Dillard's (DDS) Q2 Earnings & Sales Top Estimates, Stock Gains

Dillard's Inc. DDS posted second-quarter fiscal 2023 results, wherein the top and bottom lines surpassed the Zacks Consensus Estimate. This marked the company’s 10th straight quarter of a top and bottom-line beat. Results gained from better inventory management and strong consumer demand.

Adjusted earnings of $7.98 per share significantly surpassed the Zacks Consensus Estimate of $4.21. However, the bottom line declined 14.2% from the year-ago quarter's $9.30 per share.

Total revenues of $1,567.4 million decreased 1.3% from the prior-year quarter but beat the Zacks Consensus Estimate of $1,534 million.

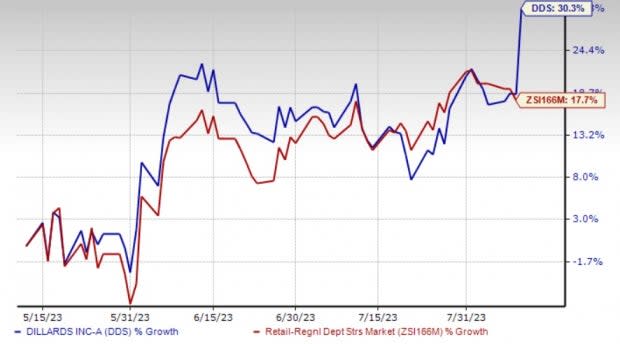

Dillard’s shares rallied 10% yesterday, driven by the robust second-quarter fiscal 2023 performance. Shares of the Zacks Rank #3 (Hold) company have rallied 30.3% in the past three months compared with the industry's growth of 17.7%.

Image Source: Zacks Investment Research

Total retail sales (excluding CDI Contractors, LLC) fell 3% year over year to $1,499 million. Comparable store sales also declined 3% year over year. Retail sales were affected by the continued cautiousness of consumers in the first few weeks of the fiscal second quarter.

Our model has predicted comps decline of 5.7% for the fiscal second quarter. The improved performance compared to our estimate can be attributed to the fading of the cautious consumer shopping behavior in the latter part of the quarter.

In the quarter, the company witnessed robust sales in cosmetics, and home and furniture categories. On the flip side, ladies’ accessories and lingerie, and ladies’ apparel and shoes were among the underperforming categories.

Dillard's, Inc. Price, Consensus and EPS Surprise

Dillard's, Inc. price-consensus-eps-surprise-chart | Dillard's, Inc. Quote

The consolidated gross margin contracted 200 basis points (bps) year over year to 38.8% in the fiscal second quarter. The retail gross margin of 40.4% reflected a year-over-year decline of 110 bps, driven by a significant gross margin decline in the men’s apparel and accessories, and a moderate decline in the juniors’ and children’s apparel categories.

Meanwhile, the company witnessed robust gross margin growth in the home and furniture category. The ladies’ accessories and lingerie categories reflected a moderation in gross margin growth during the quarter.

Dillard's consolidated SG&A expenses (as a percentage of sales) expanded 100 bps to 26.3% from the prior-year quarter's 25.3%. In dollar terms, SG&A expenses (operating expenses) grew 2.8% to $412.6 million. The increase in operating expenses is mainly attributed to higher payroll and payroll-related expenses.

Our model had predicted SG&A expenses (as a percentage of sales) to expand 200 bps to 26.8% in the fiscal second quarter. In dollar terms, we expected SG&A expenses to increase 2.4% year over year to $410.9 million.

Financial Details

Dillard’s ended the quarter with cash and cash equivalents of $774.3 million, long-term debt of $321.4 million, and total shareholders' equity of $1,709.5 million. The company provided $397.9 million of net cash from operating activities.

Capital expenditure for fiscal 2023 is likely to be $140 million, suggesting growth from the year-ago figure of $120 million.

In the fiscal second quarter, the company repurchased 358,000 Class A common stock for $103.4 million, under its existing repurchase program. As of Jul 29, DDS had an authorization worth $458.1 million remaining under its share repurchase program announced in May 2023.

Store Update

As of Jul 29, 2023, DDS operated 274 full-line Dillard’s stores and 27 clearance stores in 29 states and on dillards.com.

Outlook

For fiscal 2023, Dillard’s expects depreciation and amortization of $180 million, whereas it reported $188 million in the prior year. The company expects a net interest income of $5 million, whereas it recorded expenses of $31 million in the prior year. DDS anticipates rentals of $22 million for fiscal 2023.

Stocks to Consider

Here are some better-ranked stocks that you may want to consider, namely, Boot Barn BOOT, The Gap Inc. GPS and American Eagle Outfitters AEO.

Boot Barn, a lifestyle retail chain, currently flaunts a Zacks Rank #1 (Strong Buy). The company’s expected EPS growth rate for three to five years is 6.4%. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Boot Barn’s current fiscal year’s revenues suggests growth of 7.6% from the year-ago reported figure.

Gap, a premier international specialty retailer, currently sports a Zacks Rank #1. GPS has a trailing four-quarter earnings surprise of 12%, on average.

The Zacks Consensus Estimate for Gap’s current financial year’s EPS suggests growth of 25% from the year-ago reported figure. GPS has an expected EPS growth rate of 12% for three to five years.

American Eagle, a specialty retailer of casual apparel, accessories and footwear for men and women, carries a Zacks Rank #2 (Buy) at present. The company’s expected EPS growth rate for three to five years is 9.6%.

The Zacks Consensus Estimate for American Eagle’s current fiscal year’s EPS suggests growth of 275% from the year-ago reported figures. AEO has a trailing four-quarter earnings surprise of 9.2%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dillard's, Inc. (DDS) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

The Gap, Inc. (GPS) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report