District Heating Market Forecasted at $242.1 Billion by 2028, Dominated by Fortum, Vattenfall, ENGIE, Danfoss, and Statkraft

District Heating Market

Dublin, Feb. 02, 2024 (GLOBE NEWSWIRE) -- The "District Heating Market by Heat Source (Coal, Natural Gas, Geothermal, Biomass & Biofuel, Solar, Oil & Petroleum Products), Component (Boiler, Heat Exchanger, Heat Pumps), Plant Type (CHP, Boiler), Application and Region - Global Forecast to 2028" report has been added to ResearchAndMarkets.com's offering.

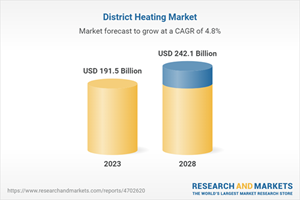

The global district heating market is expected to be valued at USD 191.5 billion in 2023 and is projected to reach USD 242.1 billion by 2028; it is expected to grow at a CAGR of 4.8% from 2023 to 2028. The key players operating in the market are Fortum (Finland), Vattenfall (Sweden), ENGIE (France), Danfoss (Denmark), Statkraft (Norway) among others.

The increasing trends of urbanization and industrialization are propelling an increased need for energy across various sectors, particularly in densely populated urban centers and industrial hubs. District heating systems emerge as a fitting solution for these areas, characterized by a concentration of buildings requiring heating and a substantial demand for heat in industrial operations. This centralized approach not only ensures dependable heating services but also contributes significantly to the reduction of pollution and overall energy consumption. Urbanization stands out as a prominent global megatrend, with ongoing urban development driving a heightened demand for district heating. The shift in population from rural to urban areas has resulted in a notable increase in public expenditures. This demographic shift has, in turn, spurred a consistent rise in the demand for heating, prompting substantial investments in the district heating sector. The growth of urban areas facilitates organized infrastructure development, creating a conducive environment for the implementation of district heating solutions.

The market is analyzed by heat source, plant type, application, and region. The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the district heating market. A detailed analysis of the key industry players has been done to provide insights into their business overviews, products, key strategies, contracts, partnerships, and agreements. New product & service launches, mergers and acquisitions, and recent developments associated with the district heating market are also covered. A competitive analysis of upcoming start-ups in the district heating market ecosystem is also covered in this report.

Renewables heat sources are growing at highest CAGR in district heating market

The renewables segment in the district heating market, encompassing sources such as geothermal, biomass & biofuel, and others like solar and wind, is experiencing the highest CAGR due to an escalating global emphasis on sustainable and eco-friendly energy solutions. As concerns about climate change intensify, there is a growing recognition of the environmental benefits offered by renewable energy sources. Governments and industries worldwide are increasingly investing in technologies that harness the power of nature, promoting the integration of renewable energy into district heating systems. The inherent advantages of renewables, including their ability to reduce carbon emissions, enhance energy security, and provide a reliable and consistent heat supply, are driving this segment's rapid growth. Additionally, advancements in renewable energy technologies, coupled with supportive policies and incentives, further contribute to the revenue growth observed in the renewables segment within the district heating market.

Boiler plants accounts for second-largest share in district heating market

Boiler plants secure the second-largest share in the district heating market by plant type due to their widespread adoption and versatility in providing cost-effective and efficient heat generation. Boilers are established and well-understood technologies with the capability to use various heat sources, including fossil fuels and biomass. Their adaptability makes them suitable for diverse applications in district heating systems, accommodating different scales of operation. Boiler plants offer a reliable and controllable means of producing heat, meeting the demands of both residential and industrial consumers. The familiarity, affordability, and proven performance of boiler plants contribute to their prominent market position, making them a preferred choice for district heating solutions globally.

Europe holds largest market share in district heating market

Europe dominates the district heating market by region, claiming the largest share, primarily due to a combination of historical infrastructure development, stringent environmental regulations, and a commitment to sustainable energy practices. Many European countries have a long-standing tradition of district heating systems, dating back decades, which has laid a robust foundation for their widespread adoption. Additionally, the region's proactive approach to combatting climate change has driven a shift towards cleaner and more efficient heating solutions. Stringent emissions standards and ambitious renewable energy targets have incentivized the expansion and modernization of district heating networks, utilizing a mix of renewable and waste heat sources. The European region's commitment to reducing carbon emissions and enhancing energy efficiency, coupled with a well-established district heating infrastructure, positions it as a leader in the global market.

Market Dynamics

Drivers

High Demand for Energy-Efficient and Cost-Effective Heating Systems

Rapid Urbanization and Industrialization

Increased Use of Renewable Sources to Run District Heating Systems

Relatively Low Operating Costs of District Heating Systems Than In-Building Heating Systems

Government-Led Incentives and Subsidies Offered for Low-Carbon Technology-Based Products

Enforcement of Carbon Tax on Fossil Fuel-Powered Heating Solutions

Restraints

Need for High Initial Investment

Barriers to District Heating Network Deployment in Small-Scale Projects

Time-Consuming and Complex Regulatory Approval Processes

Opportunities

Increasing Focus on Waste Heat Recovery for District Heating

Enforcement of Policies Boosting Renewable Energy Production

Integration of Multiple Energy Sources in Heat Generation

Utilization of Digital Technology in District Heating Networks

Challenges

Requirement for Smart Meters to Prevent Heat Loss During Heat Distribution Process

Need for Precise Load Planning and Better Utilization of Heating Systems

Limited Number of District Heating Networks to Harness Waste Heat

Technology Analysis

Use of Biofuels for District Heating

Geothermal Energy in District Heating

Usage of Waste Heat from Hydrogen Production

Fifth-Generation District Heating

Use of Nuclear Energy for District Heating

Smart District Heating

Carbon Capture and Utilization (CCU)

Case Study Analysis

Fortum Partners with Microsoft to Achieve Carbon-Neutral Heating Using Data Center Waste Heat Recovery

Danfoss Constructs District Heating Systems at Teknopark, Istanbul, to Address Complex Requirements of Project

Fjernvarme Fyn Consults Ramboli to Develop Heat Pump System That Transfers Surplus Energy from Facebook Data Center to District Heating Network of Odense

Vital Energi Provides Low-Carbon and Hot Water to Camden Locks Via Buried District Heating and Cooling Network

Companies Profiled

Fortum

Vattenfall

ENGIE

Danfoss

Statkraft

Logstor Denmark Holding ApS

Vital Energi

Kelag Energie & Warme

Shinryo Corporation

Veolia

General Electric

Uniper SE

Goteborg Energi

FVB Energy Inc.

Alfa Laval

Ramboll

Savon Voima

Enwave Energy Corporation

Orsted A/S

Helen Ltd.

Keppel Corporation Limited

Steag GmbH

Hafslund AS

Clearway Energy Group LLC

Dall Energy

Key Attributes

Report Attribute | Details |

No. of Pages | 222 |

Forecast Period | 2023-2028 |

Estimated Market Value (USD) in 2023 | $191.5 Billion |

Forecasted Market Value (USD) by 2028 | $242.1 Billion |

Compound Annual Growth Rate | 4.8% |

Regions Covered | Global |

For more information about this report visit https://www.researchandmarkets.com/r/uw9l6f

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world's leading source for international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, the top companies, new products and the latest trends.

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900