Dine Brands (NYSE:DIN) Posts Q4 Sales In Line With Estimates

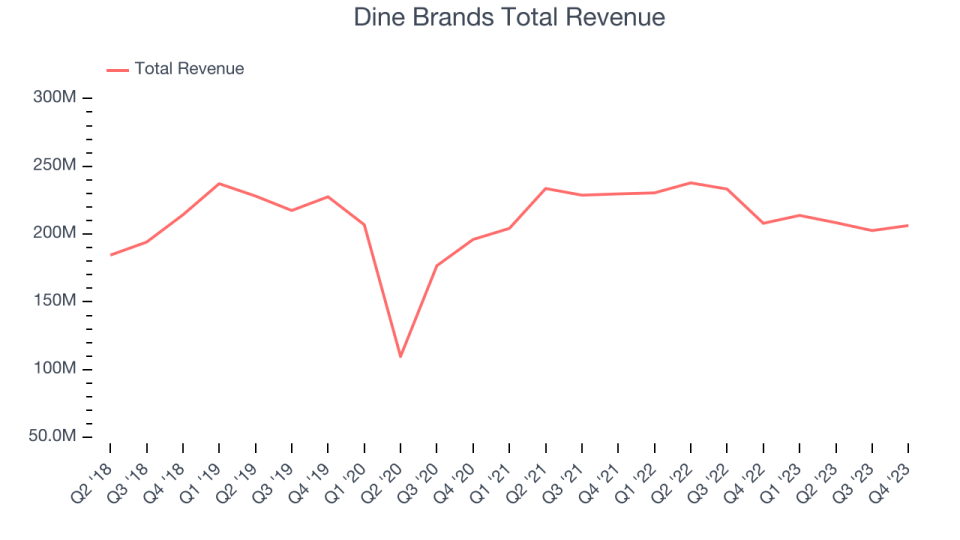

Casual restaurant chain Dine Brands (NYSE:DIN) reported results in line with analysts' expectations in Q4 FY2023, with revenue flat year on year at $206.3 million. It made a non-GAAP profit of $1.40 per share, improving from its profit of $1.34 per share in the same quarter last year.

Is now the time to buy Dine Brands? Find out by accessing our full research report, it's free.

Dine Brands (DIN) Q4 FY2023 Highlights:

Revenue: $206.3 million vs analyst estimates of $206.2 million (small beat)

EPS (non-GAAP): $1.40 vs analyst estimates of $1.15 (21.7% beat)

Free Cash Flow of $46.63 million, up 69.9% from the previous quarter

Gross Margin (GAAP): 47.7%, up from 45.9% in the same quarter last year

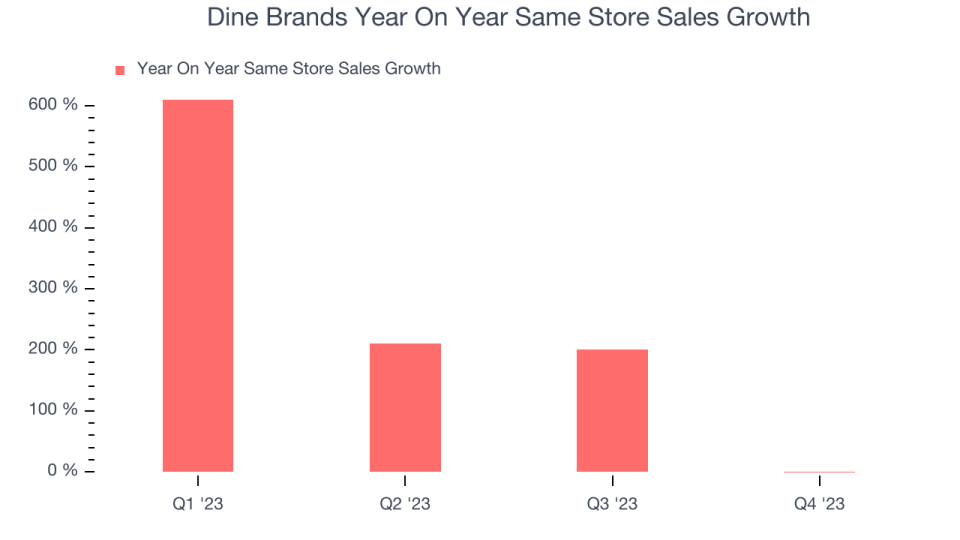

Same-Store Sales were down 0.5% year on year

Store Locations: 3,456 at quarter end, decreasing by 3 over the last 12 months

Market Capitalization: $713 million

“Our solid performance in the fourth quarter concluded a year of significant progress for Dine. We delivered another year of positive comp sales growth at IHOP and Applebee’s and generated year-over-year EBITDA growth while fully integrating Fuzzy’s into our system,” said John Peyton, Chief Executive Officer,

Operating a franchise model, Dine Brands (NYSE:DIN) is a casual restaurant chain that owns the Applebee’s and IHOP banners.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Sales Growth

Dine Brands is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Dine Brands can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue has declined over the last four years, dropping 2.2% annually as it didn't open many new restaurants.

This quarter, Dine Brands reported a rather uninspiring 0.8% year-on-year revenue decline to $206.3 million in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 1.4% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Same-Store Sales

Dine Brands's demand within its existing restaurants has generally risen over the last two years but lagged behind the broader sector. On average, the company's same-store sales have grown by 3.7% year on year. Given its flat restaurant base over the same period, this performance stems from increased foot traffic or larger order sizes per customer at existing locations.

In the latest quarter, Dine Brands's year on year same-store sales were flat. By the company's standards, this growth was a meaningful deceleration from the 1.8% year-on-year increase it posted 12 months ago. We'll be watching Dine Brands closely to see if it can reaccelerate growth.

Key Takeaways from Dine Brands's Q4 Results

Despite missing analysts' same-store sales expectations at Applebee's and IHOP, Dine Brands's revenue was in line with estimates. That was thanks to its contribution from Fuzzy's, a banner it acquired in December 2022. We were also glad Dine Brands beat analysts' EBITDA and EPS expectations this quarter. Zooming out, we think this was a decent quarter, showing that the company is staying on target. The stock is up 3.6% after reporting and currently trades at $47.8 per share. If it wants to sustain its gains over the long term, same-store sales growth at Applebee's and IHOP will need to accelerate.

So should you invest in Dine Brands right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.