Does Cohort (LON:CHRT) Deserve A Spot On Your Watchlist?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Cohort (LON:CHRT). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Cohort

How Fast Is Cohort Growing?

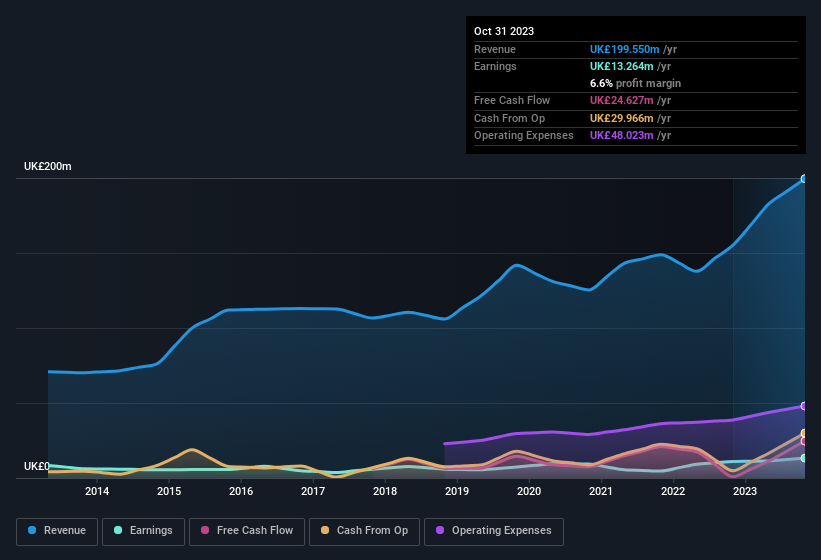

The market is a voting machine in the short term, but a weighing machine in the long term, so you'd expect share price to follow earnings per share (EPS) outcomes eventually. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Cohort managed to grow EPS by 13% per year, over three years. That's a pretty good rate, if the company can sustain it.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Cohort maintained stable EBIT margins over the last year, all while growing revenue 29% to UK£200m. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. Click on the chart to see the exact numbers.

The trick, as an investor, is to find companies that are going to perform well in the future, not just in the past. While crystal balls don't exist, you can check our visualization of consensus analyst forecasts for Cohort's future EPS 100% free.

Are Cohort Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

Despite some Cohort insiders disposing of some shares, we note that there was UK£77k more in buying interest among those who know the company best Although some people may hesitate due to the share sales, the fact that insiders bought more than they sold, is a positive thing to note. It is also worth noting that it was Independent Non-Executive director Peter Lynas who made the biggest single purchase, worth UK£82k, paying UK£5.45 per share.

On top of the insider buying, it's good to see that Cohort insiders have a valuable investment in the business. Holding UK£62m worth of stock in the company is no laughing matter and insiders will be committed in delivering the best outcomes for shareholders. At 28% of the company, the co-investment by insiders fosters confidence that management will make long-term focussed decisions.

While insiders are apparently happy to hold and accumulate shares, that is just part of the big picture. That's because Cohort's CEO, Andy Thomis, is paid at a relatively modest level when compared to other CEOs for companies of this size. For companies with market capitalisations between UK£79m and UK£314m, like Cohort, the median CEO pay is around UK£574k.

Cohort's CEO took home a total compensation package worth UK£446k in the year leading up to April 2023. That comes in below the average for similar sized companies and seems pretty reasonable. CEO compensation is hardly the most important aspect of a company to consider, but when it's reasonable, that gives a little more confidence that leadership are looking out for shareholder interests. Generally, arguments can be made that reasonable pay levels attest to good decision-making.

Should You Add Cohort To Your Watchlist?

As previously touched on, Cohort is a growing business, which is encouraging. Better yet, insiders are significant shareholders, and have been buying more shares. These factors alone make the company an interesting prospect for your watchlist, as well as continuing research. While we've looked at the quality of the earnings, we haven't yet done any work to value the stock. So if you like to buy cheap, you may want to check if Cohort is trading on a high P/E or a low P/E, relative to its industry.

Keen growth investors love to see insider buying. Thankfully, Cohort isn't the only one. You can see a a curated list of British companies which have exhibited consistent growth accompanied by recent insider buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.