Are Dividend Investors Making A Mistake With Global Indemnity Limited (NASDAQ:GBLI)?

Today we'll take a closer look at Global Indemnity Limited (NASDAQ:GBLI) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. Unfortunately, it's common for investors to be enticed in by the seemingly attractive yield, and lose money when the company has to cut its dividend payments.

In this case, Global Indemnity pays a decent-sized 3.1% dividend yield, and has been distributing cash to shareholders for the past two years. A high yield probably looks enticing, but investors are likely wondering about the short payment history. Some simple analysis can reduce the risk of holding Global Indemnity for its dividend, and we'll focus on the most important aspects below.

Click the interactive chart for our full dividend analysis

Payout ratios

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Comparing dividend payments to a company's net profit after tax is a simple way of reality-checking whether a dividend is sustainable. Although Global Indemnity pays a dividend, it was loss-making during the past year. When a financial business is loss-making and pays a dividend, the dividend is not covered by profits. Its important that investors assess the quality of the company's assets and whether it can return to generating a positive income.

We update our data on Global Indemnity every 24 hours, so you can always get our latest analysis of its financial health, here.

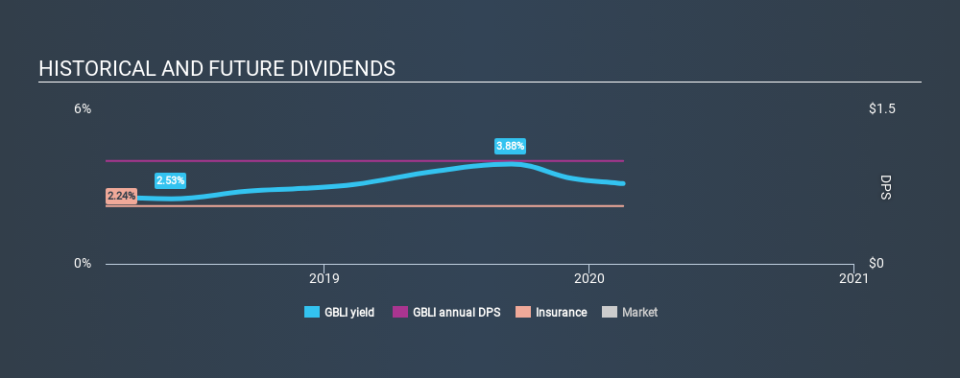

Dividend Volatility

One of the major risks of relying on dividend income, is the potential for a company to struggle financially and cut its dividend. Not only is your income cut, but the value of your investment declines as well - nasty. The company has been paying a stable dividend for a few years now, but we'd like to see more evidence of consistency over a longer period. Its most recent annual dividend was US$1.00 per share, effectively flat on its first payment two years ago.

We like that the dividend hasn't been shrinking. However we're conscious that the company hasn't got an overly long track record of dividend payments yet, which makes us wary of relying on its dividend income.

Dividend Growth Potential

Dividend payments have been consistent over the past few years, but we should always check if earnings per share (EPS) are growing, as this will help maintain the purchasing power of the dividend. Global Indemnity's EPS have fallen by approximately 53% per year during the past five years. A sharp decline in earnings per share is not great from from a dividend perspective, as even conservative payout ratios can come under pressure if earnings fall far enough.

Conclusion

Dividend investors should always want to know if a) a company's dividends are affordable, b) if there is a track record of consistent payments, and c) if the dividend is capable of growing. First, it's not great to see a dividend being paid despite the company being unprofitable over the last year. Earnings per share are down, and to our mind Global Indemnity has not been paying a dividend long enough to demonstrate its resilience across economic cycles. With any dividend stock, we look for a sustainable payout ratio, steady dividends, and growing earnings. Global Indemnity has a few too many issues for us to get interested.

Are management backing themselves to deliver performance? Check their shareholdings in Global Indemnity in our latest insider ownership analysis.

If you are a dividend investor, you might also want to look at our curated list of dividend stocks yielding above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.