats Expectations in Strong Q4, Stock Jumps 16%

Database as a service company Couchbase (NASDAQ: BASE) reported Q4 FY2024 results beating Wall Street analysts' expectations , with revenue up 20.3% year on year to $50.09 million. On top of that, next quarter's revenue guidance ($48.5 million at the midpoint) was surprisingly good and 3.3% above what analysts were expecting. It made a non-GAAP loss of $0.06 per share, improving from its loss of $0.18 per share in the same quarter last year.

Is now the time to buy Couchbase? Find out by accessing our full research report, it's free.

Couchbase (BASE) Q4 FY2024 Highlights:

Revenue: $50.09 million vs analyst estimates of $46.55 million (7.6% beat)

EPS (non-GAAP): -$0.06 vs analyst estimates of -$0.14

Revenue Guidance for Q1 2025 is $48.5 million at the midpoint, above analyst estimates of $46.94 million

Management's revenue guidance for the upcoming financial year 2025 is $205 million at the midpoint, in line with analyst expectations and implying 13.9% growth (vs 16.3% in FY2024)

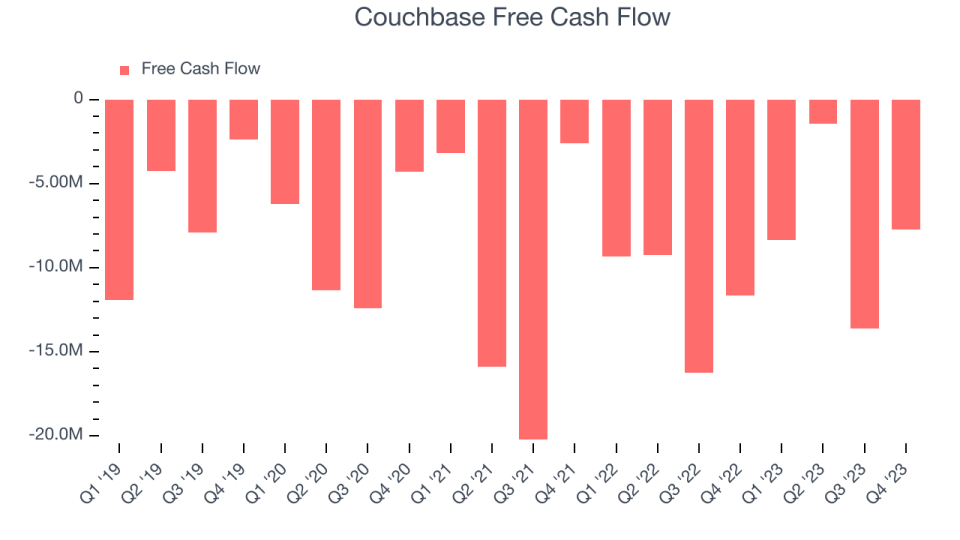

Free Cash Flow was -$7.74 million compared to -$13.61 million in the previous quarter

Gross Margin (GAAP): 89.7%, up from 85.7% in the same quarter last year

Market Capitalization: $1.34 billion

"We finished fiscal 2024 on a strong note, highlighted by 25% ARR growth, and marking a historical year for Couchbase," said Matt Cain, Chair, President and CEO of Couchbase.

Formed in 2011 with the merger of Membase and CouchOne, Couchbase (NASDAQ:BASE) is a database-as-a-service platform that allows enterprises to store large volumes of semi-structured data.

Data Storage

Data is the lifeblood of the internet and software in general, and the amount of data created is accelerating. As a result, the importance of storing the data in scalable and efficient formats continues to rise, especially as its diversity and associated use cases expand from analyzing simple, structured datasets to high-scale processing of unstructured data such as images, audio, and video.

Sales Growth

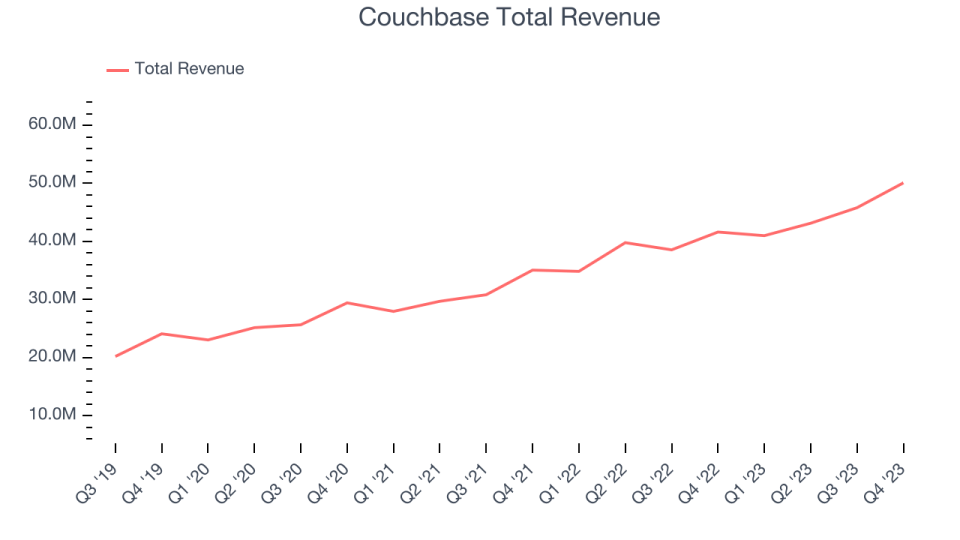

As you can see below, Couchbase's revenue growth has been strong over the last two years, growing from $35.06 million in Q4 FY2022 to $50.09 million this quarter.

This quarter, Couchbase's quarterly revenue was once again up a very solid 20.3% year on year. On top of that, its revenue increased $4.28 million quarter on quarter, a very strong improvement from the $2.67 million increase in Q3 2024. This is a sign of re-acceleration of growth and great to see.

Next quarter's guidance suggests that Couchbase is expecting revenue to grow 18.3% year on year to $48.5 million, in line with the 17.6% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $205 million at the midpoint, growing 13.9% year on year compared to the 16.3% increase in FY2024.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. Couchbase burned through $7.74 million of cash in Q4 , increasing its cash burn by 33.7% year on year.

Couchbase has burned through $31.15 million of cash over the last 12 months, resulting in a negative 17.3% free cash flow margin. This low FCF margin stems from Couchbase's constant need to reinvest in its business to stay competitive.

Key Takeaways from Couchbase's Q4 Results

We were impressed by how strongly Couchbase blew past analysts' total revenue, ARR (annual recurring revenue), and EPS estimates this quarter as it generated more subscription revenue than expected. We were also glad next quarter's revenue guidance was higher than Wall Street's estimates, though its full-year outlook was in line. Overall, we think this was a really good quarter that should please shareholders, especially with the broader software sector showing choppy full-year 2024 guidance. The stock is up 16% after reporting and currently trades at $31.19 per share.

Couchbase may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.