Despite Large Gain, Heritage Insurance Is Still Undervalued

Heritage Insurance Holdings Inc. (NYSE:HRTG) is a Florida-based insurance business that faced and survived disastrous years in 2021 and 2022 due to climate events in the U.S. Gulf Coast, inefficient risk calculation and lack of diversification. Management has learned from those two years, but the markets keep trading the stock at a discount. As such, it could be an attractive opportunity in the insurance sector for a two to five-year turnaround investment.

Overview of insurance company backed by large institutional investors

The company provides property and casualty insurance in the United States. It was founded in 2012 and two years later, started trading in the stock market. Heritage offers personal and commercial residential property insurance and rental property insurance in 16 states. It remains a relatively unknown insurance company; it is not even in the top 100 2022 largest P&C insurance companies. And yet, the company is backed by large institutional investors (34.4% ownership) with massive financial and analytical resources such as Vanguard and BlackRock.

Although it has had an impressive run since November 2022 with a 300% gain, the stock remains down 56% since its 2014 initial public offering. The Tampa, Florida-based company's stock is an attractive opportunity, in my opinion, given its fundamentals and insider trading activity.

Financials have rapidly improved

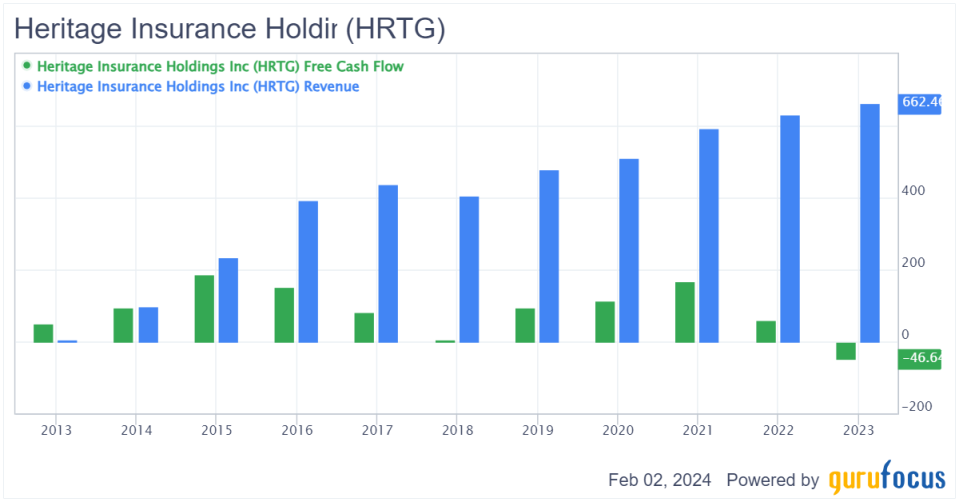

The company's revenue has grown steadily between 2014 and 2023, reaching around $700 million in revenue last year (the earnings report in a few weeks will confirm the exact amount) and the 2014 headcount of 90 has now exceeded 600 employees.

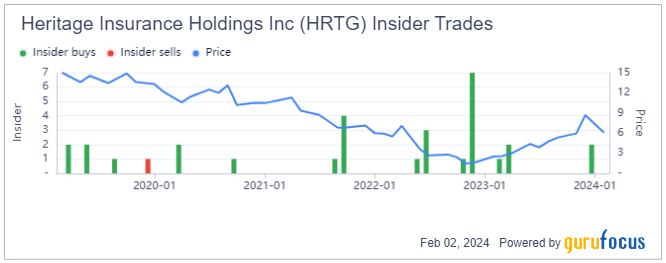

HRTG Data by GuruFocus

During its difficult period in 2021 and 2022, the company recorded negative operating income of $7.50 million and $65.40 million and, for the first time ever, negative free cash flow of $39.76 million. However, the business has shown its turnaround capabilities with a positive $42.72 million in 2023 operating income, in line with pre-Covid figures. The negative figures were caused by a series of natural disasters in the U.S. Gulf Coast (Hurricane Ian, the deadliest hurricane in Florida since 1935). With the business being concentrated in this area, the financials did suffer greatly in those two years. Management is currently mitigating this risk concentration, as I will explain later.

