Cushman & Wakefield (NYSE:CWK) Exceeds Q4 Expectations

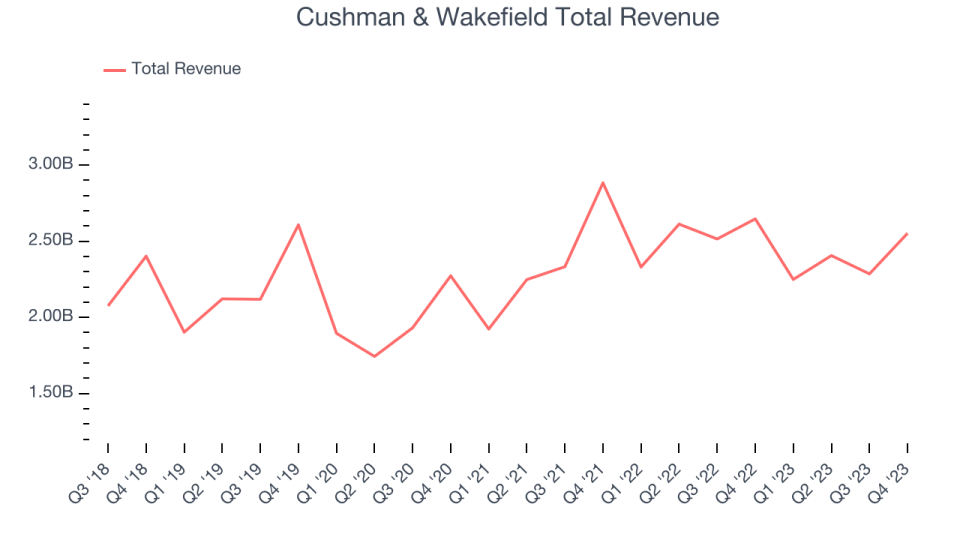

Real estate services firm Cushman & Wakefield (NYSE:CWK) announced better-than-expected results in Q4 FY2023, with revenue down 3.6% year on year to $2.55 billion. It made a non-GAAP profit of $0.45 per share, improving from its profit of $0.13 per share in the same quarter last year.

Is now the time to buy Cushman & Wakefield? Find out by accessing our full research report, it's free.

Cushman & Wakefield (CWK) Q4 FY2023 Highlights:

Revenue: $2.55 billion vs analyst estimates of $2.43 billion (4.9% beat)

EPS (non-GAAP): $0.45 vs analyst estimates of $0.40 (13.1% beat)

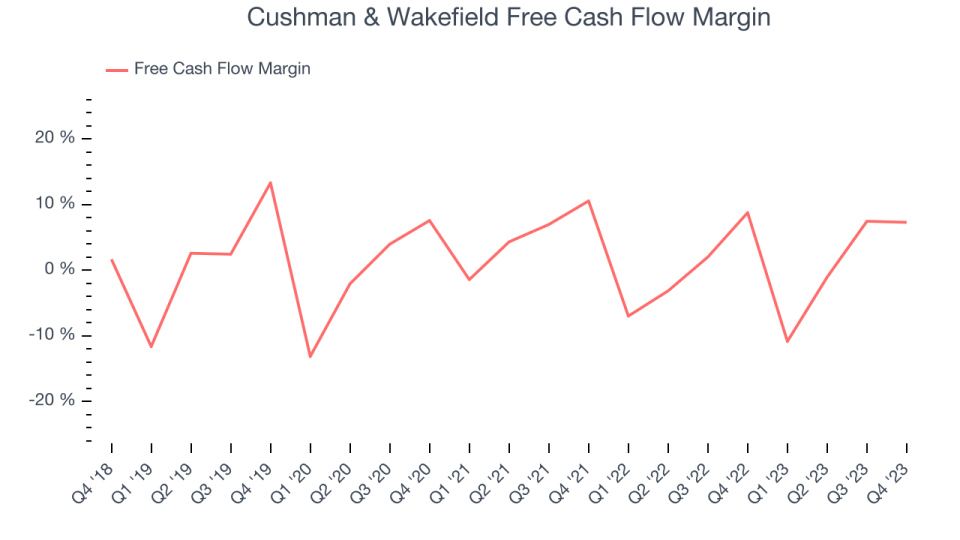

Free Cash Flow of $186.2 million, similar to the previous quarter

Gross Margin (GAAP): 18.8%, up from 18.3% in the same quarter last year

Market Capitalization: $2.62 billion

“Our Cushman & Wakefield team accomplished a great deal in 2023,” said Michelle MacKay, Cushman & Wakefield Chief Executive Officer.

With expertise in the commercial real estate sector, Cushman & Wakefield (NYSE:CWK) is a global Chicago-based real estate firm offering a comprehensive range of services to clients.

Real Estate Services

Technology has therefore been a double-edged sword in real estate services. On the one hand, internet listings are effective at disseminating information far and wide, casting a wide net for buyers and sellers to increase the chances of transactions. On the other hand, digitization in the real estate market could potentially disintermediate key players like agents who use information asymmetries to their advantage.

Sales Growth

A company’s long-term performance can give signals about its business quality. Any business can put up a good quarter or two, but many enduring ones muster years of growth. Cushman & Wakefield's annualized revenue growth rate of 2.9% over the last five years was weak for a consumer discretionary business.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Cushman & Wakefield's recent history shines a dimmer light on the company as its revenue was flat over the last two years.

This quarter, Cushman & Wakefield's revenue fell 3.6% year on year to $2.55 billion but beat Wall Street's estimates by 4.9%. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Cash Is King

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Over the last two years, Cushman & Wakefield broke even from a free cash flow perspective, subpar for a consumer discretionary business.

Cushman & Wakefield's free cash flow came in at $186.2 million in Q4, equivalent to a 7.3% margin and down 19.8% year on year. Over the next year, analysts' consensus estimates show they're expecting Cushman & Wakefield's LTM free cash flow margin of 0.9% to remain the same.

Key Takeaways from Cushman & Wakefield's Q4 Results

We enjoyed seeing Cushman & Wakefield exceed analysts' revenue and EPS expectations this quarter. That was driven by strong outperformance in its Leasing segment, which posted revenue of $587 million (5% year-on-year growth) versus Wall Street consensus estimates of $509 million. On the other hand, its operating margin missed and its Capital Markets segment continued its slump (Capital Markets revenue shrunk 31% year on year this quarter). Zooming out, we think this was still a decent, albeit mixed, quarter, showing that the company is staying on track. The stock is up 1.8% after reporting and currently trades at $11.34 per share.

So should you invest in Cushman & Wakefield right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.