Does Antares Pharma (NASDAQ:ATRS) Have A Healthy Balance Sheet?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Antares Pharma, Inc. (NASDAQ:ATRS) does carry debt. But is this debt a concern to shareholders?

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Antares Pharma

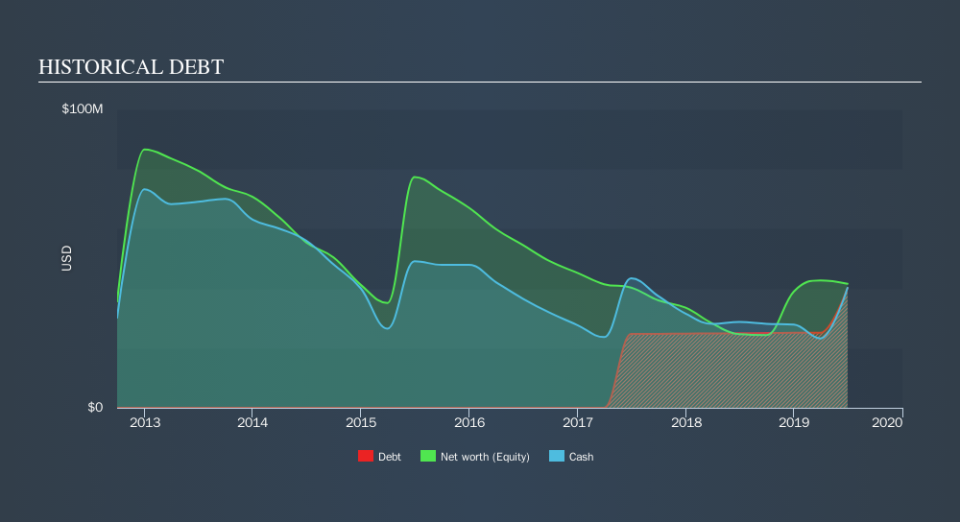

How Much Debt Does Antares Pharma Carry?

As you can see below, at the end of June 2019, Antares Pharma had US$40.1m of debt, up from US$25.0m a year ago. Click the image for more detail. However, its balance sheet shows it holds US$40.2m in cash, so it actually has US$28.0k net cash.

A Look At Antares Pharma's Liabilities

The latest balance sheet data shows that Antares Pharma had liabilities of US$25.8m due within a year, and liabilities of US$41.9m falling due after that. Offsetting this, it had US$40.2m in cash and US$30.9m in receivables that were due within 12 months. So it can boast US$3.43m more liquid assets than total liabilities.

This state of affairs indicates that Antares Pharma's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the US$546.3m company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Antares Pharma boasts net cash, so it's fair to say it does not have a heavy debt load! There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Antares Pharma can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Antares Pharma managed to grow its revenue by 58%, to US$88m. With any luck the company will be able to grow its way to profitability.

So How Risky Is Antares Pharma?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that Antares Pharma had negative earnings before interest and tax (EBIT), over the last year. And over the same period it saw negative free cash outflow of US$20m and booked a US$3.6m accounting loss. But at least it has US$40m on the balance sheet to spend on growth, near-term. Antares Pharma's revenue growth shone bright over the last year, so it may well be in a position to turn a profit in due course. Pre-profit companies are often risky, but they can also offer great rewards. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Antares Pharma's profit, revenue, and operating cashflow have changed over the last few years.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.