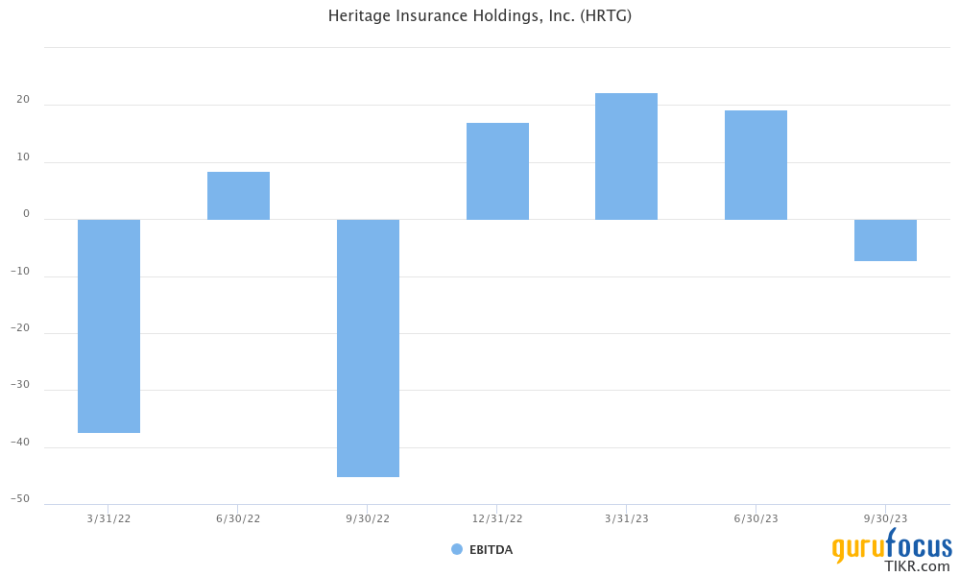

When I zoomed into the last seven quarters (the fourth quarter of 2023 is not yet available), I was able to see a clear improvement of the financial situation with Ebitda back to being positive in 2023. The last 12 months total debt-to-Ebitda ratio stands at a healthy level of 2.78.

The amount of cash the company currently sits on amounts to $228.85 million, exceeding the debt level of around $151 million, providing a comfortable cash buffer for unforeseen events. The level of cash at hand gives me sufficient comfort on how the business is cautiously run and can weather challenging times.

Trading at a discount

By practically every publicly available metric I could find, the stock is cheap. After the complicated years (due mostly to external factors), the markets have not yet efficiently repriced the stock to its current, much improved, financial situation, in my opinion.

