How Does Guardian Capital Group's (TSE:GCG.A) CEO Pay Compare With Company Performance?

This article will reflect on the compensation paid to George Mavroudis who has served as CEO of Guardian Capital Group Limited (TSE:GCG.A) since 2011. This analysis will also evaluate the appropriateness of CEO compensation when taking into account the earnings and shareholder returns of the company.

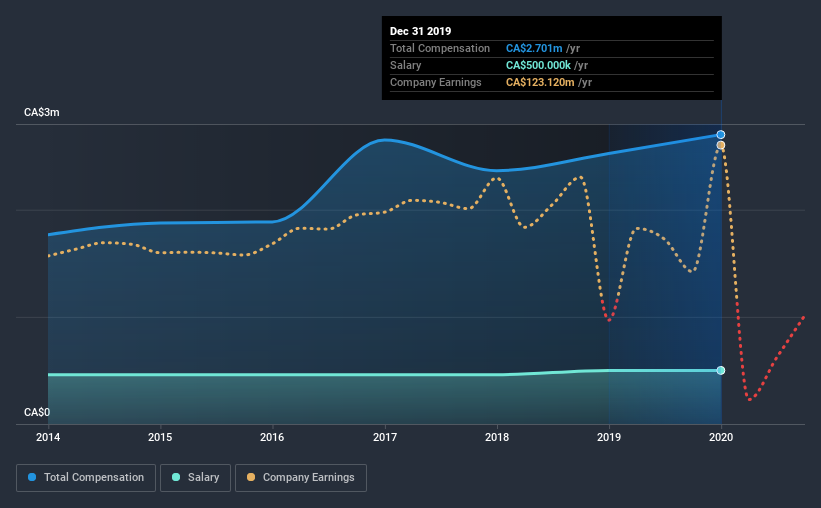

See our latest analysis for Guardian Capital Group

How Does Total Compensation For George Mavroudis Compare With Other Companies In The Industry?

At the time of writing, our data shows that Guardian Capital Group Limited has a market capitalization of CA$634m, and reported total annual CEO compensation of CA$2.7m for the year to December 2019. That's just a smallish increase of 6.9% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at CA$500k.

On examining similar-sized companies in the industry with market capitalizations between CA$259m and CA$1.0b, we discovered that the median CEO total compensation of that group was CA$2.5m. This suggests that Guardian Capital Group remunerates its CEO largely in line with the industry average. Furthermore, George Mavroudis directly owns CA$2.3m worth of shares in the company, implying that they are deeply invested in the company's success.

Component | 2019 | 2018 | Proportion (2019) |

Salary | CA$500k | CA$500k | 19% |

Other | CA$2.2m | CA$2.0m | 81% |

Total Compensation | CA$2.7m | CA$2.5m | 100% |

Speaking on an industry level, nearly 54% of total compensation represents salary, while the remainder of 46% is other remuneration. In Guardian Capital Group's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Guardian Capital Group Limited's Growth Numbers

Over the last three years, Guardian Capital Group Limited has shrunk its earnings per share by 60% per year. In the last year, its revenue is up 12%.

Few shareholders would be pleased to read that EPS have declined. There's no doubt that the silver lining is that revenue is up. But it isn't sufficiently fast growth to overlook the fact that EPS has gone backwards over three years. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Guardian Capital Group Limited Been A Good Investment?

Guardian Capital Group Limited has served shareholders reasonably well, with a total return of 12% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

As we noted earlier, Guardian Capital Group pays its CEO in line with similar-sized companies belonging to the same industry. Guardian Capital Group has had a poor showing when it comes to EPS growth, and it's tough to say that shareholder returns have done much to excite us. This doesn't compare well with CEO compensation, which is largely in line with the industry median. Considering all of this, we can't say the CEO is underpaid, and moving forward shareholders will likely want to see higher growth to justify any raise.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 2 warning signs for Guardian Capital Group you should be aware of, and 1 of them shouldn't be ignored.

Important note: Guardian Capital Group is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.