Daqo New Energy (DQ): An Undervalued Gem in the Energy Sector?

Daqo New Energy Corp (NYSE:DQ) has recently seen a 3.29% loss, marking a 32.48% decrease over the past three months. Despite this, the company boasts an impressive Earnings Per Share (EPS) (EPS) of 13.75. The question now arises: is this stock significantly undervalued? In this article, we delve deep into the valuation analysis of Daqo New Energy (NYSE:DQ) to answer this question. We encourage you to read on to understand the intrinsic value of this stock better.

Company Overview

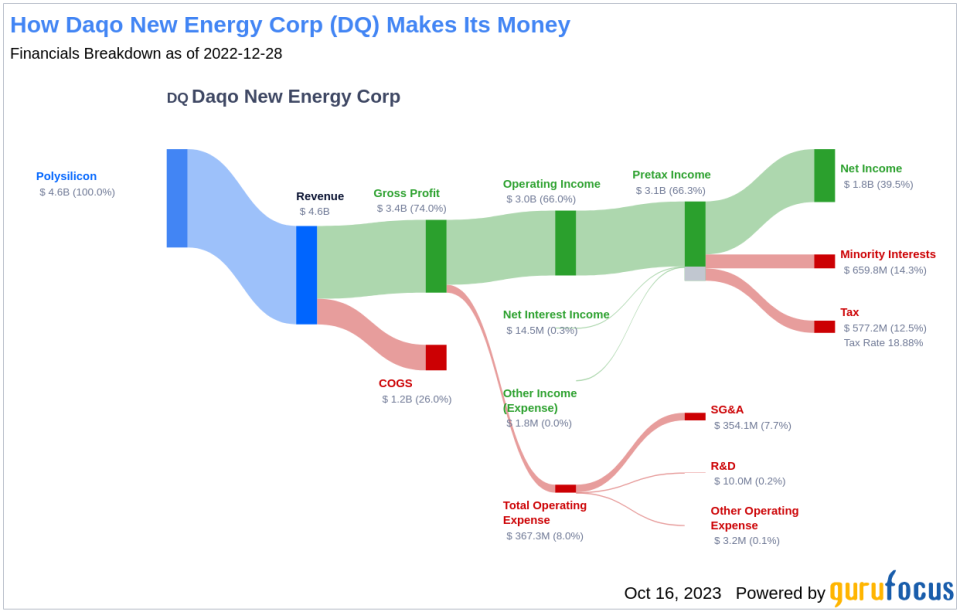

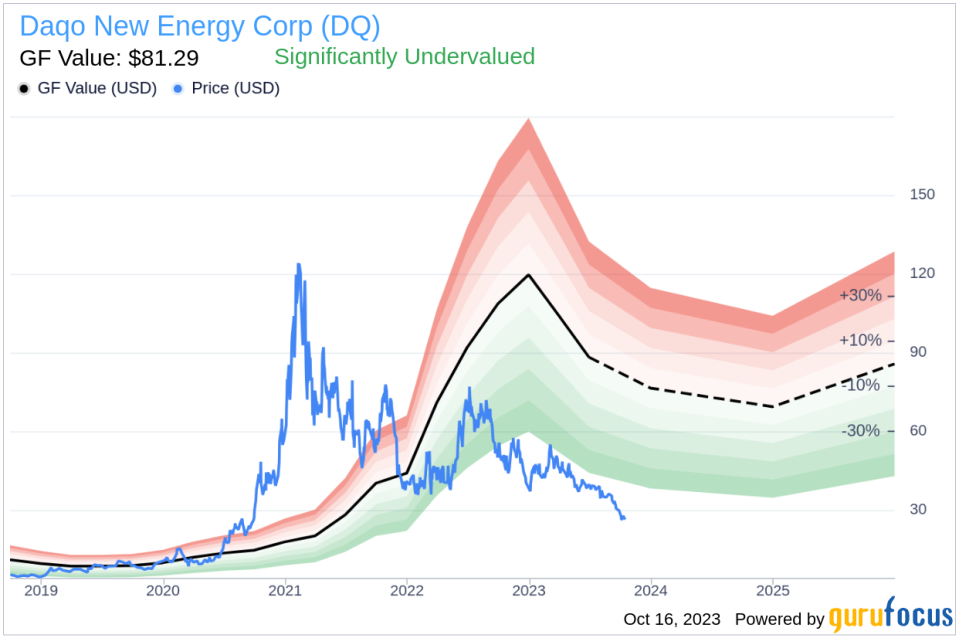

Daqo New Energy Corp is a renowned polysilicon manufacturer based in China. The company primarily manufactures and sells high-purity polysilicon to photovoltaic product manufacturers. These manufacturers process polysilicon into ingots, cells, and modules for solar power solutions. The company's stock currently trades at $26.01, while the GF Value, an estimation of fair value, stands at $81.29. This stark contrast paves the way for a deeper exploration of the company's value.

