DoubleVerify's (NYSE:DV) Q4 Earnings Results: Revenue In Line With Expectations But Stock Drops 19.5%

Digital media measurement and analytics provider DoubleVerify (NYSE:DV) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 28.9% year on year to $172.2 million. On the other hand, next quarter's revenue guidance of $138 million was less impressive, coming in 6.2% below analysts' estimates. It made a GAAP profit of $0.19 per share, improving from its profit of $0.17 per share in the same quarter last year.

Is now the time to buy DoubleVerify? Find out by accessing our full research report, it's free.

DoubleVerify (DV) Q4 FY2023 Highlights:

Revenue: $172.2 million vs analyst estimates of $171.7 million (small beat)

EPS: $0.19 vs analyst estimates of $0.13 (47% beat)

Revenue Guidance for Q1 2024 is $138 million at the midpoint, below analyst estimates of $147 million (adjusted EBITDA guidance for the period also missed expectations)

Management's revenue guidance for the upcoming financial year 2024 is $696 million at the midpoint, missing analyst estimates by 1.7% and implying 21.6% growth (vs 26.4% in FY2023) (adjusted EBITDA guidance for the period also missed expectations)

Free Cash Flow of $47.36 million, up 53.3% from the previous quarter

Gross Margin (GAAP): 82.6%, in line with the same quarter last year

Market Capitalization: $7.06 billion

“2023 was another year of exceptional growth and profitability driven by strong execution,” said Mark Zagorski, CEO of DoubleVerify.

When Oren Netzer saw a digital ad for US-based Target while sitting in his Tel Aviv apartment, he knew there was an unsolved problem, so he started DoubleVerify (NYSE:DV), a provider of advertising solutions to businesses that helps with ad verification, fraud prevention, and brand safety.

Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Sales Growth

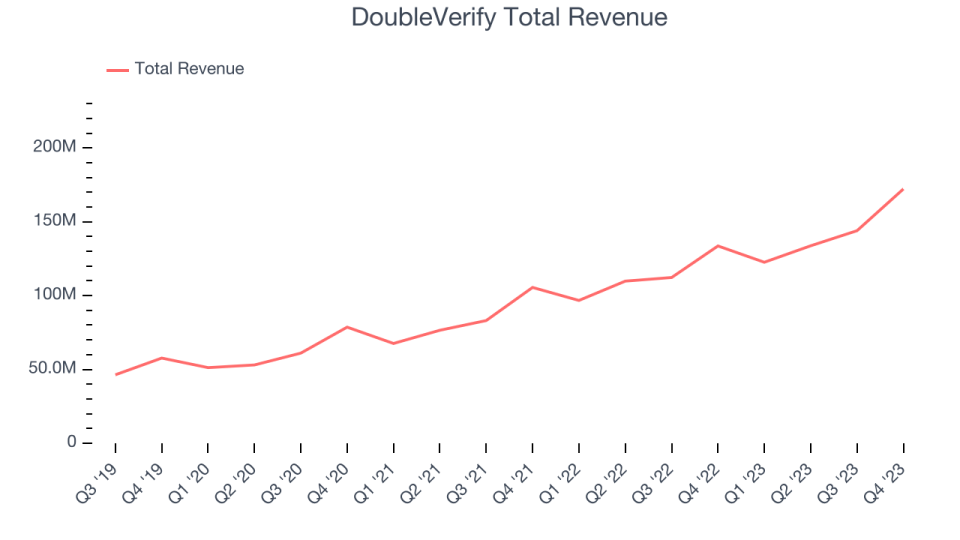

As you can see below, DoubleVerify's revenue growth has been very strong over the last two years, growing from $105.5 million in Q4 FY2021 to $172.2 million this quarter.

This quarter, DoubleVerify's quarterly revenue was once again up a very solid 28.9% year on year. On top of that, its revenue increased $28.26 million quarter on quarter, a very strong improvement from the $10.23 million increase in Q3 2023. This is a sign of acceleration of growth and great to see.

Next quarter's guidance suggests that DoubleVerify is expecting revenue to grow 12.6% year on year to $138 million, slowing down from the 26.7% year-on-year increase it recorded in the same quarter last year. For the upcoming financial year, management expects revenue to be $696 million at the midpoint, growing 21.6% year on year compared to the 26.6% increase in FY2023.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Cash Is King

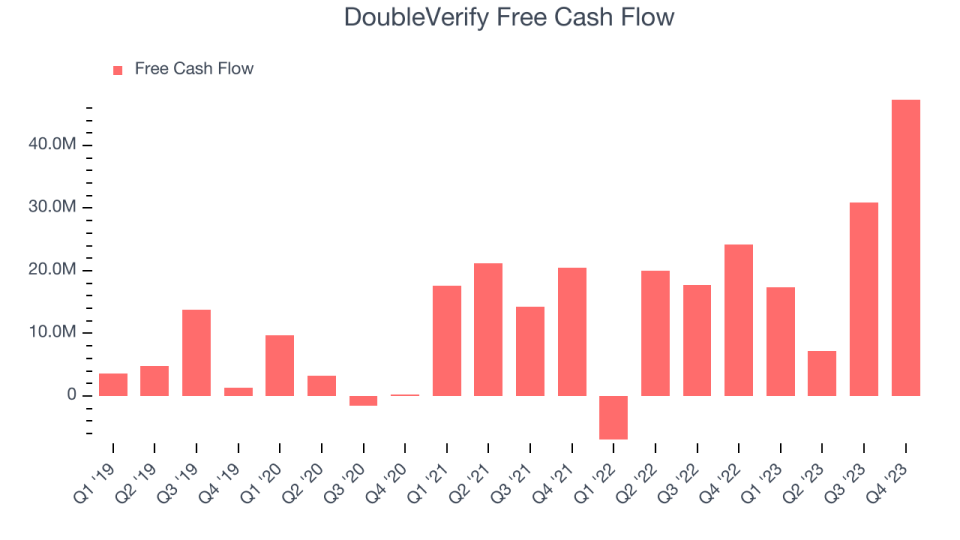

If you've followed StockStory for a while, you know that we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills. DoubleVerify's free cash flow came in at $47.36 million in Q4, up 95.4% year on year.

DoubleVerify has generated $102.7 million in free cash flow over the last 12 months, a solid 17.9% of revenue. This strong FCF margin stems from its asset-lite business model, giving it optionality and plenty of cash to reinvest in its business.

Key Takeaways from DoubleVerify's Q4 Results

Revenue in the quarter beat slightly, and gross margin improved this quarter. On the other hand, next quarter and full-year revenue as well as adjusted EBITDA guidance were both below expectations. Competitor Integral Ad Science (NASDAQ: IAS) also gave weak guidance yesterday and spoke of pricing competition and concessions in the industry, stoking fears of price wars and a deflationary environment. DV's quarter certainly is fanning those flames rather than putting the market at ease. Overall, this was a mediocre quarter for DoubleVerify. The company is down 19.5% on the results and currently trades at $31.59 per share.

DoubleVerify may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.