DaVita (DVA)'s True Worth: Is It Overpriced? An In-Depth Exploration

DaVita Inc (NYSE:DVA), a leading provider of dialysis services, experienced a daily loss of 4.8% and a 3-month loss of 1.3%. Despite these figures, the company reported an Earnings Per Share (EPS) (EPS) of 5.03. This raises a critical question: Is the stock modestly undervalued? Our valuation analysis, which delves into the company's financial health, profitability, and growth, seeks to provide an answer. We invite you to read on for an in-depth look at DaVita's valuation.

Company Overview

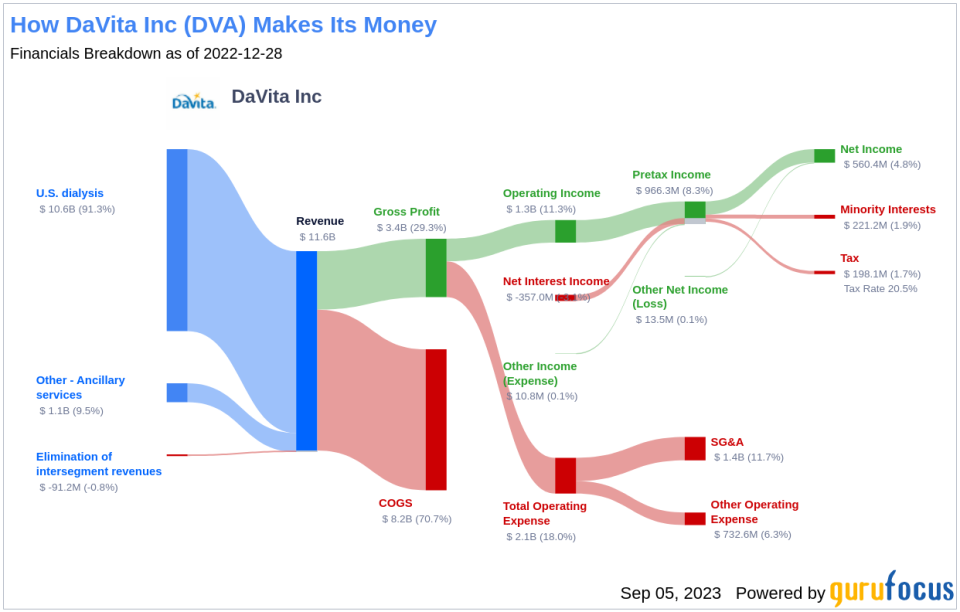

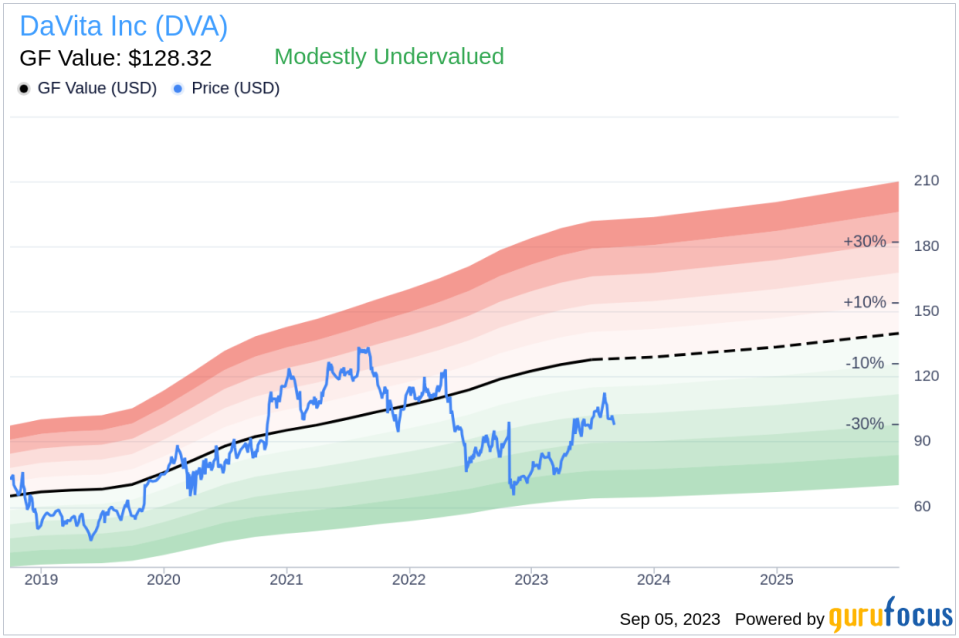

DaVita (NYSE:DVA) is the largest provider of dialysis services in the United States, with a market share exceeding 35%. The company operates over 3,000 facilities worldwide, treating over 240,000 patients annually. DaVita's revenue primarily comes from government payers, with commercial insurers accounting for nearly all of the company's U.S. dialysis business profits. The current stock price is $98.05, while the GF Value, an estimation of fair value, is $128.32. This discrepancy suggests that the stock may be modestly undervalued.

Understanding the GF Value

The GF Value is a proprietary measure of a stock's intrinsic value. It's calculated based on historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. On the other hand, if it is significantly below the GF Value Line, its future return will likely be higher.

