Down More Than 50%: 2 ‘Strong Buy’ Stocks That Are Too Cheap to Ignore

The stock market is regularly affected by wider macro developments but that only paints part of the picture. While overall market conditions can push any stock down, when you zoom in, you’ll find that every stock writes its own story, with its own reasons for ups and downs, and savvy investors will make sure to do the background research, learning those idiosyncratic reasons, before buying in.

Recognizing this, we’ve turned to some of the Wall Street analyst recommendations for pointers on two stocks that are down – but not out. Each has seen steep losses this year, for one reason or another, but it looks like certain analysts believe these stocks are now too cheap to ignore, as they see them offering investors triple-digit upside potential from their current trading price.

Additionally, there’s a wide held view on Wall Street that these are currently worth leaning into; according to the TipRanks database, both are also rated as Strong Buys by the analyst consensus with plenty of upside projected. Here are the details.

Aerovate Therapeutics (AVTE)

First on our list is Aerovate, a clinical-stage biopharmaceutical firm laser-focused on improving treatments for rare cardiopulmonary diseases. The company is currently working with the existing anti-cancer drug imatinib as a treatment for pulmonary arterial hypertension (PAH), that is, seriously elevated blood pressure in the lungs caused by blockages of the small arteries. The drug has been used in patients as an orally dosed treatment; as an innovation, Aerovate is working with imatinib as a dry powder inhalant. While PAH is a rare condition, there is a significant patient base existing, with more than 70,000 people in the US and Europe affected by the disease.

The company’s approach offers two main advantages over standard oral formulations for treating conditions in the lungs. First, imatinib is known to have systemic side effects, and even potential toxicity. The inhalant approach, by sending the drug directly to the area of action in the lung, minimizes these potential problems. And second, by using the inhalant dosing approach, Aerovate gets a higher dose to affected areas of the lung much faster than a pill will manage. As a result, the patient can use a lower dose to begin with – which goes back to the first issue, of minimizing adverse side effects.

AV-101, Aerovate’s leading product, is a self-administered dry powder inhalant currently under investigation in the IMPAHCT trial, a global Phase 2b/3 study in the treatment of PAH. The company reports continuing progress in the study, which has more than 110 clinical sites in over 20 countries, with additional clinical sites planned for activation. Aerovate expects to release topline data from the Phase 2b component of the IMPAHCT study during 2Q24.

We should note that Aerovate is a pre-revenue, research-oriented firm, with high overheads and consistent quarterly losses. Such biotech stocks without near-term catalysts can be volatile, and to wit, shares in AVTE are down 54% so far this year.

The company has also been using ATM (at-the-market) stock sales as one mode of fundraising. In 2Q23, the firm sold off $45 million worth of shares. As of June 30 this year, Aerovate reported having $150.1 million in cash and other liquid assets on hand, and claims a cash runway sufficient to maintain operations into 2026.

For Guggenheim analyst Vamil Divan, the key point here is the high commercialization potential of AV-101. He writes of Aerovate and its leading product, “We remain bullish on AV-101’s clinical and commercial potential, as the company works to leverage the efficacy of oral imatinib with a more targeted delivery approach directly to the lungs that should minimize systemic toxicities. We see a meaningful role for AV-101 on top of current PAH treatment options, and believe AV-101’s mechanism of action should allow for it to be used in combination with MRK’s sotatercept or in patients who progress or cannot tolerate sotatercept.”

Looking ahead, Divan gives AVTE shares a Buy rating, and his $36 price target implies a high one-year upside potential of 168%. (To watch Divan’s track record, click here.)

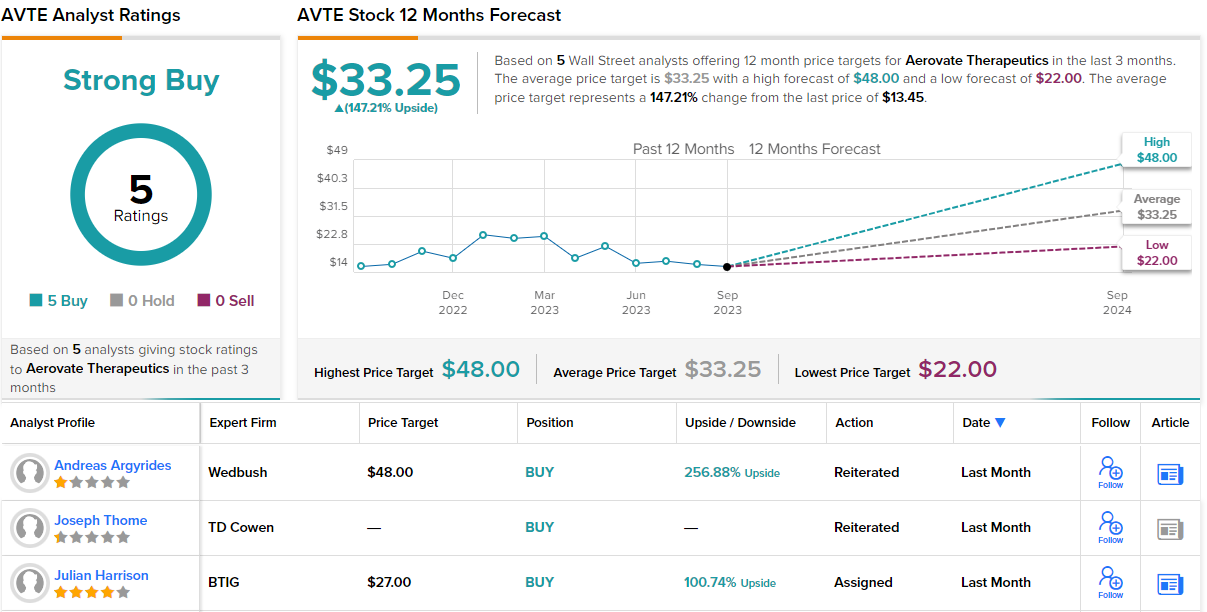

The Guggenheim view on this stock is no outlier, as shown by the unanimous Strong Buy consensus rating, based on 5 positive analyst reviews on file. The shares are trading for $13.45, and their $33.25 average price target points toward a 12-month gain of 147%. (See Aerovate’s stock forecast.)

