What does Scorpio Tankers Inc’s (STNG) Balance Sheet Tell Us Abouts Its Future?

Investors are always looking for growth in small-cap stocks like Scorpio Tankers Inc (NYSE:STNG), with a market cap of $956.26M. However, an important fact which most ignore is: how financially healthy is the business? Companies operating in the oil and gas industry, especially ones that are currently loss-making, are inclined towards being higher risk. Evaluating financial health as part of your investment thesis is crucial. Here are a few basic checks that are good enough to have a broad overview of the company’s financial strength. However, this commentary is still very high-level, so I recommend you dig deeper yourself into STNG here.

Does STNG generate enough cash through operations?

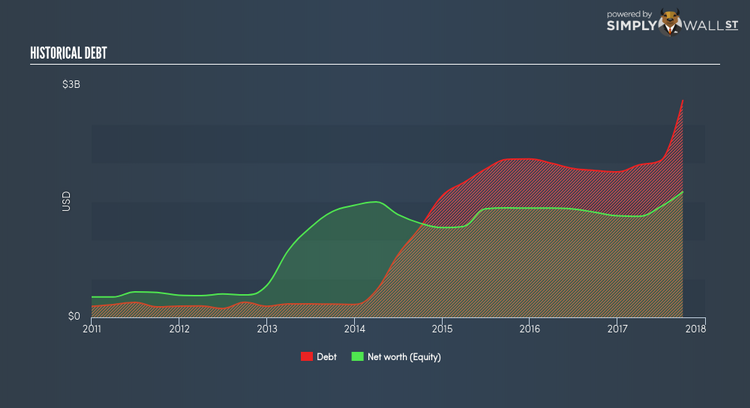

STNG’s debt levels have fallen from $2,050.0M to $1,882.7M over the last 12 months , which comprises of short- and long-term debt. With this reduction in debt, STNG’s cash and short-term investments stands at $99.9M for investing into the business. Moreover, STNG has produced cash from operations of $178.5M during the same period of time, leading to an operating cash to total debt ratio of 0.09x, meaning that STNG’s debt is not appropriately covered by operating cash. This ratio can also be a sign of operational efficiency for unprofitable businesses as traditional metrics such as return on asset (ROA) requires positive earnings. In STNG’s case, it is able to generate 0.09x cash from its debt capital.

Can STNG meet its short-term obligations with the cash in hand?

At the current liabilities level of $385.3M liabilities, it seems that the business has not maintained a sufficient level of current assets to meet its obligations, with the current ratio last standing at 0.41x, which is below the prudent industry ratio of 3x.

Can STNG service its debt comfortably?

Since total debt levels have outpaced equities, STNG is a highly leveraged company. This is not uncommon for a small-cap company given that debt tends to be lower-cost and at times, more accessible. But since STNG is currently loss-making, there’s a question of sustainability of its current operations. Maintaining a high level of debt, while revenues are still below costs, can be dangerous as liquidity tends to dry up in unexpected downturns.

Next Steps:

Are you a shareholder? STNG’s debt and cash flow levels indicate room for improvement. Its cash flow coverage of less than a quarter of debt means that operating efficiency could be an issue. However, its high liquidity means the company should continue to operate smoothly in the case of adverse events. Given that STNG’s financial situation may change. I suggest researching market expectations for STNG’s future growth on our free analysis platform.

Are you a potential investor? STNG’s high debt level indicates room for improvement. Furthermore, its cash flow coverage of less than a quarter of debt means that operating efficiency could also be an issue. However, the company exhibits an ability to meet its near term obligations should an adverse event occur. As a following step, you should take a look at STNG’s past performance analysis on our free platform to conclude on STNG’s financial health.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.