Does Houston Wire & Cable Company’s (NASDAQ:HWCC) PE Ratio Signal A Selling Opportunity?

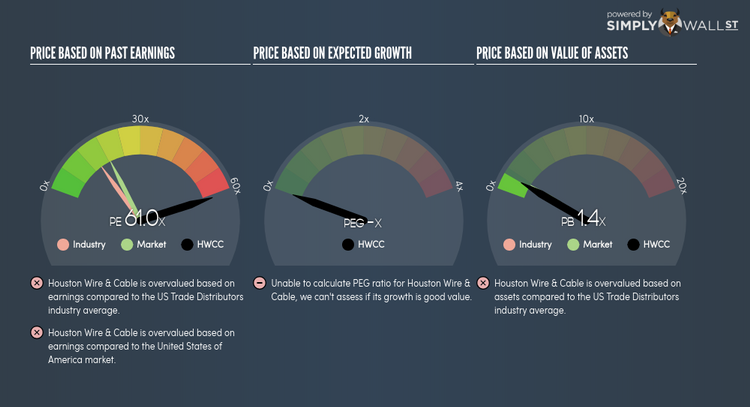

Houston Wire & Cable Company (NASDAQ:HWCC) is trading with a trailing P/E of 61x, which is higher than the industry average of 14.7x. While HWCC might seem like a stock to avoid or sell if you own it, it is important to understand the assumptions behind the P/E ratio before you make any investment decisions. Today, I will deconstruct the P/E ratio and highlight what you need to be careful of when using the P/E ratio. See our latest analysis for Houston Wire & Cable

Breaking down the Price-Earnings ratio

P/E is a popular ratio used for relative valuation. By comparing a stock’s price per share to its earnings per share, we are able to see how much investors are paying for each dollar of the company’s earnings.

P/E Calculation for HWCC

Price-Earnings Ratio = Price per share ÷ Earnings per share

HWCC Price-Earnings Ratio = $8.15 ÷ $0.134 = 61x

On its own, the P/E ratio doesn’t tell you much; however, it becomes extremely useful when you compare it with other similar companies. Our goal is to compare the stock’s P/E ratio to the average of companies that have similar attributes to HWCC, such as company lifetime and products sold. One way of gathering a peer group is to use firms in the same industry, which is what I’ll do. Since HWCC’s P/E of 61x is higher than its industry peers (14.7x), it means that investors are paying more than they should for each dollar of HWCC’s earnings. As such, our analysis shows that HWCC represents an over-priced stock.

A few caveats

However, before you rush out to sell your HWCC shares, it is important to note that this conclusion is based on two key assumptions. Firstly, our peer group contains companies that are similar to HWCC. If this isn’t the case, the difference in P/E could be due to other factors. For example, if you compared higher growth firms with HWCC, then its P/E would naturally be lower since investors would reward its peers’ higher growth with a higher price. The second assumption that must hold true is that the stocks we are comparing HWCC to are fairly valued by the market. If this does not hold true, HWCC’s lower P/E ratio may be because firms in our peer group are overvalued by the market.

What this means for you:

You may have already conducted fundamental analysis on the stock as a shareholder, so its current overvaluation could signal a potential selling opportunity to reduce your exposure to HWCC. Now that you understand the ins and outs of the PE metric, you should know to bear in mind its limitations before you make an investment decision. Remember that basing your investment decision off one metric alone is certainly not sufficient. There are many things I have not taken into account in this article and the PE ratio is very one-dimensional. If you have not done so already, I highly recommend you to complete your research by taking a look at the following:

Financial Health: Is HWCC’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

Past Track Record: Has HWCC been consistently performing well irrespective of the ups and downs in the market? Go into more detail in the past performance analysis and take a look at the free visual representations of HWCC’s historicals for more clarity.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.