According to GuruFocus' valuation method, DaVita (NYSE:DVA) appears to be modestly undervalued. The stock's fair value is estimated based on historical multiples, an internal adjustment based on the company's past business growth, and analyst estimates of future business performance. At its current price of $98.05 per share, DaVita stock appears to be modestly undervalued. Thus, the long-term return of its stock is likely to be higher than its business growth.

Link: These companies may deliver higher future returns at reduced risk.

Financial Strength

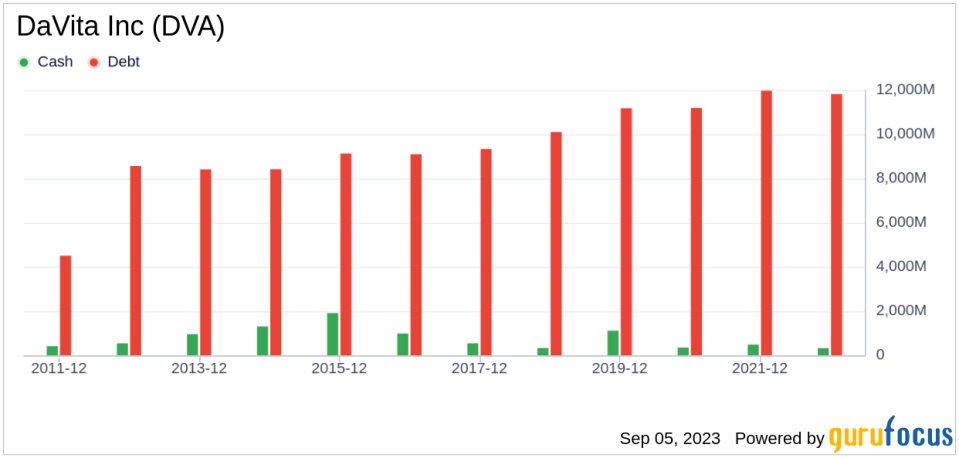

Investing in companies with poor financial strength has a higher risk of permanent loss of capital. Therefore, it's crucial to assess a company's financial strength before deciding to buy its stock. DaVita's cash-to-debt ratio of 0.03 is worse than 92.81% of 654 companies in the Healthcare Providers & Services industry. GuruFocus ranks DaVita's overall financial strength at 4 out of 10, indicating that the company's financial strength is poor.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, is less risky. DaVita has been profitable 10 out of the past 10 years. Over the past twelve months, the company had a revenue of $11.70 billion and an EPS of $5.03. Its operating margin is 10.73%, which ranks better than 73.57% of 647 companies in the Healthcare Providers & Services industry. Overall, DaVita's profitability is ranked 9 out of 10, indicating strong profitability.

One of the most critical factors in a company's valuation is growth. Companies that grow faster create more value for shareholders. DaVita's average annual revenue growth is 17.8%, ranking better than 71.28% of 571 companies in the Healthcare Providers & Services industry. The 3-year average EBITDA growth is 13.5%, which ranks better than 56.49% of 524 companies in the same industry.

ROIC vs WACC

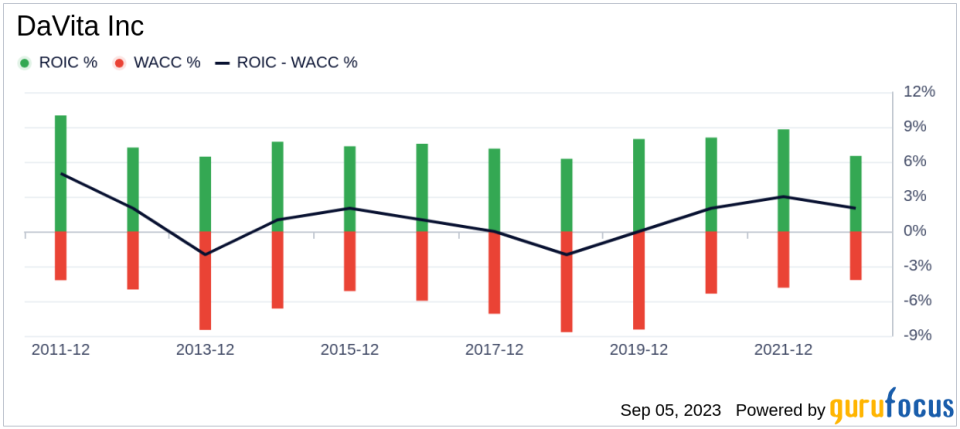

Comparing a company's return on invested capital (ROIC) to its weighted cost of capital (WACC) is another way to evaluate its profitability. ROIC measures how well a company generates cash flow relative to the capital it has invested in its business. WACC is the rate that a company is expected to pay on average to all its security holders to finance its assets. If the ROIC is higher than the WACC, it indicates that the company is creating value for shareholders. Over the past 12 months, DaVita's ROIC was 6.3, while its WACC came in at 5.31.

Conclusion

In conclusion, DaVita (NYSE:DVA) appears to be modestly undervalued. The company's financial condition is poor, but its profitability is strong. Its growth ranks better than 56.49% of 524 companies in the Healthcare Providers & Services industry. To learn more about DaVita stock, you can check out its 30-Year Financials here.

To find high-quality companies that may deliver above-average returns, please check out the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.