Dole (NYSE:DOLE) Misses Q3 Sales Targets, But Stock Soars 6.4%

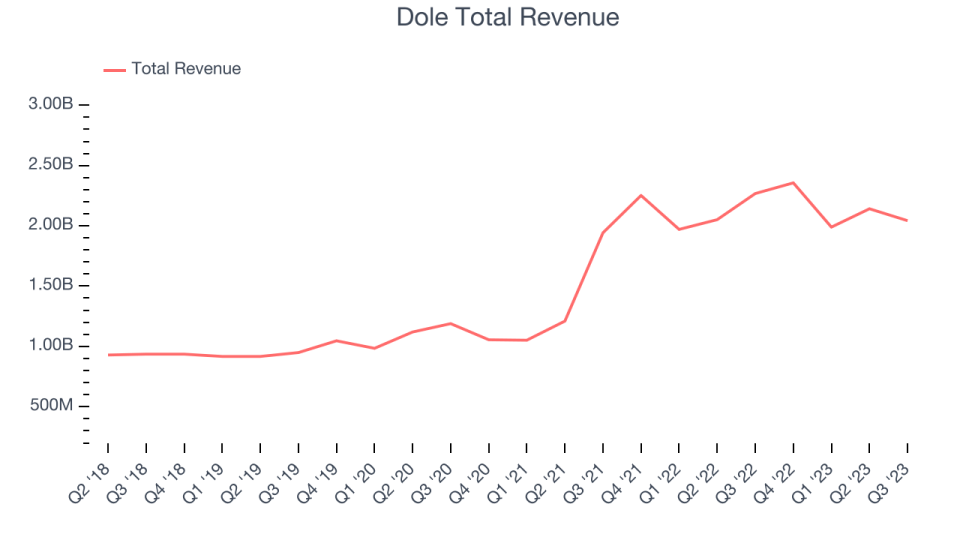

Fresh produce company Dole (NYSE:DOLE) fell short of analysts' expectations in Q3 FY2023, with revenue down 9.9% year on year to $2.04 billion. Turning to EPS, Dole made a GAAP profit of $0.48 per share, improving from its profit of $0.42 per share in the same quarter last year.

Is now the time to buy Dole? Find out by accessing our full research report, it's free.

Dole (DOLE) Q3 FY2023 Highlights:

Revenue: $2.04 billion vs analyst estimates of $2.18 billion (6.2% miss)

EPS: $0.48 vs analyst estimates of $0.10 ($0.38 beat)

Guidance for 2023 Adj. EBITDA of $365 million vs. $350 million prior (beat)

Free Cash Flow of $72.96 million, up 94.5% from the previous quarter

Gross Margin (GAAP): 8.1%, up from 6.1% in the same quarter last year

We are very pleased that our momentum from the first half of the year has continued into the third quarter. We delivered another strong set of results, with Revenue growth of 4.2% and Adjusted EBITDA growth of 7.6%.

Cherished for its delicious, world-famous pineapples and Hawaiian roots, Dole (NYSE:DOLE) is a global agricultural company specializing in fresh fruits and vegetables.

Packaged Food

As America industrialized and moved away from an agricultural economy, people faced more demands on their time. Packaged foods emerged as a solution offering convenience to the evolving American family, whether it be canned goods, prepared meals, or snacks. Today, Americans seek brands that are high in quality, reliable, and reasonably priced. Furthermore, there's a growing emphasis on health-conscious and sustainable food options. Packaged food stocks are considered resilient investments. People always need to eat, so these companies can enjoy consistent demand as long as they stay on top of changing consumer preferences. The industry spans from multinational corporations to smaller specialized firms and is subject to food safety and labeling regulations.

Sales Growth

Dole is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 25.3% over the last three years was exceptional for a consumer staples business.

This quarter, Dole reported a rather uninspiring 9.9% year-on-year revenue decline, missing Wall Street's estimates. Looking ahead, analysts expect sales to grow 3.7% over the next 12 months.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Operating Margin

Operating margin is a key profitability metric for companies because it accounts for all expenses enabling a business to operate smoothly, including marketing and advertising, IT systems, wages, and other administrative costs.

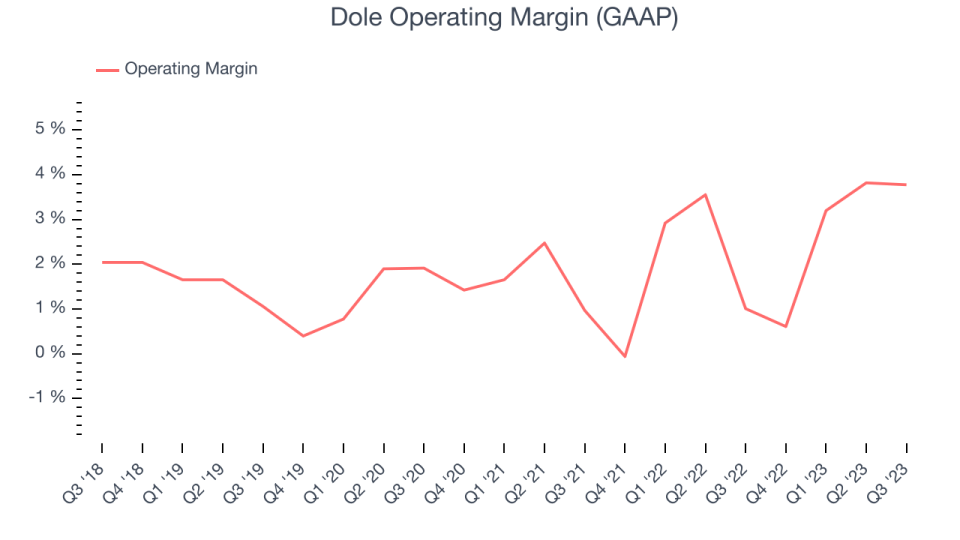

In Q3, Dole generated an operating profit margin of 3.8%, up 2.8 percentage points year on year. This increase was encouraging, and we can infer Dole was more efficient with its expenses because its operating margin expanded more than its gross margin.

Zooming out, Dole was profitable over the last eight quarters but held back by its large expense base. It's demonstrated subpar profitability for a consumer staples business, producing an average operating margin of 2.4%. Its margin has also seen few fluctuations, meaning it will likely take a big change to improve profitability.

Key Takeaways from Dole's Q3 Results

Sporting a market capitalization of $1.13 billion, Dole is among smaller companies, but its more than $223.3 million in cash on hand and positive free cash flow over the last 12 months puts it in an attractive position to invest in growth.

We were impressed by how significantly Dole blew past analysts' EPS expectations this quarter, which was driven by better profitability, as revenue missed. Full year guidance for adjusted EBITDA was raised, and this is a key positive. Overall, we think this was a fine quarter with some negatives and positives. The stock is flat after reporting and currently trades at $11.95 per share.

Dole may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.