Decoding Martin Marietta Materials (MLM)'s Market Value: A Comprehensive Examination of Its ...

As of October 04, 2023, Martin Marietta Materials Inc (NYSE:MLM) has seen a daily gain of 1.73%, and a 3-month loss of 10.31%. With an Earnings Per Share (EPS) of 15.24, the question arises: Is the stock fairly valued? In this article, we delve into a detailed valuation analysis of Martin Marietta Materials, providing valuable insights for investors. Read on for a comprehensive understanding of the company's intrinsic value.

A Snapshot of Martin Marietta Materials Inc (NYSE:MLM)

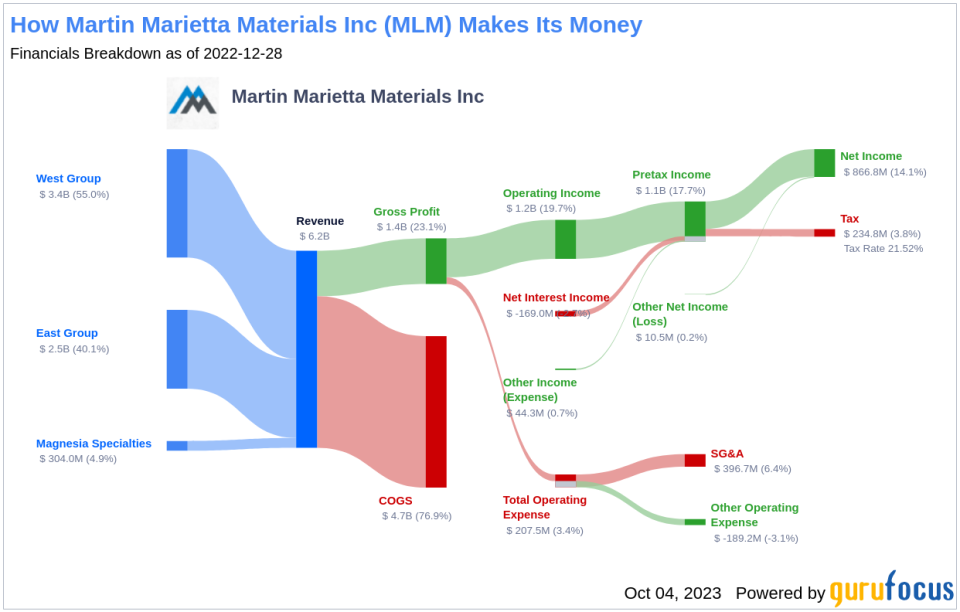

Martin Marietta Materials is one of the largest producers of construction aggregates in the United States. The company sold 207 million tons of aggregates in 2022, with its most significant markets being Texas, Colorado, North Carolina, Georgia, and Florida. Besides producing cement in Texas, Martin Marietta Materials also uses its aggregates in its asphalt and ready-mixed concrete businesses. Furthermore, the company's magnesia specialties business produces magnesia-based chemical products and dolomitic lime.

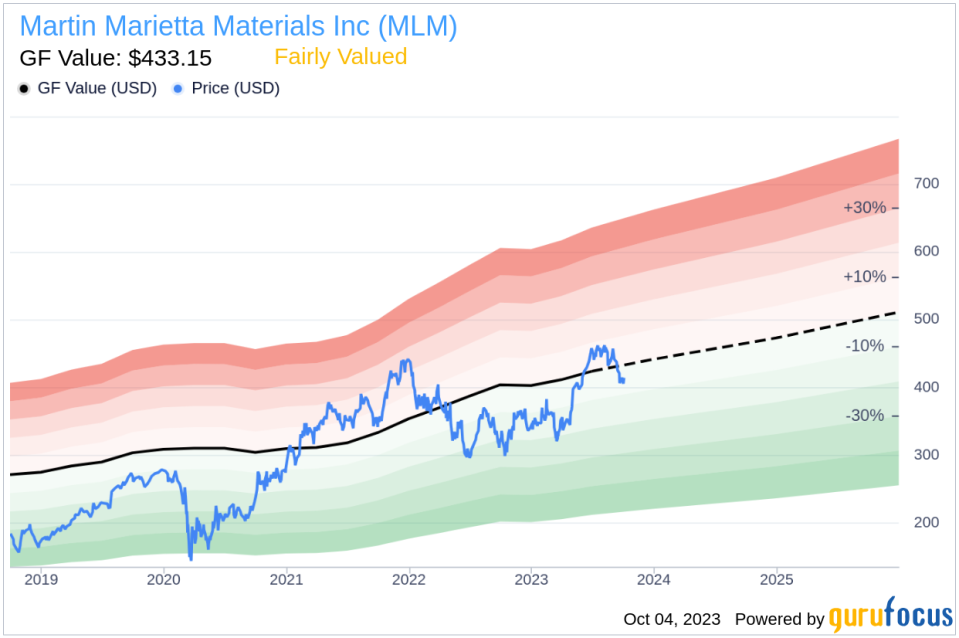

With a stock price of $411.36, Martin Marietta Materials has a market cap of $25.40 billion. The company's GF Value, a proprietary measure of a stock's intrinsic value, stands at $433.15, indicating that the stock is fairly valued.

Understanding GF Value

The GF Value represents the current intrinsic value of a stock, derived from GuruFocus' exclusive method. The GF Value Line provides an overview of the fair value at which the stock should be traded. It is calculated based on historical multiples, GuruFocus adjustment factor based on the company's past returns and growth, and future business performance estimates.

According to GuruFocus' valuation method, Martin Marietta Materials (NYSE:MLM) is estimated to be fairly valued. If the stock's share price is significantly above the GF Value Line, the stock may be overvalued and have poor future returns. Conversely, if the stock's share price is significantly below the GF Value Line, the stock may be undervalued and have high future returns. Given that Martin Marietta Materials is fairly valued, the long-term return of its stock is likely to be close to the rate of its business growth.

Financial Strength

Companies with poor financial strength pose a high risk of permanent capital loss to investors. To avoid this, investors must research and review a company's financial strength before deciding to purchase shares. Martin Marietta Materials has a cash-to-debt ratio of 0.08, ranking worse than 85.07% of 355 companies in the Building Materials industry. The overall financial strength of Martin Marietta Materials is 5 out of 10, indicating fair financial strength.

Profitability and Growth

Investing in profitable companies, especially those with consistent profitability over the long term, is less risky. Martin Marietta Materials has been profitable 10 over the past 10 years. Over the past twelve months, the company had a revenue of $6.50 billion and Earnings Per Share (EPS) of $15.24. Its operating margin is 20.63%, which ranks better than 87.29% of 362 companies in the Building Materials industry. Overall, the profitability of Martin Marietta Materials is ranked 9 out of 10, indicating strong profitability.

Growth is an essential factor in the valuation of a company. Martin Marietta Materials's 3-year average revenue growth rate is better than 64.59% of 353 companies in the Building Materials industry. Its 3-year average EBITDA growth rate is 12.4%, ranking better than 70.35% of 317 companies in the industry.

ROIC vs WACC

Comparing a company's return on invested capital and the weighted cost of capital is another way to look at its profitability. Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. On the other hand, the weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. For the past 12 months, Martin Marietta Materials's return on invested capital is 7.56, and its cost of capital is 8.9.

Conclusion

In short, the stock of Martin Marietta Materials (NYSE:MLM) is estimated to be fairly valued. The company's financial condition is fair, and its profitability is strong. Its growth ranks better than 70.35% of 317 companies in the Building Materials industry. To learn more about Martin Marietta Materials stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.