Understanding GF Value

The GF Value is a proprietary measure that represents the current intrinsic value of a stock. This measure is derived from three critical factors: historical multiples at which the stock has traded, an internal adjustment based on the company's past returns and growth, and future estimates of the business performance. The GF Value Line on our summary page gives an overview of the fair value at which the stock should ideally be traded.

Daqo New Energy (NYSE:DQ) is believed to be significantly undervalued based on GuruFocus' valuation method. If the share price is substantially above the GF Value Line, the stock may be overvalued, indicating poor future returns. Conversely, if the share price is significantly below the GF Value Line, the stock may be undervalued, suggesting higher future returns. At its current price of $26.01 per share, Daqo New Energy stock is believed to be significantly undervalued.

Given that Daqo New Energy is significantly undervalued, the long-term return of its stock is likely to be much higher than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength

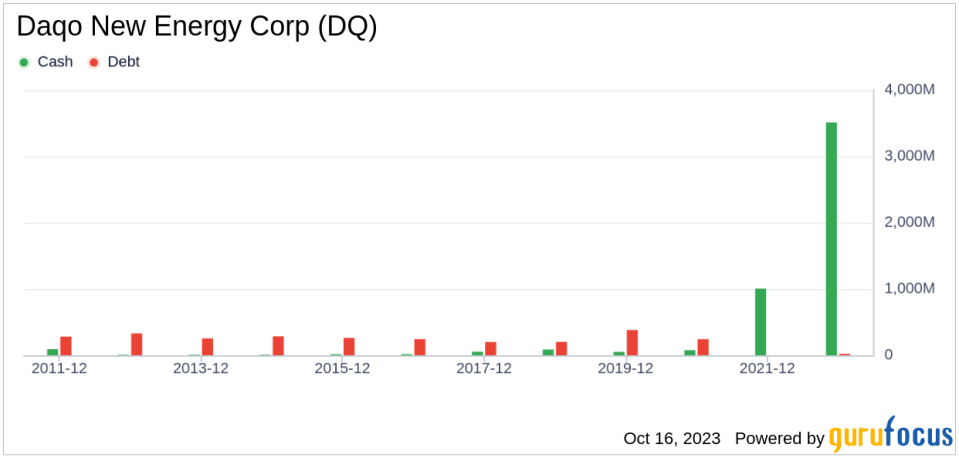

Before investing in a company's stock, it is crucial to check its financial strength. Investing in companies with poor financial strength poses a higher risk of permanent loss. A great way to understand a company's financial strength is by looking at the cash-to-debt ratio and interest coverage. Daqo New Energy has a cash-to-debt ratio of 10000, which is better than 99.89% of 903 companies in the Semiconductors industry. The overall financial strength of Daqo New Energy is 10 out of 10, indicating strong financial health.

Profitability and Growth

Companies that have been consistently profitable over the long term offer less risk for investors. Daqo New Energy has been profitable 9 over the past 10 years. Over the past twelve months, the company had a revenue of $3.40 billion and an EPS of $13.75. Its operating margin is 58.12%, which ranks better than 99.37% of 953 companies in the Semiconductors industry. Overall, the profitability of Daqo New Energy is ranked 9 out of 10, indicating strong profitability.

Growth is a critical factor in the valuation of a company. A faster-growing company creates more value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth of Daqo New Energy is 128.5%, which ranks better than 98.63% of 874 companies in the Semiconductors industry. The 3-year average EBITDA growth rate is 292%, which ranks better than 99.48% of 775 companies in the Semiconductors industry.

ROIC vs. WACC

Another method of determining the profitability of a company is to compare its return on invested capital (ROIC) to the weighted average cost of capital (WACC). ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. WACC is the rate that a company is expected to pay on average to all its security holders to finance its assets. When the ROIC is higher than the WACC, it implies the company is creating value for shareholders. For the past 12 months, Daqo New Energy's ROIC is 44.66, and its WACC is 5.94.

Conclusion

In summary, the stock of Daqo New Energy (NYSE:DQ) is believed to be significantly undervalued. The company's financial condition is strong, and its profitability is robust. Its growth ranks better than 99.48% of 775 companies in the Semiconductors industry. To learn more about Daqo New Energy stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.

This article first appeared on GuruFocus.