Decoding DocuSign Inc (DOCU): A Strategic SWOT Insight

DocuSign Inc showcases robust revenue growth and a return to profitability in its latest fiscal year.

Investments in AI and international expansion signal future growth potential.

Competitive pressures and cybersecurity risks remain key challenges for the company.

DocuSign's strong market position and innovative product offerings drive customer value.

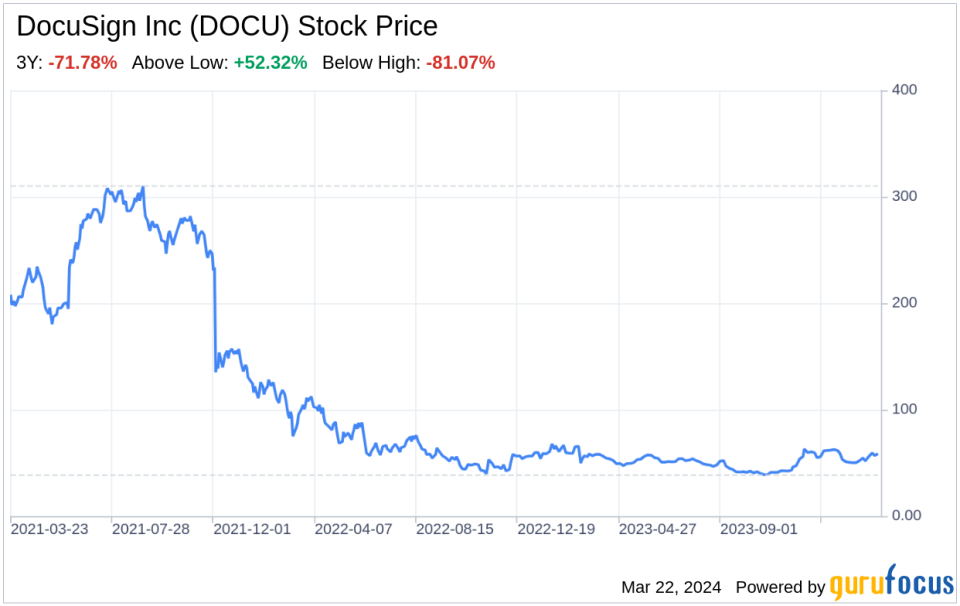

DocuSign Inc (NASDAQ:DOCU), a leader in the agreement cloud and e-signature solutions, filed its 10-K on March 21, 2024, revealing a year of financial recovery and strategic advancements. The company reported a significant revenue increase to $2.76 billion in 2024, up from $2.51 billion in 2023, and a notable swing to net profitability with $73.98 million in net income, a stark contrast to the previous year's loss of $97.45 million. This financial overview sets the stage for a comprehensive SWOT analysis, providing investors with a data-driven perspective on DocuSign Inc's current position and future prospects.

Strengths

Market Leadership and Brand Recognition: DocuSign Inc (NASDAQ:DOCU) has established itself as a leader in the e-signature and agreement cloud market, with over 1.5 million customers and a presence in more than 180 countries. The brand is synonymous with the digital agreement process, which has become increasingly vital in a world that prioritizes speed, efficiency, and remote capabilities. The company's strong brand recognition is not only a testament to its first-mover advantage but also to its continuous innovation, as evidenced by its extensive API integrations and partnerships with over 900 active partners.

Financial Resilience and Growth: The financial tables from the latest 10-K filing highlight DocuSign Inc's financial resilience. The company has successfully increased its subscription revenue to $2.69 billion, up from $2.44 billion in the previous year, indicating a solid and growing customer base that relies on its subscription services. This growth is a clear indicator of the strength of DocuSign's business model and its ability to scale effectively. Additionally, the return to profitability with a net income of $73.98 million is a positive sign for investors, showcasing the company's ability to manage costs and drive efficiency.

Weaknesses

Dependence on Subscription Revenue: While DocuSign Inc's subscription-based revenue model provides a recurring income stream, it also exposes the company to risks associated with customer retention and market saturation. The company's heavy reliance on subscription revenue means that any significant churn in its customer base could adversely affect its financial stability. Moreover, as the market for e-signature and digital agreement solutions matures, DocuSign may face challenges in maintaining its growth rates.

Operational Costs and Competition: The 10-K filing reveals that despite an increase in revenue, DocuSign Inc's operating expenses remain high, with sales and marketing expenses totaling $1.17 billion. This indicates that the company is investing heavily in customer acquisition and retention, which is essential in a competitive market but also puts pressure on margins. Additionally, the competitive landscape is intensifying, with rivals potentially offering lower prices or bundling services, which could force DocuSign to increase its marketing spend or reduce prices to maintain market share.

Opportunities

International Expansion and Market Penetration: DocuSign Inc has identified international expansion as a key growth strategy, with 26% of its revenue already coming from outside the U.S. The company's targeted investments in high-potential countries like Germany and Japan, along with a digital-first strategy in emerging markets, present significant opportunities for increasing its global customer base and diversifying revenue streams.

Product Innovation and AI Integration: The company's commitment to innovation, particularly in AI for contract analysis and automation, positions it well to capitalize on the growing demand for intelligent and automated agreement solutions. DocuSign's ongoing investments in AI and machine learning technologies could lead to the development of new products and features that enhance customer value and create additional revenue opportunities.

Threats

Technological Disruption and Competitive Pressure: The rapid pace of technological change poses a threat to DocuSign Inc, as new and disruptive technologies such as generative AI could alter the market dynamics. The company must continuously innovate to stay ahead of these changes and defend against competitors who may offer new or bundled solutions at lower prices.

Cybersecurity Risks: As a provider of digital agreement solutions, DocuSign Inc faces significant cybersecurity risks. Any breach or security incident could damage the company's reputation, lead to loss of customers, and result in substantial liabilities. DocuSign's reliance on third-party and public-cloud infrastructure further compounds these risks, making robust security measures and incident response plans critical to maintaining customer trust and operational integrity.

In conclusion, DocuSign Inc (NASDAQ:DOCU) presents a compelling case of a company that has successfully navigated the challenges of the past fiscal year to emerge stronger, with a clear path to sustained growth and profitability. The company's strengths in market leadership, brand recognition, and financial resilience are balanced by its weaknesses, including a heavy reliance on subscription revenue and high operational costs. Opportunities for international expansion and product innovation, particularly through AI integration, are countered by threats from technological disruption and cybersecurity risks. As DocuSign continues to execute its growth strategies and address its vulnerabilities, it remains a key player in the digital agreement space, poised to capitalize on the accelerating trend towards remote and automated business processes.

This article, generated by GuruFocus, is designed to provide general insights and is not tailored financial advice. Our commentary is rooted in historical data and analyst projections, utilizing an impartial methodology, and is not intended to serve as specific investment guidance. It does not formulate a recommendation to purchase or divest any stock and does not consider individual investment objectives or financial circumstances. Our objective is to deliver long-term, fundamental data-driven analysis. Be aware that our analysis might not incorporate the most recent, price-sensitive company announcements or qualitative information. GuruFocus holds no position in the stocks mentioned herein.

This article first appeared on GuruFocus.