Vir Biotechnology (VIR)

Next up is Vir Biotechnology, an immunology-focused pharmaceutical researcher working on ways to treat and prevent infectious diseases. The company vision is based on ‘a world without infectious disease,’ and its development program is broad-based, targeting viral infections such as hepatitis, influenza, and HIV. Vir has several hepatitis-B candidates in the clinic, at the Phase 2 level, and is preparing to initiate a Phase 1 trial for an HIV vax candidate.

The biggest news about Vir, however, is about a failure. This is hardly unusual for a biotech researcher; far more pipeline programs fail than succeed and move to approval. In this case, Vir’s drug candidate VIR-2482, a potential vaccine against influenza, failed to meet the Phase 2 clinical trial goals. The trial, dubbed PENINSULA, was testing the drug as a preventative against influenza, and in a July 20 data release the company announced that the drug had not met its primary or secondary efficacy endpoints. Shares in VIR dropped 45% on the news. Year-to-date, the stock is down 62%.

While the -2482 program has suffered a serious setback, the company’s hepatitis and HIV programs remain on track. VIR has two drug candidates targeting hepatitis-B, undergoing multiple ongoing clinical trials. The aim is to develop a functional cure for chronic hepatitis-B. Data readouts from these trials are expected in 4Q23 and 1H24.

In the HIV program, Vir’s Phase 1 study of VIR-1388, a novel T-cell vaccine intended as a preventative against HIV, is set to begin dosing during this 3Q23.

These upcoming catalysts are at the base of Leerink Partners’ Roanna Ruiz’s upbeat take on the stock. The analyst writes, “With multiple programs in the clinic (HBV, HDV, and HIV), Vir could become a leading infectious disease biopharma with a management team that has expertise in infectious disease, drug development, and commercialization; further, their ~$1.9B cash position offers ample support for Vir’s multiple clinical development efforts without the need for near-term capital raises.”

Ruiz goes on to rate this stock as Outperform (a Buy), with a $24 price target that implies a robust upside of 149% in the next 12 months. (To watch Ruiz’s track record, click here.)

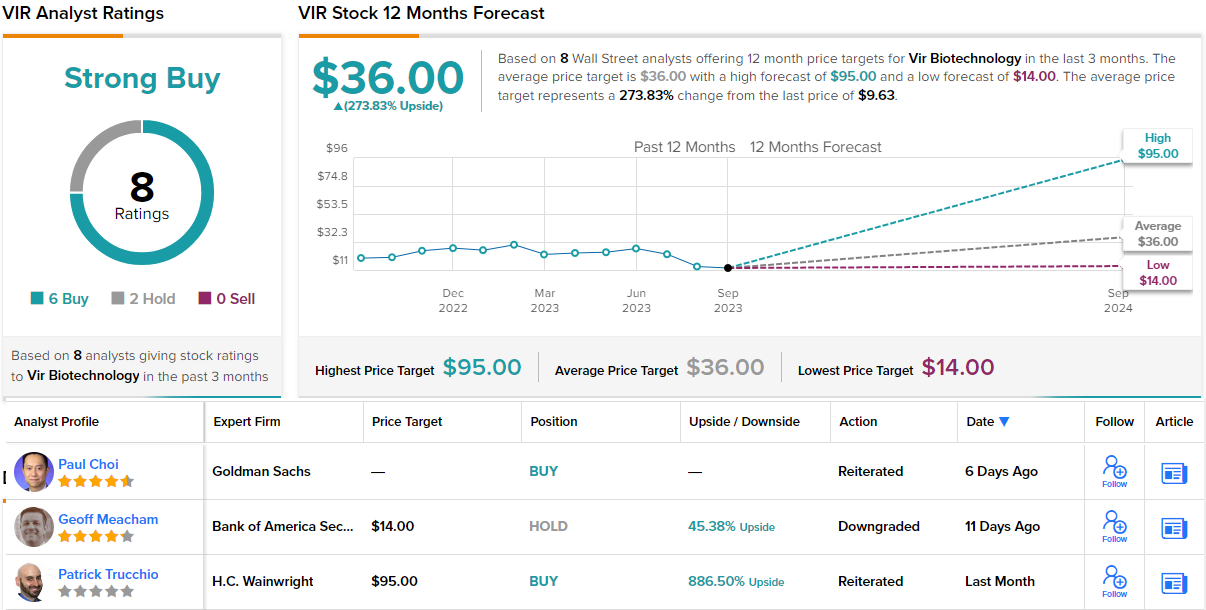

This company has picked up 8 recent analyst reviews, including 6 to Buy against 2 Holds, to support its Strong Buy analyst consensus rating. The average price target of $36 suggests a powerful 274% gain in the coming year, from the current trading price of $9.63. (See Vir Biotechnology’s stock forecast.)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.