Digging Into Direct Indexing

While direct indexing has been around for years and seems to be gaining momentum within the asset management community, misconceptions and oversimplifications remain around the technology and its capabilities.

While direct indexing will not be for everyone, it does have several use cases where it could be of value to investors with customization needs.

Clearing up these misunderstandings by providing education around what direct indexing is designed to achieve is an important measure. Doing so enables investors to have access to the information needed to make the best decisions to meet their unique investment goals and needs.

‘Direct Indexing Is Just A Fad’

The investment industry is not immune to fads, and many hot ideas that promised to add value for investors have not panned out as promised.

But in terms of ETFs, the majority of assets that have flowed into the investment vehicle this year have continued to be geared toward low-cost, passive ETFs. That trend is likely to persist in the future.

But at least for some, the higher degree of customization offered by direct indexing will be desirable. Daniel Gonzalez, analyst at Javelin Strategy & Research, believes that younger investors in particular will be attracted to custom indexing.

“Millennial and next-generation investors value customization—specifically when applying ESG preferences,” he said.

Javelin’s research supports this idea, with a recent study highlighting generational differences in preferences for a personalized ESG strategy.

(For a larger view, click on the image above)

As these younger investors inherit and continue to grow their wealth, their preference for customization could help drive more assets into direct indexing.

’It’s Only For High Net Worth Investors’

While direct indexing has long been used by institutional investors with larger pools of assets, minimums for direct indexing have decreased and will likely see continued downward pressure in the future.

Parametric, an early provider of custom indexing, offers standard separately managed accounts for $250,000. However, the company also offers a version with an account minimum of $75,000.

Jeff Brown, director and institutional portfolio manager at Parametric, elaborated on how the process is adjusted for smaller account sizes: “We do a version of the strategy where we use sector ETFs to do the index tracking and try to be tax-efficient there; so we’re not buying 400 names, we’re buying 11 names.”

He also suggests that account minimums would continue to come down in the future: “I think fractional shares could potentially have a role to play here. A $3,000 stock is a pretty spendy stock for $100,000. But if [you] could buy a fifth of a share, you could get minimums down.”

Gonzalez highlights an important consideration for smaller accounts: “For smaller account minimums, the asset manager will typically use a sample of securities or replicate it with ETFs. The problem with this approach is that you’ll get higher tracking error from the index.”

As with the other considerations, account size and the limitations this will place on the ability to customize and track the index is an additional factor to consider for investors interested in direct indexing. But smaller accounts are increasingly gaining access to this capability as technology advances.

‘It’s Active Management By Another Name’

While direct indexing will allow for differentiation from broad benchmarks, dismissing it as simply being “active management in disguise” is a disservice to investors.

In some use cases, the process could even be used to reduce active risk. Consider an example where an investor has a large position in Amazon stock in a taxable investment account, and that this position has a large unrealized gain.

The purchase of any cap-weighted large cap ETF such as the SPDR S&P 500 ETF Trust (SPY) will have a large weighting to this company.

Courtesy of FactSet

(For a larger view, click on the image above)

It might also be held in thematic ETFs owned by an investor, such as the ProShares Online Retail ETF (ONLN), where Amazon is a 26% position.

Courtesy of FactSet

(For a larger view, click on the image above)

By using the ETF.com Stock Finder, we can see that AMZN is widely held within various ETFs, showing up in 303 total.

In this example, the investor might have less “active” risk by excluding Amazon from its large cap exposure, due to the ability to avoid duplicating the individual stock holding or exposure from owning thematic ETFs such as ONLN.

Even if direct indexing is used to tilt the portfolio toward certain factors or ESG characteristics, the ETF industry has demonstrated there is investor appetite for these rules-based strategies, and that they can outperform in certain environments.

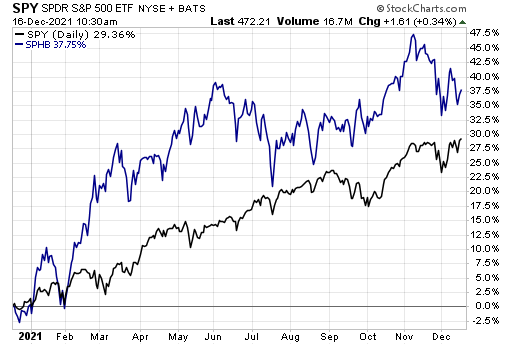

For example, an aggressive investor might want to tilt their portfolio toward higher beta names if they are extremely bullish on the market. A portfolio that tilted toward names like those found within the Invesco S&P 500 High Beta ETF (SPHB) would likely be outperforming SPY this year.

In combination with the potential for tax alpha and ESG customization, if desired, this could be a valuable proposition for some investors beyond using similar factor ETFs.

Victor Gomez, CEO and co-founder of BITA, proposes that, for some, the potential active exposure of direct indexing is a win for clients due to lower fees relative to actively managed funds: “You’re seeing a transition from active into passive, but for some asset owners, it’s not that simple. They’re getting a certain exposure through active management, they’re going to transition into passive to reduce fees, but the ETF [exposure] doesn’t match. That’s where direct indexing comes into play.”

But one thing to keep in mind—the more an investor tweaks a portfolio, the higher the level of tracking error possible.

Amrita Nandakumar, president of Vident Investment Advisory, elaborates on this point: “When you do customize your exposure through a process like direct indexing, you do take on benchmark risk. For financial advisors, there will be a balance between determining where it makes sense to offer that level of customization for a client and where it ends up being too difficult to measure against their standard benchmark.”

In other words, while there is the potential for active risk with the use of direct indexing, this will play out differently on a case-by-case basis.

Contact Jessica Ferringer at jessica.ferringer@etf.com or follow her on Twitter

Recommended Stories