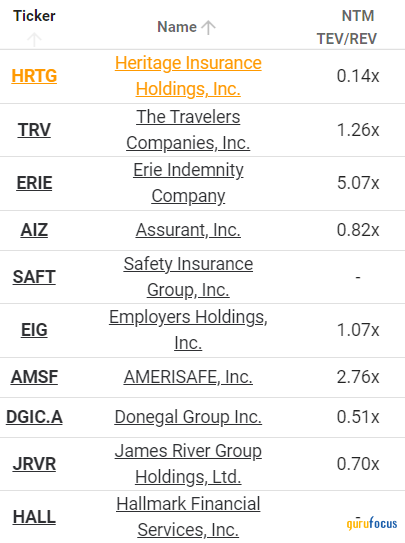

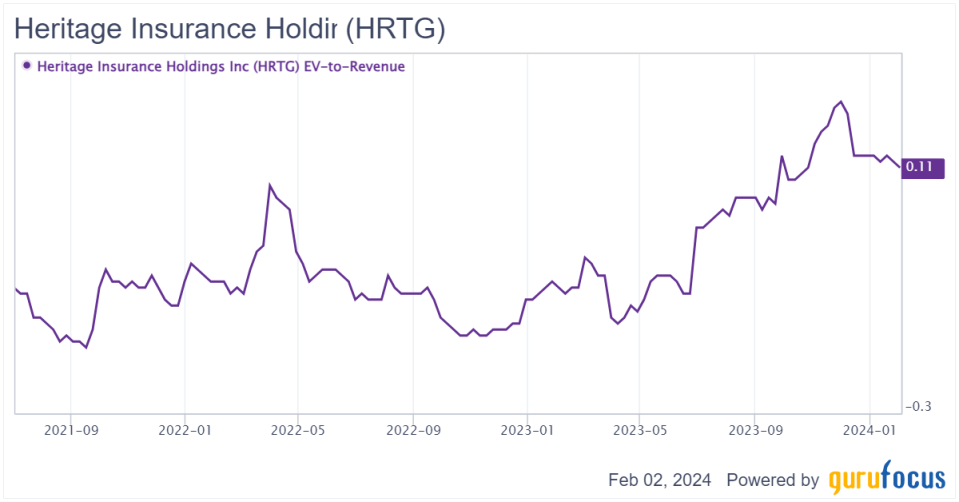

Indeed, the stock is currently trading at 0.14 times next 12 months total enterprise value/revenue, 0.15 times last 12 monts EV/revenue, 0.9 times last 12 months EV/gross profit and 2.10 times EV/Ebitda. The mean and median of the sector's next 12 months EV/revenue ratio lies much higher at 1.74 and 1.07. The competitors of Heritage Insurance are also valued at significantly higher multiples and if you prefer cheaper stocks for the same value like me, Heritage Insurance is an attractive candidate.

As I previously mentioned, the timing to purchase the stock is ideal in my opinion, as you may also conclude from the above chart. The business recently suffered from two complicated years due to natural events in the geography where Heritage Insurance's profitability concentration was located, explaining the significant discount relative to other, more diversified insurers.

However, the diversification efforts of management and renewed profitability strategy is likely to push the markets to reprice the stock at a significant multiple from here, closer to the fair value that I estimate to be around $25 (once the turnaround is confirmed over a few years), in line with competitors of similar size such as Donegal Group Inc. (NASDAQ:DGICA) and James River Group Holdings Inc. (NASDAQ:JRVR) (both companies have around $700 million to $800 million in revenue), currently trading at 0.50 times 0.70 times the next 12 months EV/revenue.

Competent management continues to purchase shares

Management revealed in the last available earnings report for the third quarter of 2023 the following key strategy focuses:

Generate underwriting profit through rate adequacy and more selective underwriting

Allocate capital to products and geographies that maximize long-term returns

Maintain a balanced and diversified portfolio

Provide coverage suitable to the market and return targets

These four action points aim at mitigating the financial impact of future unforeseen external events (in particular natural catastrophes) by implementing several changes in the way the insurance business is conducted. According to this earnings report, management is readjusting the policy pricing in response to the increased risk of certain geographic areas such as Florida. Chief Financial Officer Ernie Garateix explained during the second-quarter 2023 earnings call that Heritage selectively grew its Florida commercial residential in-force premiums by 75.5% over the prior year quarter (to reflect the geographic risk) while at the same time announced efforts to maintain a balanced and diversified portfolio continued with no state representing more than 26.2% of the company's TIV (total insurable value).

This new business plan is important to me as a potential investor because it clearly shows an approach of increased caution over the next few years. Indeed, to my understanding of the reports and earnings calls I read and listened to, I am clearly seeing a renewed strategy that seems to be emerging. This renewed business plan that will aim at diversifying both products and geographies to limit the risk of one single unforeseen event materially impacting the business viability. %hat provides me comfort as a potential investor that it is not planning to see the same challenging times it faced in 2021-22.

I found another argument to buy the Florida-based company's stock in the legal sphere. Indeed, the regulatory landscape is also changing with the New Florida Insurance Law 2023 with a few changes, some more positive for the business, others a bit more restrictive. The main benefit, however, is that, overall, the law aims at simplifying the claims handling by the insurance companies by removing a few administrative layers (one-way attorney fee repeal, policyholder claim time reduction, etc.). This could further boost Heritage Insurance.

Finally, I noticed management's optimism is also confirmed in the purchase of shares. Indeed, the insider trading activity reveals a strong uptick in share purchases by the company's management.

The purchase of shares typically either reveals positive sentiment of the management that the business will perform better or reveals that the business has already improved its performance. The insider trading activity is a key indicator for any company, given that it reflects optimism of management on the prospects of the business. This is, for me, another reason to believe the stock is an attractive buying opportunity for the next couple of years at least.

Bottom line: An attractive opportunity

After two years of struggle, Heritage Insurance, backed by large institutional investors and supported by a competent management team, is showing signs of a turnaround. The diversification, both geographic and in product, is reducing the risk the business is incurring to encounter again a period as complicated as 2021-22. The stock is still trading at a significant discount and the multiple insider purchases from management since mid-2021, with an acceleration since the end of 2022, is further confirming my thesis that the business is on track to return to long-term profitability and currently trading below its fair value. The stock, therefore, represents an attractive opportunity for the long term.

This article first appeared on GuruFocus.