What Docebo Inc.'s (TSE:DCBO) P/S Is Not Telling You

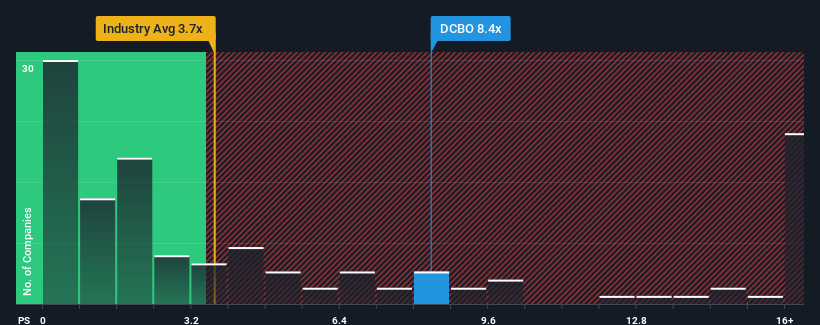

Docebo Inc.'s (TSE:DCBO) price-to-sales (or "P/S") ratio of 8.4x might make it look like a strong sell right now compared to the Software industry in Canada, where around half of the companies have P/S ratios below 3.7x and even P/S below 1.2x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/S.

View our latest analysis for Docebo

What Does Docebo's P/S Mean For Shareholders?

There hasn't been much to differentiate Docebo's and the industry's revenue growth lately. Perhaps the market is expecting future revenue performance to improve, justifying the currently elevated P/S. However, if this isn't the case, investors might get caught out paying too much for the stock.

Keen to find out how analysts think Docebo's future stacks up against the industry? In that case, our free report is a great place to start.

How Is Docebo's Revenue Growth Trending?

There's an inherent assumption that a company should far outperform the industry for P/S ratios like Docebo's to be considered reasonable.

Taking a look back first, we see that the company grew revenue by an impressive 37% last year. The latest three year period has also seen an excellent 245% overall rise in revenue, aided by its short-term performance. Accordingly, shareholders would have definitely welcomed those medium-term rates of revenue growth.

Turning to the outlook, the next three years should generate growth of 26% per annum as estimated by the eleven analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 24% per year, which is not materially different.

In light of this, it's curious that Docebo's P/S sits above the majority of other companies. It seems most investors are ignoring the fairly average growth expectations and are willing to pay up for exposure to the stock. Although, additional gains will be difficult to achieve as this level of revenue growth is likely to weigh down the share price eventually.

The Final Word

It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

Seeing as its revenues are forecast to grow in line with the wider industry, it would appear that Docebo currently trades on a higher than expected P/S. When we see revenue growth that just matches the industry, we don't expect elevates P/S figures to remain inflated for the long-term. Unless the company can jump ahead of the rest of the industry in the short-term, it'll be a challenge to maintain the share price at current levels.

Many other vital risk factors can be found on the company's balance sheet. Our free balance sheet analysis for Docebo with six simple checks will allow you to discover any risks that could be an issue.

If companies with solid past earnings growth is up your alley, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here