Deckers (NYSE:DECK) Reports Strong Q3, Stock Soars

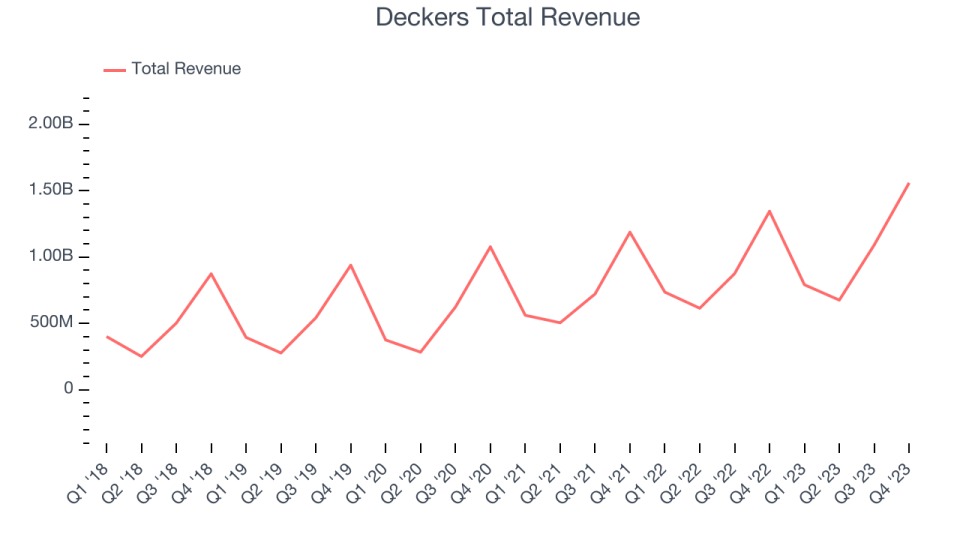

Footwear and apparel conglomerate Deckers (NYSE:DECK) reported Q3 FY2024 results beating Wall Street analysts' expectations , with revenue up 16% year on year to $1.56 billion. The company's full-year revenue guidance of $4.15 billion at the midpoint also came in 1.1% above analysts' estimates. It made a GAAP profit of $15.11 per share, improving from its profit of $10.48 per share in the same quarter last year.

Is now the time to buy Deckers? Find out by accessing our full research report, it's free.

Deckers (DECK) Q3 FY2024 Highlights:

Revenue: $1.56 billion vs analyst estimates of $1.45 billion (7.3% beat)

EPS: $15.11 vs analyst estimates of $11.66 (29.6% beat)

The company lifted its revenue guidance for the full year from $4.03 billion to $4.15 billion at the midpoint, a 3.1% increase

Gross Margin (GAAP): 58.7%, up from 53% in the same quarter last year

Market Capitalization: $19.39 billion

Established in 1973, Deckers (NYSE:DECK) is a footwear and apparel conglomerate with a portfolio of lifestyle and performance brands.

Footwear

In addition to practical purposes, footwear has been a way for people to communicate status or express themselves throughout history. Before the advent of the internet, styles changed, but consumers mainly bought clothing and accessories by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

Sales Growth

Exploring a company's long-term performance can offer valuable insights into its business quality. Any business can experience brief periods of success, but distinguished ones maintain steady growth over time. Deckers's annualized revenue growth rate of 15.2% over the last 5 years was solid for a consumer discretionary business.

Within consumer discretionary, a long-term historical view may miss a company riding a successful new product or emerging trend. That's why we also follow short-term performance. Deckers's healthy annualized revenue growth of 17.7% over the last 2 years is above its 5-year trend, suggesting its brand resonates with consumers.

Deckers also reports sales performance excluding currency movements, which are outside the company’s control and not indicative of demand. Over the last 2 years, its constant currency sales averaged 19.8% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see that macroeconomic challenges hindered Deckers's top-line performance.

This quarter, Deckers reported robust year-on-year revenue growth of 16%, and its $1.56 billion of revenue exceeded Wall Street's estimates by 7.3%. Looking ahead, Wall Street expects sales to grow 7.6% over the next 12 months, a deceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Deckers has been a well-managed company over the last eight quarters. It's demonstrated it can be one of the more profitable businesses in the consumer discretionary sector, boasting an average operating margin of 17.2%.

This quarter, Deckers generated an operating profit margin of 31.3%, up 4.2 percentage points year on year. This increase indicates the company was more efficient with its expenses over the last year, spending less money in areas like corporate overhead and advertising.

Over the next 12 months, Wall Street expects Deckers to become less profitable. Analysts are expecting the company’s LTM operating margin of 21.5% to decline to 19%.

Key Takeaways from Deckers's Q3 Results

We were impressed by how significantly Deckers blew past analysts' constant currency revenue expectations this quarter. We were also excited its operating margin outperformed Wall Street's estimates. Icing on the cake was the company raising its revenue and EPS guidance in a backdrop where some companies selling discretionary consumer goods have stumbled. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. The stock is up 6.9% after reporting and currently trades at $823.7 per share.

Deckers may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.